Advanced Driver Assistance Systems (ADAS) Market Overview and Key Insights:

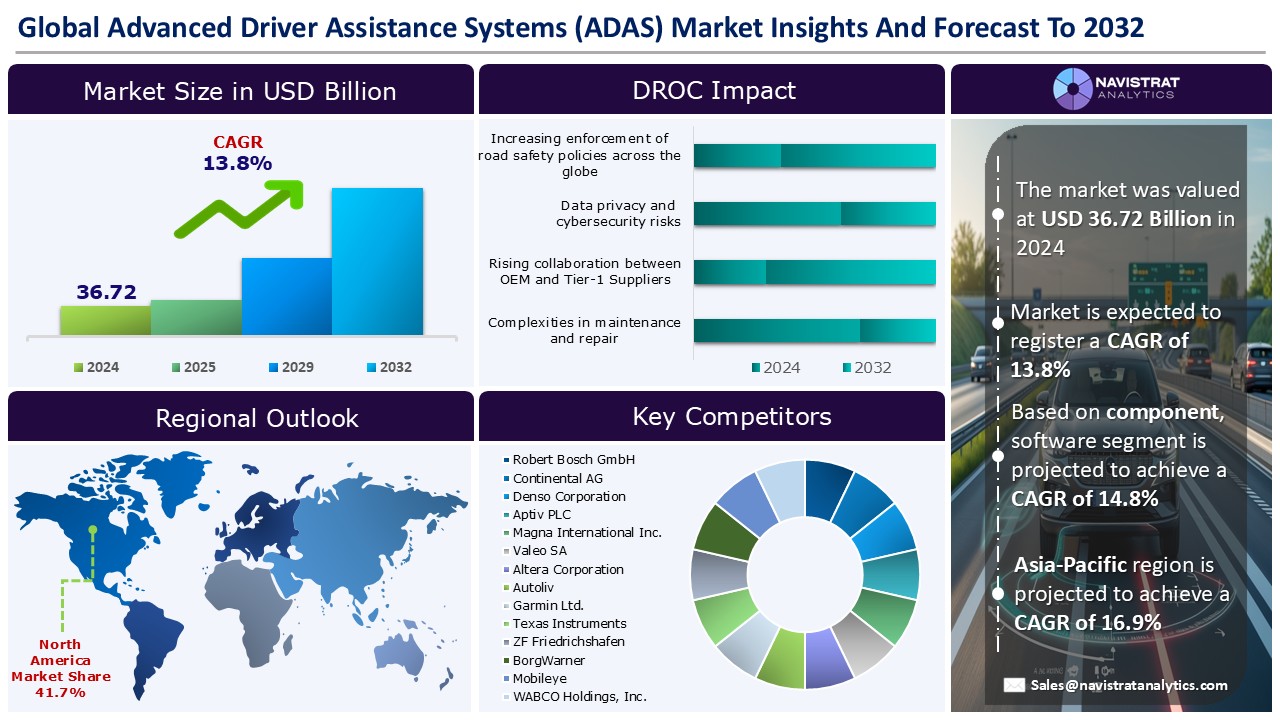

The global Advanced Driver Assistance Systems (ADAS) market reached USD 36.72 billion in 2024 and is expected to register a revenue CAGR of 13.8% during the forecast period. Increasing enforcement of road safety policies across the globe, rising focus on accident prevention, growing expansion of electric and autonomous vehicles, and rising consumer demand for tech-enabled driving experiences are expected to drive revenue growth of the market.

Market Drivers:

Rising focus on accident prevention is the major factor driving revenue growth of the market. According to the World Health Organization (WHO), more than 3,500 individuals lose their lives in road accidents every day. It results in nearly 1.3 million preventable deaths and around 50 million injuries annually. This alarming statistic positions road incidents as the primary cause of mortality among children and young adults across the globe. Current trends indicate that, without significant intervention, road accidents could account for an additional 13 million deaths and 500 million injuries over the next decade. As a result, governments are implementing stricter vehicle safety regulations, and consumers are increasingly prioritizing safety features in their vehicle purchase decisions. These developments are pushing automakers to adopt ADAS technologies and driving revenue growth of the market.

The growing consumer awareness and demand for enhanced vehicle safety are prompting automakers to incorporate ADAS technologies across a broader range of vehicle models. In April 2024, Mobileye announced that it had delivered the initial production-ready hardware and software for its new EyeQ6 Lite system-on-chip to customers. This technology will allow Advanced Driver-Assistance Systems (ADAS) in several vehicle models scheduled for launch. The delivery marks the debut of the EyeQ6 product line, with the EyeQ6L already planned for integration into 46 million vehicles over the coming years, positioning it as a leading ADAS solution for the global automotive industry from the outset.

Market Opportunity:

Rising collaboration between OEM and Tier-1 Suppliers is creating significant opportunities for the market. These strategic partnerships allow seamless integration of advanced hardware components, such as sensors, radar, and LiDAR, with sophisticated software platforms, resulting in more robust and scalable ADAS solutions. This collaborative ecosystem reduces development costs and improves regulatory compliance. It drives broader adoption of ADAS across vehicle segments and contributes to market revenue growth.

In January 2025, Trimble announced an expansion of its technology partnership with Qualcomm Technologies, Inc. to provide high-precision positioning solutions for a wide range of automated vehicles, including passenger cars and heavy-duty trucks. This integration is designed to support Level 2+ and potentially higher levels of automated driving applications by providing accurate positioning for advanced Driver Assistance Systems (ADAS) and Cellular Vehicle-To-Everything (C-V2X) technologies, targeting both automakers and Tier-1 suppliers.

Recent Trends:

One recent trend in the Advanced Driver Assistance Systems (ADAS) market is the integration of AI and machine learning to increase ADAS Capabilities. These technologies enhance the real-time processing of data from various sensors. It allows more accurate object detection, predictive analytics, and adaptive decision-making. For instance, AI-powered algorithms can process vast amounts of sensor data, improving object recognition, path planning, and collision avoidance. The demand for AI-integrated ADAS features is not limited to luxury vehicles. It is also increasingly prevalent in mid-range and entry-level models.

In April 2024, for instance, Helm.ai, a leading developer of advanced AI software for ADAS, autonomous driving, and robotics automation, introduced neural network-based, high-fidelity virtual scenario generation models for perception simulation. This advanced technology strengthens the company’s portfolio of AI-driven solutions designed to support the development of sophisticated ADAS at Levels 2 and 3, as well as Level 4 autonomous driving systems.

Restraints & Challenges:

Data privacy and cybersecurity risks pose a significant challenge to the Advanced Driver Assistance Systems (ADAS) market. ADAS technologies rely heavily on real-time data collection, processing, and communication between vehicle systems and external networks. As a result, they become vulnerable to potential cyber threats and data breaches. Concerns over unauthorized access to sensitive information, such as location data, driving patterns, and vehicle control systems, have prompted regulatory scrutiny and heightened consumer apprehension. This has led to increased compliance costs for manufacturers.

In February 2024, the U.S. Department of Commerce revealed plans to investigate whether connected vehicle technologies, including ADAS developed by companies linked to China, could threaten national security. The department also sought input from industry stakeholders regarding potential regulations for connected vehicles, including which specific technologies should be targeted. According to a proposed rule released in September, the Commerce Department aims to prohibit the use of vehicle connectivity hardware, software, or automated driving systems that might enable foreign entities, particularly from China and Russia, to access sensitive information or remotely control vehicles.

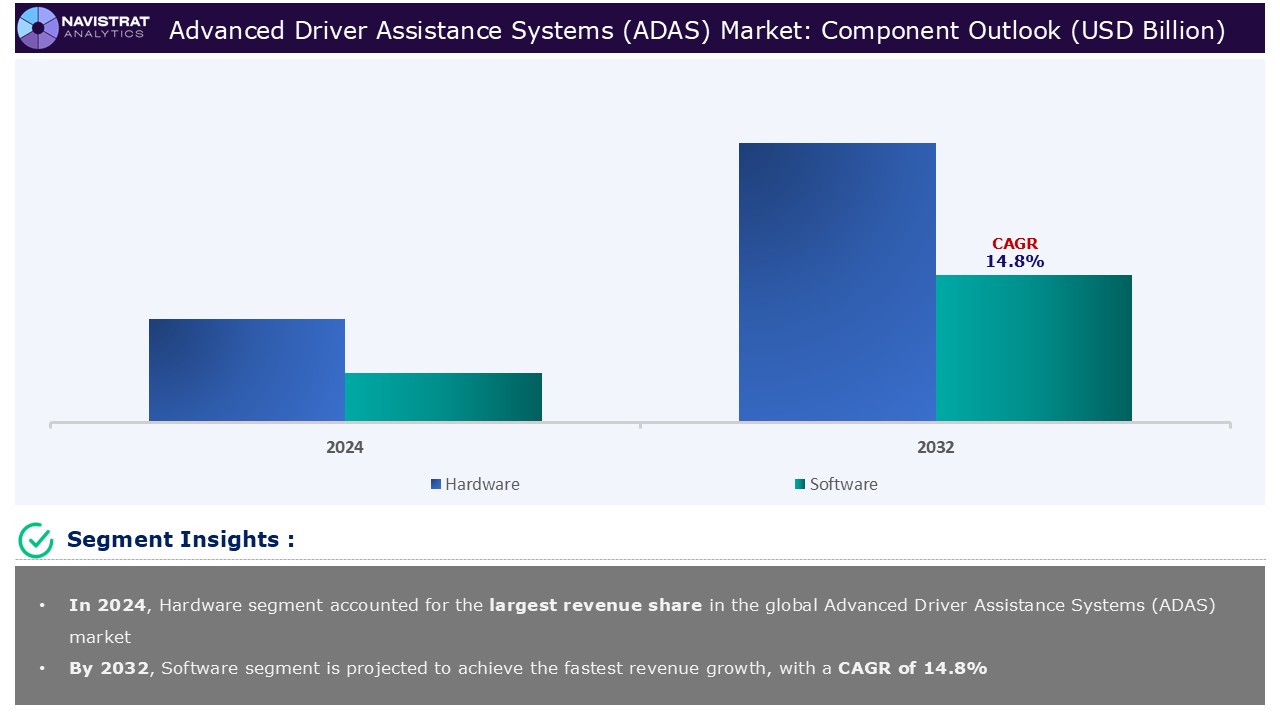

Component Segment Insights and Analysis:

Based on the component, the Advanced Driver Assistance Systems (ADAS) market is segmented into hardware, and software. The hardware segment is further sub-segmented into sensors, Electronic Control Units (ECUs), actuators, display panels and others. Sensors segment is further sub-segmented into radar, lidar, ultrasonic sensors, infrared sensors, and image sensors. Software segment is further sub-segmented into embedded software, AI/ML algorithms, mapping & navigation software, and others.

Hardware segment contributed the largest share in 2024 due to the increasing integration of safety and automation features in modern vehicles. There is a growing demand for hardware components such as radar sensors, LiDAR, ultrasonic sensors, cameras, and Electronic Control Units (ECUs) owing to the stringent safety regulations, consumer preference for enhanced driver assistance functionalities, and the push toward higher levels of vehicle autonomy.

In September 2024, Arbe Robotics Ltd, a leading provider of perception radar solutions, announced that its Tier 1 partner, HiRain Technologies, is fast-tracking the development of an ADAS system for a Chinese automotive manufacturer using Arbe’s radar chipset. The system will feature a fusion of camera and radar technologies. It eliminates the need for LiDAR while still delivering equivalent performance and functionality. Subject to final approval from the OEM, the system is expected to enter mass production by the fourth quarter of 2025.

Function Segment Insights and Analysis:

Based on function, the Advanced Driver Assistance Systems (ADAS) market is segmented into Adaptive Cruise Control (ACC), Automatic Emergency Braking (AEB), Lane Departure Warning (LDW), Lane Keeping Assist System (LKAS), Blind Spot Detection (BSD), Traffic Sign Recognition (TSR), Driver Monitoring Systems (DMS), Forward Collision Warning (FCW), Night Vision Systems (NVS), Park Assist / Automated Parking System, and others.

Adaptive Cruise Control (ACC) segment contributed the largest share in 2024 due to rising consumer demand for better safety, comfort, and convenience during driving. ACC systems automatically adjust vehicle speed to maintain a safe following distance from the vehicle ahead. It reduces driver fatigue and minimizes the risk of rear-end collisions. In addition, increasing government regulations mandating advanced safety technologies in vehicles, particularly in North America, Europe, and parts of Asia-Pacific, are further accelerating ACC adoption and boosts revenue growth of this segment.

In August 2023, ZF introduced an advanced predictive adaptive cruise control system, the ZF Eco Control 4 ACC. It can improve driving range by up to 8%. A key feature of this enhanced ACC is the Model Predictive Control (MPC) optimization algorithm developed by Embotech. The system continuously analyzes real-time data, including map details like road inclines, declines, and curves, along with internal vehicle data related to the powertrain’s most efficient operating conditions.

Vehicle Type Segment Insights and Analysis:

Based on vehicle type, the Advanced Driver Assistance Systems (ADAS) market is segmented into passenger vehicles and commercial vehicles. Commercial vehicles segment is further sub-segmented into Light Commercial Vehicles (LCVs) and Heavy Commercial Vehicles (HCVs).

Passenger vehicles segment contributed the largest revenue share in 2024 due to the increasing consumer demand for safety, convenience, and technologically advanced features. Regulatory authorities and automakers are accelerating the integration of ADAS technologies such as adaptive cruise control, lane keeping assist, and automatic emergency braking into passenger vehicles owing to the increasing awareness of road safety. In addition, the growing emphasis on connected vehicles and semi-autonomous driving capabilities further drives revenue growth of this segment.

The implementation of mandatory safety regulations to reduce road accidents by Governments across the globe is also driving revenue growth of this segment. For example, from April 2026, all newly launched passenger vehicle models in India, designed to carry more than eight occupants, as well as buses and trucks, will be required to feature Advanced Emergency Braking Systems (AEBS), Driver Drowsiness and Attention Warning Systems (DDAWS), and Lane Departure Warning Systems (LDWS). According to a draft notification issued by the Ministry of Road Transport, these safety requirements will also extend to existing vehicle models starting from October 2026.

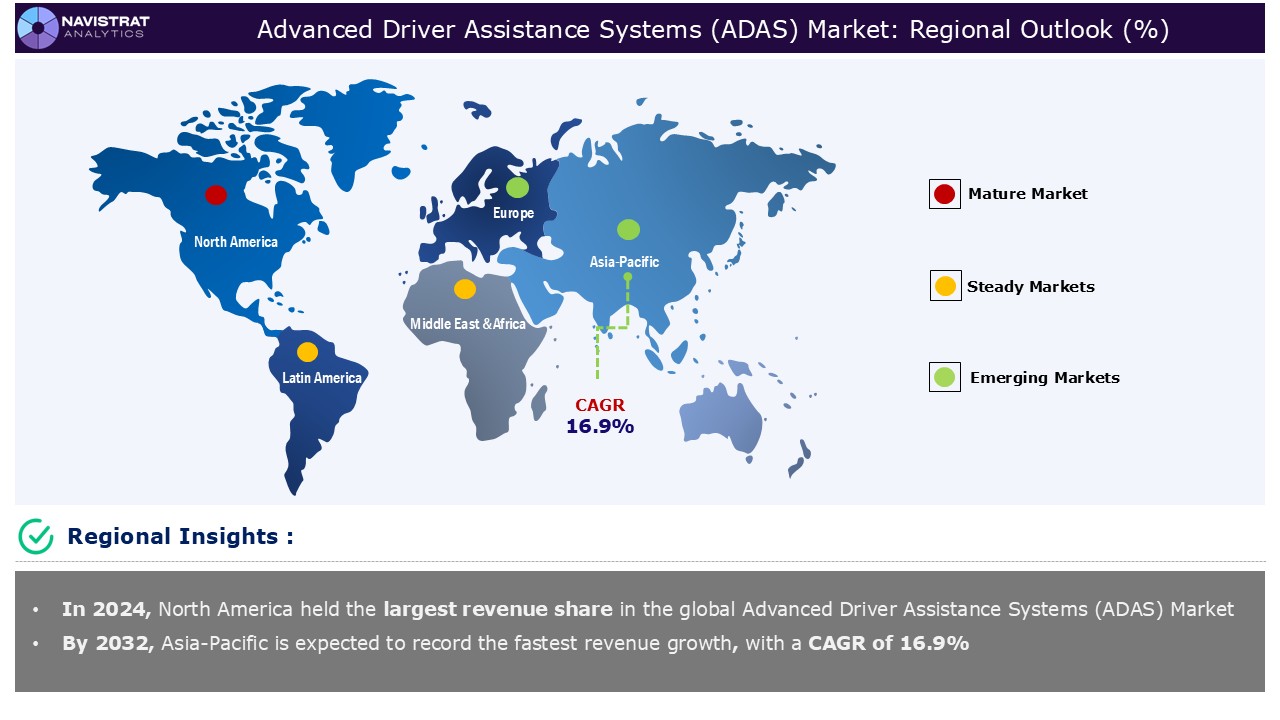

Geographical Outlook:

Advanced Driver Assistance Systems (ADAS) market is strategically segmented by geography to provide a comprehensive understanding of regional market dynamic. Discover demand analysis, emerging trends, and growth opportunities shaping market performance across different region and countries.

North America Advanced Driver Assistance Systems (ADAS) Market:

Market in North America accounted for largest revenue share in 2024 due to the combination of regulatory mandates, high consumer awareness, and rapid technological advancements in the region, especially in U.S. and Canada. Stringent safety regulations enforced by agencies such as the National Highway Traffic Safety Administration (NHTSA) are compelling automakers to integrate ADAS features like automatic emergency braking, lane departure warning, and blind spot detection into new vehicle models. In November 2024, the NHTSA expanded its program to encompass four key advanced driver assistance systems (ADAS) technologies: Pedestrian Automatic Emergency Braking (PAEB), Lane Keeping Assist (LKA), Blind Spot Warning (BSW), and Blind Spot Intervention (BSI). The updated testing protocols are designed to improve vehicle performance in preventing collisions, thereby influencing how vehicles respond to real-world driving conditions.

In addition, increasing investments in autonomous driving are also fueling innovation and deployment of ADAS solutions across the region. The year 2024 witnessed consistent progress in the Autonomous Vehicle (AV) sector in the United States. In July, Alphabet, the parent company of Waymo, announced plans to invest up to USD 5 billion in the AV startup. During the same period, Waymo also introduced the sixth generation of its autonomous driving platform, known as the Waymo Driver. The company currently operates a fleet of approximately 800 self-driving vehicles across California, with additional units deployed in Phoenix, Arizona. The expansion of self-driving fleets in U.S. is creating greater commercial deployment opportunities for ADAS technologies and drives revenue growth of the market is this region.

Asia Pacific Advanced Driver Assistance Systems (ADAS) Market:

Asia Pacific is expected to register a fast revenue growth rate during the forecast period due to the rapid vehicle production, increasing adoption of safety technologies, and supportive government regulations. Countries like China, Japan, South Korea, and India are witnessing a surge in demand for passenger and commercial vehicles equipped with ADAS features. Currently, around 25% of newly registered vehicles in China are equipped with Level 2 driving systems designed for highway use. By 2030, over 80% of vehicles in the Chinese market are expected to feature Level 2+ systems. Additionally, Level 2++ systems capable of handling both highway and urban driving environments are projected to be integrated into 75% of new vehicles by that time. At Auto Shanghai 2025, the Volkswagen Group unveiled its first internally developed Advanced Driver Assistance System (ADAS), aimed at delivering particularly smooth and safe driving experiences.

In addition, the presence of leading automotive component manufacturers and the expansion of smart city and connected vehicle infrastructure are further accelerating ADAS implementation in this region. Looking ahead to 2030, the Chinese government has outlined specific targets for the Intelligent Connected Vehicle (ICV) sector. These include having over 70% of new vehicles feature partial or conditional automation, more than 50% equipped with high-level automation capabilities, and nearly all new vehicles integrated with Cellular Vehicle-to-Everything (C-V2X) technology. These developments are fueling substantial revenue growth across the ADAS ecosystem in China.

Europe Advanced Driver Assistance Systems (ADAS) Market:

Market in Europe accounted for a significant revenue share in 2024 due to stringent safety regulations, rising consumer demand for vehicle safety technologies, and the leadership in automotive innovation in the region. The European Union has mandated the inclusion of several ADAS features, such as intelligent speed assistance, lane keeping systems, and automatic emergency braking, in all new vehicles starting from July 2024 under the General Safety Regulation (GSR). These regulatory requirements are compelling automakers to accelerate the integration of advanced safety technologies across passenger and commercial vehicle fleets.

In addition, the presence of leading OEMs and Tier-1 suppliers in Germany, France, and UK also fosters continuous innovation and large-scale deployment. In January 2025, German automotive technology company Continental debuted its Xelve portfolio—a scalable, cost-efficient solution for ADAS and automated driving. The system featured Bird’s-Eye View and deep fusion technology. It utilized raw data from satellite cameras along with Continental’s advanced sixth-generation radar sensors to generate a comprehensive 360° spatial model of the vehicle’s surroundings. It can significantly increase the safety and performance of automated driving functionalities.

Competition Analysis:

The Advanced Driver Assistance Systems (ADAS) market is characterized by a fragmented structure, with numerous players competing across various segments and regions. List of major players included in the Advanced Driver Assistance Systems (ADAS) market report are:

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Aptiv PLC

- Magna International Inc.

- Valeo SA

- Altera Corporation

- Autoliv

- Garmin Ltd.

- Texas Instruments

- ZF Friedrichshafen

- BorgWarner

- Mobileye

- WABCO Holdings, Inc.

Strategic Developments in Advanced Driver Assistance Systems (ADAS) Market:

- On 21 April 2025, Hexagon’s Manufacturing Intelligence division launched a cloud-native platform designed to test, train, and validate Advanced Driver Assistance Systems (ADAS) and autonomous vehicle technologies. The solution—Virtual Test Drive X (VTDx) allows the automotive industry to automatically assess software performance across thousands of real-world driving scenarios. This capability significantly shortens development cycles and speeds up the deployment of safe and reliable mobility innovations.

- On 18 February 2025, Elitek Vehicle Services, a subsidiary of LKQ, announced the launch of its cutting-edge ADAS MAP (Advanced Driver Assistance Systems Mapping) solution. Developed in collaboration with OPUS IVS, a global expert in intelligent vehicle support, the new software tool is designed to equip repair shops with the accuracy and efficiency required to effectively diagnose, calibrate, and service ADAS components in modern vehicles.

- 16 December 2024, Onsemi and leading tier-one automotive supplier Denso Corporation announced an expansion of their long-standing partnership to advance the procurement of technologies for Autonomous Driving (AD) and Advanced Driver Assistance Systems (ADAS). For more than a decade, Onsemi has been providing DENSO with cutting-edge intelligent automotive sensors aimed at enhancing the performance of ADAS and AD solutions. These semiconductors play a crucial role in boosting vehicle intelligence and connectivity, contributing significantly to efforts to reduce traffic-related fatalities.

Key Advantages for Stakeholders:

Navistrat Analytics’ industry report provides an in-depth quantitative analysis of various market segments, historical and current trends, market forecasts, and dynamics within the global market. The historical years covered in this report are 2022 to 2023, with 2024 serving as the base year for market size calculations. The forecast period extends from 2025 to 2032.

The report includes an executive summary and a comprehensive overview of market drivers, restraints, opportunities, and challenges (DROC), along with insights into regulatory standards. It features detailed analyses such as PORTER’s Five Forces, SWOT, and PESTLE, as well as assessments of technological trends and the competitive landscape.

PORTER’s Five Forces analysis helps stakeholders evaluate the impact of new entrants, competitive rivalry, supplier power, buyer power, and substitution threats, enabling them to assess the level of competition and the attractiveness of the global market. The competitive landscape provides stakeholders with a clear understanding of the current market positions of key players, offering valuable insights into their competitive environment.

Scope And Key Highlights of The Advanced Driver Assistance Systems (ADAS) Market Report:

| Report Features | Details |

| Market Size in 2024 | USD 36.72 Billion |

| Market Growth Rate in CAGR (2025–2032) | 13.8% |

| Market Revenue Forecast to 2032 | USD 101.97 Billion |

| Base year | 2024 |

| Historical year | 2022–2023 |

| Forecast period | 2025–2032 |

| Report Pages | 450 |

| Segments Covered |

|

| Regional scope |

|

| Country Scope |

|

| Key Market Players |

|

| Delivery Format | Reports are delivered in PDF format via email. |

| Customization scope | Request Customization |

The Advanced Driver Assistance Systems (ADAS) market report offers a detailed analysis of market size, including historical revenue (in USD Billion) data for 2022-2023 and revenue forecasts for 2025-2032 across the following segments:

- Component (Revenue, USD Billion; 2022-2032)

- Hardware

- Sensors

- Radar

- Lidar

- Ultrasonic Sensors

- Infrared Sensors

- Electronic Control Units (ECUs)

- Actuators

- Display Panels

- Others

- Sensors

- Software

- Embedded Software

- AI/ML Algorithms

- Mapping & Navigation Software

- Others

- Hardware

- Function Outlook (Revenue, USD Billion; 2022-2032)

- Adaptive Cruise Control (ACC)

- Automatic Emergency Braking (AEB)

- Lane Departure Warning (LDW)

- Lane Keeping Assist System (LKAS)

- Blind Spot Detection (BSD)

- Traffic Sign Recognition (TSR)

- Driver Monitoring Systems (DMS)

- Forward Collision Warning (FCW)

- Night Vision Systems (NVS)

- Park Assist / Automated Parking System

- Others

- Vehicle Type Outlook (Revenue, USD Billion; 2022-2032)

- Passenger Vehicles

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Level of Automation (Revenue, USD Billion; 2022-2032)

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Sales Channel (Revenue, USD Billion; 2022-2032)

- Original Equipment Manufacturer (OEMs)

- Aftermarket

- Regional Outlook (Revenue, USD Billion; 2022-2032)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Oceania

- ASEAN Countries

- Rest of APAC

- Latin America

- Brazil

- Rest of LATAM

- Middle East & Africa

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of MEA

- North America

Frequently Asked Questions (FAQ) about the Advanced Driver Assistance Systems (ADAS) Market Report

The Advanced Driver Assistance Systems (ADAS) market size was USD 36.72 Billion in 2024.

The Advanced Driver Assistance Systems (ADAS) market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 13.8% during the forecast period.

Increasing enforcement of road safety policies across the globe, rising focus on accident prevention, growing expansion of electric and autonomous vehicles, and rising consumer demand for tech-enabled driving experiences are the key drivers of the Advanced Driver Assistance Systems (ADAS) market revenue growth.

Data privacy and cybersecurity risks, high cost of ADAS components and integration and limited awareness of ADAS features among consumers are key factors restraining revenue growth of the market.

Asia Pacific is expected to account for the fastest revenue growth of 16.9%.

Hardware segment is the leading segment of Advanced Driver Assistance Systems (ADAS) market in terms of application.

- Market Definition

- Research Objective

- Research Methodology

- Research Design

- Data Collection Methods

- Primary

- Secondary

- Market Size Estimation

- Top-down method

- Bottom-up method

- Forecasting Methodology

- Tools and Models Used

- Market Overview and Trends

- Market Size and Forecast

- Industry Analysis

- Market Drivers, Restraints, Opportunitiesand Challenges (DROC) Analysis

- Market Drivers

- Increasing enforcement of road safety policies across the globe

- Rising focus on accident prevention

- Growing expansion of electric and autonomous vehicles

- Rising consumer demand for tech-enabled driving experiences

- Market Restraints

- Data privacy and cybersecurity risks

- High cost of ADAS components and integration

- Limited awareness of ADAS features among consumers

- Market Opportunities

- Rapid advancements in sensor & AI technologies

- Rising collaboration between OEM and Tier-1 Suppliers

- Increasing adoption of ADAS in emerging markets

- Market Challenges

- Regulatory and liability challenges

- Complexities in maintenance and repair

- Regulatory Landscape

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

- Strategic Insights

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Price Trend Analysis

- Value Chain Analysis

- Technological Trends

- Recent Developments

- Funding

- Merger and Acquisition

- Expansion

- Partnership and Collaboration

- Product/Service Launch

- Component Market Revenue Estimates and Forecasts, 2022-2032

- Hardware

- Sensors

- Radar

- Lidar

- Ultrasonic Sensors

- Infrared Sensors

- Image Sensors

- Electronic Control Units (ECUs)

- Actuators

- Display Panels

- Others

- Sensors

- Software

- Embedded Software

- AI/ML Algorithms

- Mapping & Navigation Software

- Others

- Hardware

- Function Market Revenue Estimates and Forecasts, 2022-2032

- Adaptive Cruise Control (ACC)

- Automatic Emergency Braking (AEB)

- Lane Departure Warning (LDW)

- Lane Keeping Assist System (LKAS)

- Blind Spot Detection (BSD)

- Traffic Sign Recognition (TSR)

- Driver Monitoring Systems (DMS)

- Forward Collision Warning (FCW)

- Night Vision Systems (NVS)

- Park Assist / Automated Parking System

- Others

- Vehicle Type Market Revenue Estimates and Forecasts, 2022-2032

- Passenger Vehicles

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Level of Automation Market Revenue Estimates and Forecasts, 2022-2032

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Sales Channel Market Revenue Estimates and Forecasts, 2022-2032

- Original Equipment Manufacturers (OEMs)

- Aftermarket

- Advanced Driver Assistance Systems (ADAS) Market Revenue Estimates and Forecasts by Region, 2022-2032, USD Billion

- North America

- North America Advanced Driver Assistance Systems (ADAS) Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Hardware

- Sensors

- Radar

- Lidar

- Ultrasonic Sensors

- Infrared Sensors

- Image Sensors

- Electronic Control Units (ECUs)

- Actuators

- Display Panels

- Others

- Sensors

- Software

- Embedded Software

- AI/ML Algorithms

- Mapping & Navigation Software

- Others

- Hardware

- North America Advanced Driver Assistance Systems (ADAS) Market By Function, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Adaptive Cruise Control (ACC)

- Automatic Emergency Braking (AEB)

- Lane Departure Warning (LDW)

- Lane Keeping Assist System (LKAS)

- Blind Spot Detection (BSD)

- Traffic Sign Recognition (TSR)

- Driver Monitoring Systems (DMS)

- Forward Collision Warning (FCW)

- Night Vision Systems (NVS)

- Park Assist / Automated Parking System

- Others

- North America Advanced Driver Assistance Systems (ADAS) Market By Vehicle Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Passenger Vehicles

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- North America Advanced Driver Assistance Systems (ADAS) Market By Level of Automation, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

- North America Advanced Driver Assistance Systems (ADAS) Market By Sales Channel, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Original Equipment Manufacturers (OEMs)

- Aftermarket

- North America Advanced Driver Assistance Systems (ADAS) Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion

- United States

- Canada

- Mexico

- North America Advanced Driver Assistance Systems (ADAS) Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Europe

- Europe Advanced Driver Assistance Systems (ADAS) Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Hardware

- Sensors

- Radar

- Lidar

- Ultrasonic Sensors

- Infrared Sensors

- Image Sensors

- Electronic Control Units (ECUs)

- Actuators

- Display Panels

- Others

- Sensors

- Software

- Embedded Software

- AI/ML Algorithms

- Mapping & Navigation Software

- Others

- Hardware

- Europe Advanced Driver Assistance Systems (ADAS) Market By Function, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Adaptive Cruise Control (ACC)

- Automatic Emergency Braking (AEB)

- Lane Departure Warning (LDW)

- Lane Keeping Assist System (LKAS)

- Blind Spot Detection (BSD)

- Traffic Sign Recognition (TSR)

- Driver Monitoring Systems (DMS)

- Forward Collision Warning (FCW)

- Night Vision Systems (NVS)

- Park Assist / Automated Parking System

- Others

- Europe Advanced Driver Assistance Systems (ADAS) Market By Vehicle Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Passenger Vehicles

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Europe Advanced Driver Assistance Systems (ADAS) Market By Level of Automation, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Europe Advanced Driver Assistance Systems (ADAS) Market By Sales Channel, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Original Equipment Manufacturers (OEMs)

- Aftermarket

- Europe Advanced Driver Assistance Systems (ADAS) Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion

- Germany

- United Kingdom

- France

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Europe Advanced Driver Assistance Systems (ADAS) Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Asia-Pacific

- Asia-Pacific Advanced Driver Assistance Systems (ADAS) Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Hardware

- Sensors

- Radar

- Lidar

- Ultrasonic Sensors

- Infrared Sensors

- Image Sensors

- Electronic Control Units (ECUs)

- Actuators

- Display Panels

- Others

- Sensors

- Software

- Embedded Software

- AI/ML Algorithms

- Mapping & Navigation Software

- Others

- Hardware

- Asia-Pacific Advanced Driver Assistance Systems (ADAS) Market By Function, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Adaptive Cruise Control (ACC)

- Automatic Emergency Braking (AEB)

- Lane Departure Warning (LDW)

- Lane Keeping Assist System (LKAS)

- Blind Spot Detection (BSD)

- Traffic Sign Recognition (TSR)

- Driver Monitoring Systems (DMS)

- Forward Collision Warning (FCW)

- Night Vision Systems (NVS)

- Park Assist / Automated Parking System

- Others

- Asia-Pacific Advanced Driver Assistance Systems (ADAS) Market By Vehicle Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Passenger Vehicles

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Asia-Pacific Advanced Driver Assistance Systems (ADAS) Market By Level of Automation, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Asia-Pacific Advanced Driver Assistance Systems (ADAS) Market By Sales Channel, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Original Equipment Manufacturers (OEMs)

- Aftermarket

- Asia-Pacific Advanced Driver Assistance Systems (ADAS) Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion

- China

- India

- Japan

- South Korea

- Oceania

- ASEAN Countries

- Rest of Asia-Pacific

- Asia-Pacific Advanced Driver Assistance Systems (ADAS) Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Latin America

- Latin America Advanced Driver Assistance Systems (ADAS) Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Hardware

- Sensors

- Radar

- Lidar

- Ultrasonic Sensors

- Infrared Sensors

- Image Sensors

- Electronic Control Units (ECUs)

- Actuators

- Display Panels

- Others

- Sensors

- Software

- Embedded Software

- AI/ML Algorithms

- Mapping & Navigation Software

- Others

- Hardware

- Latin America Advanced Driver Assistance Systems (ADAS) Market By Function, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Adaptive Cruise Control (ACC)

- Automatic Emergency Braking (AEB)

- Lane Departure Warning (LDW)

- Lane Keeping Assist System (LKAS)

- Blind Spot Detection (BSD)

- Traffic Sign Recognition (TSR)

- Driver Monitoring Systems (DMS)

- Forward Collision Warning (FCW)

- Night Vision Systems (NVS)

- Park Assist / Automated Parking System

- Others

- Latin America Advanced Driver Assistance Systems (ADAS) Market By Vehicle Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Passenger Vehicles

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Latin America Advanced Driver Assistance Systems (ADAS) Market By Level of Automation, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Latin America Advanced Driver Assistance Systems (ADAS) Market By Sales Channel, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Original Equipment Manufacturers (OEMs)

- Aftermarket

- Latin America Advanced Driver Assistance Systems (ADAS) Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion

- Brazil

- Rest of Latin America

- Latin America Advanced Driver Assistance Systems (ADAS) Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Middle East & Africa

- Middle East & Africa Advanced Driver Assistance Systems (ADAS) Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Hardware

- Sensors

- Radar

- Lidar

- Ultrasonic Sensors

- Infrared Sensors

- Image Sensors

- Electronic Control Units (ECUs)

- Actuators

- Display Panels

- Others

- Sensors

- Software

- Embedded Software

- AI/ML Algorithms

- Mapping & Navigation Software

- Others

- Hardware

- Middle East & Africa Advanced Driver Assistance Systems (ADAS) Market By Function, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Adaptive Cruise Control (ACC)

- Automatic Emergency Braking (AEB)

- Lane Departure Warning (LDW)

- Lane Keeping Assist System (LKAS)

- Blind Spot Detection (BSD)

- Traffic Sign Recognition (TSR)

- Driver Monitoring Systems (DMS)

- Forward Collision Warning (FCW)

- Night Vision Systems (NVS)

- Park Assist / Automated Parking System

- Others

- Middle East & Africa Advanced Driver Assistance Systems (ADAS) Market By Vehicle Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Passenger Vehicles

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Middle East & Africa Advanced Driver Assistance Systems (ADAS) Market By Level of Automation, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Middle East & Africa Advanced Driver Assistance Systems (ADAS) Market By Sales Channel, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Original Equipment Manufacturers (OEMs)

- Aftermarket

- Middle East & Africa Advanced Driver Assistance Systems (ADAS) Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of Middle East & Africa

- Middle East & Africa Advanced Driver Assistance Systems (ADAS) Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Market Share Analysis

- Revenue Market Share by Key Players (2023-2024)

- Analysis of Top Players by Market Presence

- Competitive Matrix

- Competitive Strategies

- Mergers and Acquisitions

- Partnerships and Collaboration

- Investment and Funding

- Agreement

- Expansion

- New Product/Services Launches

- Technological Innovations

- Robert Bosch GmbH

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Continental AG

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Denso Corporation

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Aptiv PLC

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Magna International Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Valeo SA

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Altera Corporation

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Autoliv

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Garmin Ltd.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Texas Instruments

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- ZF Friedrichshafen

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- BorgWarner

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Mobileye

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- WABCO Holdings, Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis