GPU as a Service (GPUaaS) Market Overview and Key Insights:

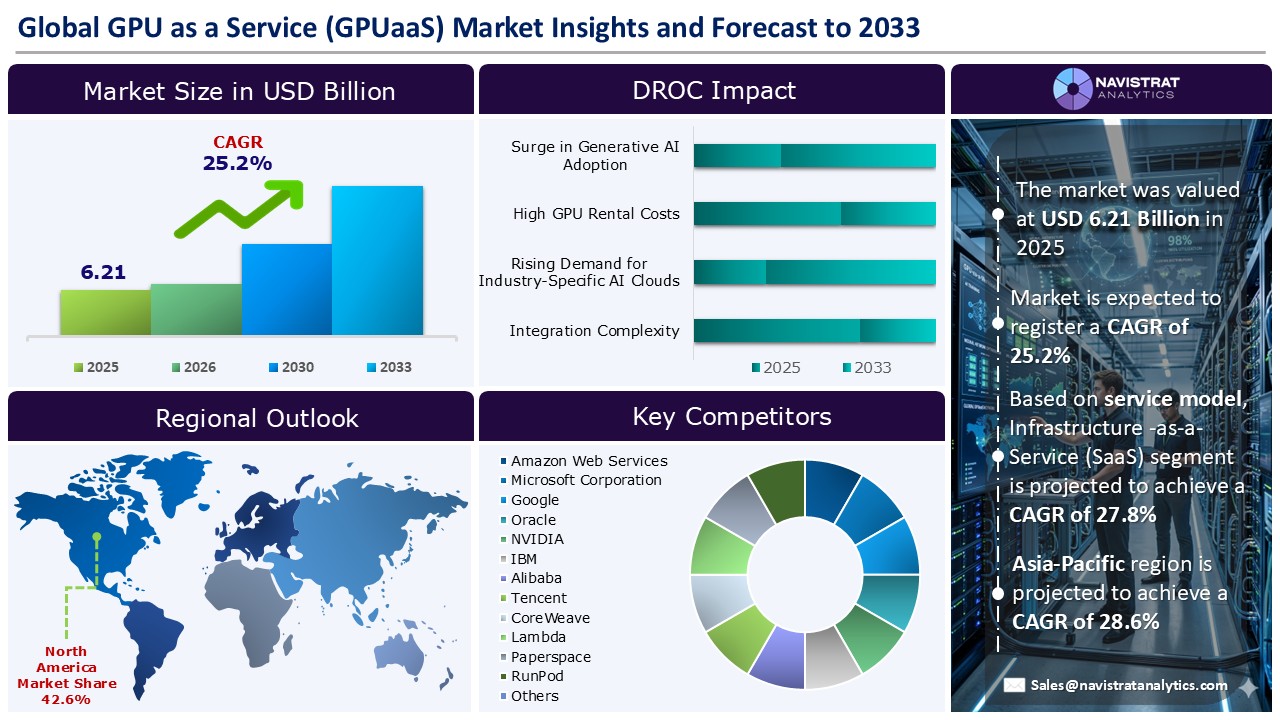

The global GPU as a Service (GPUaaS) market reached USD 6.21 billion in 2025 and is expected to register a revenue CAGR of 25.2% during the forecast period. Surge in generative AI adoption, rising cloud migration, increasing expansion of cloud gaming, and growth of High-Performance Computing (HPC) workloads are expected to drive revenue growth of the market.

Market Drivers:

Surge in generative AI adoption is driving strong revenue growth of the market. The transition of generative AI from experimental research laboratories into widespread enterprise production environments has created an unprecedented deficit in global compute supply. Generative models, particularly advanced multimodal transformers, fundamentally rely on massive parallel processing capabilities to execute matrix multiplications and tensor calculations across petabytes of unstructured data. AI workloads require distinct, resource-intensive phases. The initial model training, which demands thousands of interconnected GPUs operating continuously for months, and the subsequent inference phase, which requires ultra-low-latency processing to deliver real-time user interactions. The ROI of these AI tools has been unequivocally validated across enterprise sectors, generating 5–10x returns on productivity, which entirely justifies the continuous acquisition of cloud-compute hours despite premium hourly rates.

In November 2025, cloud provider Lambda reached a landmark multibillion-dollar agreement with Microsoft to deploy massive AI infrastructure powered by tens of thousands of NVIDIA GPUs. This unprecedented capacity expansion was specifically orchestrated to alleviate the severe compute bottlenecks experienced by generative AI developers. Furthermore, in October 2025, NVIDIA announced the rollout of specialized GPUaaS instances powered by its next-generation Blackwell architecture in collaboration with major hyperscalers. These new instances are engineered specifically to accelerate LLM training and AI inference, promising up to a 2× performance improvement over prior-generation A100 and H100 instances.

Market Opportunity:

Rising demand for industry-specific AI clouds is creating significant opportunities for the market. Organizations in highly regulated, data-intensive verticals, such as healthcare, biotechnology, financial services, and autonomous automotive engineering, are increasingly demanding specialized GPU environments tailored to their unique compliance frameworks, latency tolerances, and algorithmic structures. This specialization requires GPUaaS providers to move beyond raw hardware rentals and integrate sophisticated platform-as-a-service (PaaS) layers that include sovereign data residency controls, HIPAA/GDPR-compliant orchestration, and pre-configured industry models. For example, the financial sector requires extreme low-latency inference for high-frequency trading and fraud detection, whereas the healthcare sector demands massive parallel processing for genomic sequencing and protein folding simulations.

In October 2025, pharmaceutical giant Eli Lilly and Company announced a historic collaboration with NVIDIA to construct an “AI factory”—an industry-specific supercomputing infrastructure designed explicitly to manage the rigorous demands of pharmaceutical research. Powered by over 1,000 next-generation B300 GPUs connected via a unified networking fabric, this specialized deployment allows biomedical researchers to rapidly iterate complex molecular simulations and accelerate drug discovery workflows at an unprecedented scale. Forward-looking insights suggest that the proliferation of these customized clouds will allow specialized GPUaaS operators (neoclouds) to secure highly profitable, enduring niches.

Recent Trends:

Rapid adoption of Next-Generation AI GPUs has emerged as a key technological trend in the GPU as a Service (GPUaaS) market. As the computational complexity of deep learning models scales exponentially, legacy silicon architectures are rapidly becoming obsolete, prompting a massive, industry-wide hardware refresh cycle across global data centers. Next-generation GPUs—characterized by substantially larger High Bandwidth Memory (HBM) capacities, advanced tensor core configurations, and highly optimized power usage effectiveness (PUE)—are critical for maintaining the economic viability of cloud inferencing at scale.

This trend is evidenced by aggressive hardware deployments from the dominant semiconductor manufacturers, which are fundamentally diversifying the supply chain and driving down the cost-per-flop for end users. In March 2025, Google Cloud significantly advanced the market by introducing comprehensive support for NVIDIA Blackwell GPUs within its AI Hypercomputer architecture, an infrastructure specifically engineered to accelerate large-scale generative AI workloads with unprecedented energy efficiency. The integration of the Blackwell architecture enables developers to process foundational models with significantly reduced latency compared to previous Hopper-class generations

Restraints & Challenges:

High GPU rental costs, severely exacerbated by systemic supply chain constraints, constitute a formidable restraint impeding the broader democratization and revenue growth of the market. The fundamental bottleneck originates not merely in standard silicon manufacturing, but in the highly complex advanced packaging of High Bandwidth Memory (HBM) required for AI accelerators. Because global HBM production capacity remains constrained, the output of high-end GPUs is fundamentally misaligned with the explosive demand from hyperscalers, AI startups, and research institutions.

This enduring scarcity dynamic has resulted in severe inflationary pressure on cloud compute pricing. It creates an environment where access to state-of-the-art models is increasingly dictated by capital availability rather than innovation. By the end of 2026, it is expected that GPU rental prices will have skyrocketed, with pricing for latest-generation chips surging by 48% in a matter of months. Specifically, the rental cost for highly sought-after NVIDIA Blackwell chips hit an exorbitant $4.08 per hour. To capitalize on this leverage and manage constrained inventory, major neocloud providers such as CoreWeave aggressively raised baseline prices by 20% and extended minimum contract durations from one year to an inflexible three-year commitment.

Service Model Segment Insights and Analysis:

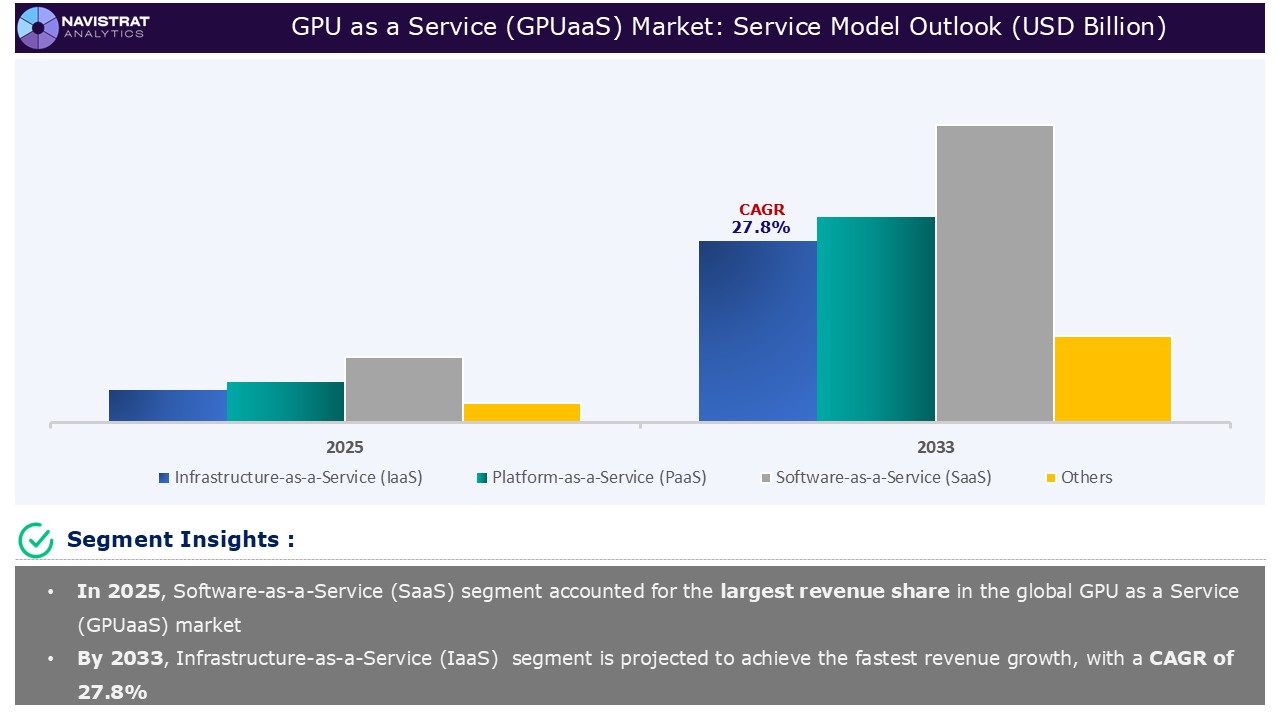

Based on service model, the GPU as a Service (GPUaaS) market is segmented into Infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), Software-as-a-Service (SaaS) and others.

Software-as-a-Service (SaaS) segment contributed the largest share in 2025 due to due to the rising demand for ready-to-use AI applications, cloud-based rendering platforms, and advanced analytics solutions that eliminate the need for enterprises to manage complex GPU infrastructure internally. Businesses across healthcare, BFSI, media, gaming, and manufacturing increasingly prefer SaaS-based GPU solutions for applications such as computer vision, natural language processing, fraud detection, 3D rendering, video processing, and predictive analytics because these platforms offer faster deployment, lower upfront investment, simplified operations, and subscription-based pricing. The rapid adoption of generative AI tools and enterprise AI copilots is further accelerating demand for GPU-backed SaaS offerings.

Recent developments strongly support the revenue growth of this segment, particularly as enterprises shift toward managed AI platforms instead of raw infrastructure consumption. In April 2025, for instance, Google Cloud reported that Vertex AI usage increased 20x year-over-year, driven by rapid adoption of Gemini, Imagen, and Veo models, with over four million developers building on Gemini. This reflects rising enterprise demand for ready-to-use GPU-backed AI SaaS platforms rather than self-managed GPU infrastructure. In March 2024, NVIDIA launched NVIDIA NIM microservices. This significantly expanded SaaS-layer monetization by allowing enterprises to deploy GPU-powered applications without managing backend infrastructure.

Component Segment Insights and Analysis:

Based on component, the GPU as a Service (GPUaaS) market is segmented into solutions and services. Solutions segment is further sub-segmented into GPU virtualization software, GPU orchestration platforms, AI/ML acceleration platforms, and GPU resource management tools. Services systems is further sub-segmented into managed services and professional services.

Solutions segment contributed the largest share in 2025 due to the escalating enterprise imperative to deploy highly scalable hardware platforms capable of executing advanced AI training protocols, complex deep learning algorithms, and high-throughput real-time inference workloads. As organizations transition from isolated experimentation to production-grade AI integration, the demand for sophisticated, out-of-the-box solutions has surged. These solutions now heavily feature Kubernetes-based GPU orchestration and containerized deployment frameworks. It abstracts the profound technical complexity of managing distributed parallel compute nodes.

In May 2025, NVIDIA executed a critical strategic development with the launch of DGX Cloud Lepton. It is a comprehensive component solution that operates as a global AI compute platform and unified marketplace. This innovative solution fundamentally restructures cloud consumption by connecting developers directly with a vast, interoperable network of GPU resources spanning multiple diverse cloud partners. This development significantly drives the revenue growth of the solutions segment by providing a turnkey, frictionless environment. Data scientists can immediately initiate massive model training without the burdensome necessity of configuring underlying networking layers or complex CUDA drivers.

Application Segment Insights and Analysis:

Based on application, the GPU as a Service (GPUaaS) market is segmented into Artificial Intelligence & Machine Learning (AI/ML), High-Performance Computing (HPC), data analytics & big data, rendering & visualization, cloud gaming, blockchain & cryptography, Edge AI / IoT processing and others.

Artificial Intelligence & Machine Learning (AI/ML) segment contributed the largest share in 2025 due to the direct and unavoidable consequence of the global, multi-industry AI arms race. Modern artificial intelligence depends heavily on GPUs at every stage of development. Huge amounts of data such as text, images, videos, and audio must first be collected, cleaned, and processed. This requires strong parallel computing power, which GPUs provide efficiently. During the training phase, large AI models with billions of parameters need months of continuous computation, and GPUs make this possible by handling many tasks at the same time. Even after training, real-time inferencing also relies on GPUs for fast and low-latency performance. This is why GPUs have become the core foundation of the entire AI lifecycle.

In October 2025, a critical strategic advancement occurred when major hyperscalers, in close collaboration with NVIDIA, rolled out highly anticipated GPUaaS instances powered by the advanced Blackwell architecture. These next-generation instances are specifically engineered to accelerate complex LLM training and high-volume AI inference, delivering up to a 2× performance enhancement over the prior A100 and P5 instance generations.

Geographical Outlook:

GPU as a Service (GPUaaS) market is strategically segmented by geography to provide a comprehensive understanding of regional market dynamic. Discover demand analysis, emerging trends, and growth opportunities shaping market performance across different region and countries.

North America GPU as a Service (GPUaaS) Market:

Market in North America accounted for largest revenue share in 2025 due to the deeply entrenched cloud infrastructure ecosystem, unparalleled venture capital investment flowing into AI startups, and the physical headquarters of global hyperscalers and semiconductor innovators such as AWS, Google, Microsoft, NVIDIA, and AMD in the region. The region heavily leverages dense data-center corridors in Virginia, Texas, and Oregon, supported by robust fiber backbones and access to critical energy grids.

A key growth driver is the aggressive modernization of federal IT and critical academic research infrastructure. The U.S. government has prioritized the democratization of compute capabilities through national initiatives like the National Artificial Intelligence Research Resource (NAIRR). Following a highly successful two-year pilot phase, the National Science Foundation formally announced a USD 35 million investment in September 2025 to establish a sustained NAIRR Operations Center, significantly expanding academic access to cloud GPU resources and bypassing commercial bottlenecks.

Investment trends strongly favor massive hyperscale expansions and localized edge buildouts to support this demand. In November 2025, Anthropic committed a staggering USD 50 billion toward constructing massive AI data centers across Texas and New York, strategically utilizing vendors like Fluidstack for massive GPU cluster orchestration. Furthermore, the establishment of “CoreWeave Federal” exemplifies the strategic pivot toward secure, FedRAMP-authorized sovereign cloud environments tailored specifically for U.S. government intelligence and defense workloads, effectively cementing North America’s position as the dominant global compute hub for the foreseeable future.

Asia Pacific GPU as a Service (GPUaaS) Market:

Asia Pacific is expected to register a fast revenue growth rate during the forecast period due to the aggressive national digital transformation mandates, soaring localized AI model development, and increasingly rigid data sovereignty laws that mandate the domestic processing of citizen data. Countries such as China, India, Japan, and South Korea are heavily subsidizing the rapid construction of massive intelligent computing networks to rival Western technological capabilities. In addition, Government initiatives are completely reshaping the infrastructure landscape. In China, the government has aggressively advanced its “East Data, West Computing” initiative, constructing a highly integrated optical network spanning over 1,200 miles that connects coastal tech hubs to energy-rich inland data centers with a reported 98% efficiency rate.

Strategic developments highlight the influx of immense private capital matching government ambition. In November 2025, GMI Cloud announced a USD 500 million investment to build an advanced AI data center in Taiwan, uniquely designed to house 7,000 NVIDIA Blackwell GB300 GPUs. Concurrently, Japanese cloud providers secured significant Ministry of Economy, Trade and Industry (METI) funding to deploy sovereign cloud capabilities that meet strict national Power Usage Effectiveness (PUE) mandates. This synchronized expansion of both public and private infrastructure guarantees robust, sustained revenue growth across the Asia Pacific market.

Europe GPU as a Service (GPUaaS) Market:

Market in Europe accounted for a significant revenue share in 2025 due to stringent data privacy regulations (such as GDPR and the sweeping NIS2 directive) and a profound strategic geopolitical imperative to establish technological sovereignty. European governments and major enterprises are actively pivoting away from a total reliance on US-based hyperscalers. It is fostering the rapid development of localized “sovereign clouds” in France, Germany, and the Nordics to ensure critical data remains within EU borders.

In addition, the revenue growth is heavily subsidized by complex public-private partnerships driven by the European Union. The European High Performance Computing Joint Undertaking (EuroHPC JU) serves as the primary catalyst for regional AI infrastructure. In 2025, EuroHPC launched its highly ambitious “AI Factories” initiative, providing customized, subsidized supercomputing access to European startups and SMEs to prevent brain drain to Silicon Valley.

Following the successful activation of the HammerHAI AI Factory in April 2025, the EuroHPC JU officially approved six additional factory sites across Czechia, Lithuania, the Netherlands, Poland, Romania, and Spain in October 2025. It brings the total to 19 heavily subsidized computing hubs across the continent. These initiatives structurally alter the regional market by supplying high-performance GPUaaS directly to scientific and industrial communities at subsidized or completely free-of-charge rates for innovation purposes.

Competition Analysis:

The GPU as a Service (GPUaaS) market is characterized by a consolidated structure, with few players competing across various segments and regions. List of major players included in the GPU as a Service (GPUaaS) market report are:

- Amazon Web Services

- Microsoft Corporation

- Oracle

- NVIDIA

- IBM

- Alibaba

- Tencent

- CoreWeave

- Lambda

- Paperspace

- RunPod

- Vast.ai

- HCL Technologies

- Vultr

Strategic Developments in GPU as a Service (GPUaaS) Market:

- In November 2025, Lambda AI, an AI company that provides high-performance GPU cloud computing, announced a multi-billion-dollar partnership with Microsoft to build large-scale AI infrastructure using tens of thousands of GPUs from NVIDIA, including advanced GB300 NVL72 systems. This long-term collaboration marks a major expansion of NVIDIA-powered cloud computing capacity, aimed at increasing availability of high-performance AI infrastructure. The agreement also reflects the rapidly rising global demand for accelerated computing, fueled by growing adoption of AI assistants and expanding enterprise AI deployments.

- In October 2025, Oracle and AMD have expanded their long-standing, multi-generation partnership to accelerate large-scale AI adoption. As part of this collaboration, Oracle Cloud Infrastructure (OCI) will serve as a launch partner for one of the first publicly accessible AI superclusters powered by AMD Instinct MI450 Series GPUs. The deployment is expected to begin with around 50,000 GPUs in the third quarter of 2026, with further expansion planned in 2027 and beyond. This initiative builds on the companies’ earlier collaboration to deliver AMD Instinct GPU solutions on OCI, including the rollout of MI300X-based compute instances for enterprise AI workloads.

Key Advantages for Stakeholders:

Navistrat Analytics’ industry report provides an in-depth quantitative analysis of various market segments, historical and current trends, market forecasts, and dynamics within the global market. The historical years covered in this report are 2023 to 2024, with 2025 serving as the base year for market size calculations. The forecast period extends from 2026 to 2033.

The report includes an executive summary and a comprehensive overview of market drivers, restraints, opportunities, and challenges (DROC), along with insights into regulatory standards. It features detailed analyses such as PORTER’s Five Forces, SWOT, and PESTLE, as well as assessments of technological trends and the competitive landscape.

PORTER’s Five Forces analysis helps stakeholders evaluate the impact of new entrants, competitive rivalry, supplier power, buyer power, and substitution threats, enabling them to assess the level of competition and the attractiveness of the global market. The competitive landscape provides stakeholders with a clear understanding of the current market positions of key players, offering valuable insights into their competitive environment.

Scope And Key Highlights of The GPU as a Service (GPUaaS) Market Report:

| Report Features | Details |

| Market Size in 2025 | USD 6.21 Billion |

| Market Growth Rate in CAGR (2026–2033) | 25.2% |

| Market Revenue Forecast to 2033 | USD 36.77 Billion |

| Base year | 2025 |

| Historical year | 2023–2024 |

| Forecast period | 2026–2033 |

| Report Pages | 450 |

| Segments Covered |

|

| Regional scope |

|

| Country Scope |

|

| Key Market Players |

|

| Delivery Format | Reports are delivered in PDF format via email. |

| Customization scope | Request Customization |

The GPU as a Service (GPUaaS) market report offers a detailed analysis of market size, including historical revenue (in USD Billion) data for 2023-2024 and revenue forecasts for 2026-2033 across the following segments:

- Service Model Outlook (Revenue, USD Billion; 2023-2033)

- Infrastructure-as-a-Service (IaaS)

- Platform-as-a-Service (PaaS)

- Software-as-a-Service (SaaS)

- Others

- Component Outlook (Revenue, USD Billion; 2023-2033)

- Solution

- GPU Virtualization Software

- GPU Orchestration Platforms

- AI/ML Acceleration Platforms

- GPU Resource Management Tools

- Services

- Managed services

- Professional services

- Solution

- Deployment Outlook (Revenue, USD Billion; 2023-2033)

- Public Cloud

- Private Cloud

- Hybrid Cloud

- GPU Type Outlook (Revenue, USD Billion; 2023-2033)

- Virtual GPU (vGPU)

- Dedicated GPU

- Hybrid GPU

- Bare Metal GPU

- Pricing Model Outlook (Revenue, USD Billion; 2023-2033)

- Pay-as-you-go

- Subscription-Based

- Spot / Preemptible Pricing

- Enterprise Licensing

- Application Outlook (Revenue, USD Billion; 2023-2033)

- Artificial Intelligence & Machine Learning

- High-Performance Computing (HPC)

- Data Analytics & Big Data

- Rendering & Visualization

- Cloud Gaming

- Blockchain & Cryptography

- Edge AI / IoT Processing

- Others

- Industry Vertical (Revenue, USD Billion; 2023-2033)

- IT & telecom

- BFSI

- Media and Entertainment

- Gaming

- Automotive

- Healthcare and Life Sciences

- Retail & E-commerce

- Government & Defense

- Others

- Regional Outlook (Revenue, USD Billion; 2023-2033)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Oceania

- ASEAN Countries

- Rest of APAC

- Latin America

- Brazil

- Rest of LATAM

- Middle East & Africa

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of MEA

- North America

Frequently Asked Questions (FAQ) about the GPU as a Service (GPUaaS) Market Report

The GPU as a Service (GPUaaS) market size was USD 6.21 billion in 2025.

The GPU as a Service (GPUaaS) market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 25.2% during the forecast period.

Surge in generative AI adoption, rising cloud migration, increasing expansion of cloud gaming, and growth of High-Performance Computing (HPC) workloads are the key drivers of the GPU as a Service (GPUaaS) market revenue growth.

High GPU rental costs, data security concerns, and supply chain constraints are key factors restraining revenue growth of the market.

Asia Pacific is expected to account for the fastest revenue growth of 28.6%.

Software-as-a-Service (SaaS) segment is the leading segment of GPU as a Service (GPUaaS) market in terms of service model.

- Market Definition

- Research Objective

- Research Methodology

- Research Design

- Data Collection Methods

- Primary

- Secondary

- Market Size Estimation

- Top-down method

- Bottom-up method

- Forecasting Methodology

- Tools and Models Used

- Market Overview and Trends

- Market Size and Forecast

- Industry Analysis

- Market Driver, Restraints, Opportunity and Challenges (DROC) Analysis

- Market Drivers

- Surge in Generative AI Adoption

- Rising Cloud Migration

- Increasing Expansion of Cloud Gaming

- Growth of High-Performance Computing (HPC) Workloads

- Market Restraints

- High GPU Rental Costs

- Data Security Concerns

- Supply Chain Constraints

- Market Opportunities

- Rising Demand for Industry-Specific AI Clouds

- Sovereign AI Infrastructure Development

- Edge AI and 5G-Driven GPUaaS

- Market Challenges

- Vendor Dependency and Lock-In Risk

- Integration Complexity

- Regulatory Landscape

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

- Strategic Insights

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Price Trend Analysis

- Value Chain Analysis

- Technological Trends

- Edge and Distributed GPU Compute

- Adoption of Next-Generation AI GPUs

- Containerized and Kubernetes-Based GPU Orchestration

- Confidential Computing and GPU Security Isolation

- Resource Optimization Through Multi-Instance GPU (MIG) and Partitioning

- Recent Developments

- Funding

- Merger and Acquisition

- Expansion

- Partnership and Collaboration

- Product/ Service Launch

- GPU Type Market Revenue Estimates and Forecasts, 2023-2033

- Virtual GPU (vGPU)

- Dedicated GPU

- Hybrid GPU

- Bare Metal GPU

- Service Model Market Revenue Estimates and Forecasts, 2023-2033

- Infrastructure-as-a-Service (IaaS)

- Platform-as-a-Service (PaaS)

- Software-as-a-Service (SaaS)

- Others

- Deployment Market Revenue Estimates and Forecasts, 2023-2033

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Component Market Revenue Estimates and Forecasts, 2023-2033

- Solutions

- GPU Virtualization Software

- GPU Orchestration Platforms

- AI/ML Acceleration Platforms

- GPU Resource Management Tools

- Services

- Managed services

- Professional services

- Solutions

- Pricing Model Market Revenue Estimates and Forecasts, 2023-2033

- Pay-as-you-go

- Subscription-Based

- Spot / Preemptible Pricing

- Enterprise Licensing

- Application Market Revenue Estimates and Forecasts, 2023-2033

- Artificial Intelligence & Machine Learning

- High-Performance Computing (HPC)

- Data Analytics & Big Data

- Rendering & Visualization

- Cloud Gaming

- Blockchain & Cryptography

- Edge AI / IoT Processing

- Others

- Industry Vertical Market Revenue Estimates and Forecasts, 2023-2033

- IT & telecom

- BFSI

- Media and Entertainment

- Gaming

- Automotive

- Healthcare and Life Sciences

- Retail & E-commerce

- Government & Defense

- Others

- GPU as a Service (GPUaaS) Market Revenue Estimates and Forecasts by Region, 2023-2033, USD Billion

- North America

- North America GPU as a Service (GPUaaS) Market By Component, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Solution

- GPU Virtualization Software

- GPU Orchestration Platforms

- AI/ML Acceleration Platforms

- GPU Resource Management Tools

- Services

- Managed services

- Professional services

- Solution

- North America GPU as a Service (GPUaaS) Market By GPU Type, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Virtual GPU (vGPU)

- Dedicated GPU

- Hybrid GPU

- Bare Metal GPU

- North America GPU as a Service (GPUaaS) Market By Deployment, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Public Cloud

- Private Cloud

- Hybrid Cloud

- North America GPU as a Service (GPUaaS) Market By Service Model, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Infrastructure-as-a-Service (IaaS)

- Platform-as-a-Service (PaaS)

- Software-as-a-Service (SaaS)

- Others

- North America GPU as a Service (GPUaaS) Market By Pricing Model, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Pay-as-you-go

- Subscription-Based

- Spot / Preemptible Pricing

- Enterprise Licensing

- North America GPU as a Service (GPUaaS) Market By Application, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Artificial Intelligence & Machine Learning

- High-Performance Computing (HPC)

- Data Analytics & Big Data

- Rendering & Visualization

- Cloud Gaming

- Blockchain & Cryptography

- Edge AI / IoT Processing

- Others

- North America GPU as a Service (GPUaaS) Market By Industry Vertical, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- IT & telecom

- BFSI

- Media and Entertainment

- Gaming

- Automotive

- Healthcare and Life Sciences

- Retail & E-commerce

- Government & Defense

- Others

- North America GPU as a Service (GPUaaS) Market Revenue Estimates and Forecasts by Country, 2023-2033, USD Billion

- United States

- Canada

- Mexico

- North America GPU as a Service (GPUaaS) Market By Component, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Europe

- Europe GPU as a Service (GPUaaS) Market By Component, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Solution

- GPU Virtualization Software

- GPU Orchestration Platforms

- AI/ML Acceleration Platforms

- GPU Resource Management Tools

- Services

- Managed services

- Professional services

- Solution

- Europe GPU as a Service (GPUaaS) Market By GPU Type, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Virtual GPU (vGPU)

- Dedicated GPU

- Hybrid GPU

- Bare Metal GPU

- Europe GPU as a Service (GPUaaS) Market By Deployment, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Europe GPU as a Service (GPUaaS) Market By Service Model, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Infrastructure-as-a-Service (IaaS)

- Platform-as-a-Service (PaaS)

- Software-as-a-Service (SaaS)

- Others

- Europe GPU as a Service (GPUaaS) Market By Pricing Model, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Pay-as-you-go

- Subscription-Based

- Spot / Preemptible Pricing

- Enterprise Licensing

- Europe GPU as a Service (GPUaaS) Market By Application, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Artificial Intelligence & Machine Learning

- High-Performance Computing (HPC)

- Data Analytics & Big Data

- Rendering & Visualization

- Cloud Gaming

- Blockchain & Cryptography

- Edge AI / IoT Processing

- Others

- Europe GPU as a Service (GPUaaS) Market By Industry Vertical, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- IT & telecom

- BFSI

- Media and Entertainment

- Gaming

- Automotive

- Healthcare and Life Sciences

- Retail & E-commerce

- Government & Defense

- Others

- Europe GPU as a Service (GPUaaS) Market Revenue Estimates and Forecasts by Country, 2023-2033, USD Billion

- Germany

- United Kingdom

- France

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Europe GPU as a Service (GPUaaS) Market By Component, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Asia-Pacific

- Asia-Pacific GPU as a Service (GPUaaS) Market By Component, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Solution

- GPU Virtualization Software

- GPU Orchestration Platforms

- AI/ML Acceleration Platforms

- GPU Resource Management Tools

- Services

- Managed services

- Professional services

- Solution

- Asia-Pacific GPU as a Service (GPUaaS) Market By GPU Type, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Virtual GPU (vGPU)

- Dedicated GPU

- Hybrid GPU

- Bare Metal GPU

- Asia-Pacific GPU as a Service (GPUaaS) Market By Deployment, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Asia-Pacific GPU as a Service (GPUaaS) Market By Service Model, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Infrastructure-as-a-Service (IaaS)

- Platform-as-a-Service (PaaS)

- Software-as-a-Service (SaaS)

- Others

- Asia-Pacific GPU as a Service (GPUaaS) Market By Pricing Model, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Pay-as-you-go

- Subscription-Based

- Spot / Preemptible Pricing

- Enterprise Licensing

- Asia-Pacific GPU as a Service (GPUaaS) Market By Application, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Artificial Intelligence & Machine Learning

- High-Performance Computing (HPC)

- Data Analytics & Big Data

- Rendering & Visualization

- Cloud Gaming

- Blockchain & Cryptography

- Edge AI / IoT Processing

- Others

- Asia-Pacific GPU as a Service (GPUaaS) Market By Industry Vertical, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- IT & telecom

- BFSI

- Media and Entertainment

- Gaming

- Automotive

- Healthcare and Life Sciences

- Retail & E-commerce

- Government & Defense

- Others

- Asia-Pacific GPU as a Service (GPUaaS) Market Revenue Estimates and Forecasts by Country, 2023-2033, USD Billion

- China

- India

- Japan

- South Korea

- Oceania

- ASEAN Countries

- Rest of Asia-Pacific

- Asia-Pacific GPU as a Service (GPUaaS) Market By Component, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Latin America

- Latin America GPU as a Service (GPUaaS) Market By Component, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Solution

- GPU Virtualization Software

- GPU Orchestration Platforms

- AI/ML Acceleration Platforms

- GPU Resource Management Tools

- Services

- Managed services

- Professional services

- Solution

- Latin America GPU as a Service (GPUaaS) Market By GPU Type, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Virtual GPU (vGPU)

- Dedicated GPU

- Hybrid GPU

- Bare Metal GPU

- Latin America GPU as a Service (GPUaaS) Market By Deployment, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Latin America GPU as a Service (GPUaaS) Market By Service Model, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Infrastructure-as-a-Service (IaaS)

- Platform-as-a-Service (PaaS)

- Software-as-a-Service (SaaS)

- Others

- Latin America GPU as a Service (GPUaaS) Market By Pricing Model, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Pay-as-you-go

- Subscription-Based

- Spot / Preemptible Pricing

- Enterprise Licensing

- Latin America GPU as a Service (GPUaaS) Market By Application, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Artificial Intelligence & Machine Learning

- High-Performance Computing (HPC)

- Data Analytics & Big Data

- Rendering & Visualization

- Cloud Gaming

- Blockchain & Cryptography

- Edge AI / IoT Processing

- Others

- Latin America GPU as a Service (GPUaaS) Market By Industry Vertical, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- IT & telecom

- BFSI

- Media and Entertainment

- Gaming

- Automotive

- Healthcare and Life Sciences

- Retail & E-commerce

- Government & Defense

- Others

- Latin America GPU as a Service (GPUaaS) Market Revenue Estimates and Forecasts by Country, 2023-2033, USD Billion

- Brazil

- Rest of Latin America

- Latin America GPU as a Service (GPUaaS) Market By Component, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Middle East & Africa

- Middle East & Africa GPU as a Service (GPUaaS) Market By Component, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Solution

- GPU Virtualization Software

- GPU Orchestration Platforms

- AI/ML Acceleration Platforms

- GPU Resource Management Tools

- Services

- Managed services

- Professional services

- Solution

- Middle East & Africa GPU as a Service (GPUaaS) Market By GPU Type, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Virtual GPU (vGPU)

- Dedicated GPU

- Hybrid GPU

- Bare Metal GPU

- Middle East & Africa GPU as a Service (GPUaaS) Market By Deployment, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Middle East & Africa GPU as a Service (GPUaaS) Market By Service Model, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Infrastructure-as-a-Service (IaaS)

- Platform-as-a-Service (PaaS)

- Software-as-a-Service (SaaS)

- Others

- Middle East & Africa GPU as a Service (GPUaaS) Market By Pricing Model, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Pay-as-you-go

- Subscription-Based

- Spot / Preemptible Pricing

- Enterprise Licensing

- Middle East & Africa GPU as a Service (GPUaaS) Market By Application, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Artificial Intelligence & Machine Learning

- High-Performance Computing (HPC)

- Data Analytics & Big Data

- Rendering & Visualization

- Cloud Gaming

- Blockchain & Cryptography

- Edge AI / IoT Processing

- Others

- Middle East & Africa GPU as a Service (GPUaaS) Market By Industry Vertical, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- IT & telecom

- BFSI

- Media and Entertainment

- Gaming

- Automotive

- Healthcare and Life Sciences

- Retail & E-commerce

- Government & Defense

- Others

- Middle East & Africa GPU as a Service (GPUaaS) Market Revenue Estimates and Forecasts by Country, 2023-2033, USD Billion

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of Middle East & Africa

- Middle East & Africa GPU as a Service (GPUaaS) Market By Component, Market Revenue Estimates and Forecasts, 2023-2033, USD Billion

- Market Share Analysis

- Revenue Market Share by Key Players (2025-2026)

- Analysis of Top Players by Market Presence

- Competitive Matrix

- Competitive Strategies

- Mergers and Acquisitions

- Partnerships and Collaboration

- Investment and Fundings

- Agreement

- Expansion

- New Product/ Services Launches

- Technological Innovations

- Microsoft Corporation

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- Amazon Web Services

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- Google

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- Oracle

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- NVIDIA

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- IBM

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- Alibaba

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- Tencent

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- CoreWeave

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- Lambda AI

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- Paperspace

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- RunPod

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- Vast.ai

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- HCL Technologies

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis

- Vultr

- Company Overview

- Financial Insights

- Product/ Services Component

- Strategic Developments

- SWOT Analysis