Global Aviation Emissions Control Market Overview and Key Insights:

The global aviation emissions control market size reached USD 1,165.3 million in 2024 and is expected to register a revenue CAGR of 13.6% during the forecast period. Stringent environmental regulations on aviation emissions, rising concerns about climate change, increasing adoption of sustainable aviation practices, and growing government incentives and funding for using clean energy solutions in aviation are expected to drive the revenue growth of the market.

Market Drivers:

Stringent environmental regulations on aviation emissions are the major factor driving revenue growth of the aviation emissions control market. Governments and international bodies, such as the International Civil Aviation Organization (ICAO), have introduced policies like the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) to curb the carbon footprint and reducing carbon-dioxide emissions of the aviation industry. According to the International Energy Agency (IEA), aviation contributed 2% of global energy-related CO2 emissions in 2022. It is experiencing faster growth than rail, road, or shipping in recent decades. With the post-COVID boom in international air travel, aviation emissions approached 800 million tons of CO2, about 80% of pre-pandemic levels.

Several technological measures, including the adoption of low-emission fuels such as biofuel-powered airplanes, advancements in airframe and engine technologies, operational efficiency improvements, and demand management strategies, are essential to curb emissions growth and achieve the Net Zero Emissions (NZE) in 2050. In 2022, the 184 member states of the International Civil Aviation Organization (ICAO) endorsed a Long-Term Global Aspirational Goal (LTAG). This program aims to acheve net-zero carbon emissions in international aviation by 2050, which is expected to boost revenue growth of the market.

Additionally, the general aviation sector is witnessing increasing activity, with more take-offs and landings at runways worldwide. It is necessitating sustainable practices. Factors like high-altitude operations and the push for greener airways contribute to the industry’s shift towards eco-friendly alternatives, which is further boosting market revenue growth.

Market Opportunity:

Increasing expansion of global passenger and cargo air traffic is creating significant opportunities for the aviation emissions control market. The demand for air travel has risen in recent years owing to economic growth, globalization, and e-commerce expansion. According to The Airports Council International (ACI), there is a 10% growth in global passenger traffic, reaching 9.5 billion passengers by 2024. In 2023, global passenger traffic was 8.7 billion, recovering to 95% of pre-pandemic levels. By the end of 2024, international passenger traffic is expected to hit 4.1 billion, representing 43% of the total, while domestic passenger traffic is expected to reach 5.4 billion, accounting for the remaining 57%.

As air travel demand rises the aviation industry is under pressure to address its environmental impact. This surge in air traffic results in higher fuel consumption and emissions. It increases the need for innovative emissions control technologies and sustainable practices. Airlines and aircraft manufacturers are investing heavily in solutions such as advanced propulsion systems, Sustainable Aviation Fuels (SAFs), and aerodynamic design improvements to meet regulatory standards and reduce their carbon footprint. This growing emphasis on sustainability in aviation is expected to increase the adoption of aviation emissions control solutions and drives revenue growth of the market.

Recent Trends:

One recent trend in the aviation emissions control market is the rising exploration of hydrogen-powered aircraft. The need for efficient emissions control solutions is rising due to the growing air-transpiration demand and the expansion of airspace for both manned and unmanned aircraft. Hydrogen is recognized as a sustainable alternative fuel due to its potential to eliminate carbon emissions during combustion. Key players in the aviation industry, such as Airbus and ZeroAvia, are investing heavily in the research and development of hydrogen-powered aircraft.

In June 2023, Airbus revealed the successful completion of a test campaign for its hydrogen fuel cell system. It reached a full power output of 1.2 megawatts. Their goal is to introduce the world’s first hydrogen-powered commercial aircraft by 2035. In July 2024, ZeroAvia and KLM Royal Dutch Airlines announced that they would collaborate on a demonstration flight using ZeroAvia’s ZA2000 hydrogen-electric engines. These are designed for large regional turboprops with zero emissions.

Restraints & Challenges:

Slow adoption of alternative propulsion systems is a significant restraint on the revenue growth of the aviation emissions control market. The aviation industry faces challenges in transitioning from traditional jet engines to alternative technologies. High research and development costs, technical complexities, limited infrastructure for fueling and maintenance, and the long certification process for new propulsion systems hinder the widespread adoption of these innovations. These barriers slow the pace and limits the overall revenue growth of the aviation emissions control market.

Component Segment Insights and Analysis:

Based on the component, the aviation emissions control market is segmented into hardware, software and services. Hardware segment is further sub-segmented into sensors, actuators, filters and others. Software segment is further sub-segmented into emission monitoring software, predictive maintenance tools and others. Services segment is further sub-segmented into installation services and maintenance & repair services.

Hardware segment contributed largest share in 2024 due to the increasing demand for advanced technologies owing to reducing aircraft emissions. Key hardware components are essential for compliance with stringent environmental regulations. Airlines and aircraft manufacturers are heavily investing in retrofitting older fleets. They are integrating hardware solutions into new aircraft to enhance fuel efficiency and minimize carbon footprints.

In October 2024, aerospace company Natilus unveiled plans to develop a commercial aircraft designed to reduce emissions by 50% and consume 30% less fuel compared to other airliners in the market. The company announced that it will pioneer the use of a blended wing body design in commercial aviation. The horizon model is set to compete with well-established aircraft like the Boeing 737 Max and Airbus A320, which rely on the traditional tube-and-wing configuration.

Software segment is expected to register a fast revenue growth rate during the forecast period due to the increasing demand for advanced solutions to monitor, manage, and optimize aviation emissions. Airlines and airport operators are increasingly adopting software-driven tools to ensure compliance with stringent environmental regulations and achieve sustainability targets. Emissions management software provided real-time tracking and analysis of carbon footprints. It is facilitating precise reporting and adherence to international standards such as CORSIA and ICAO guidelines.

On September 2024 for instance, airline company Air Premia announced the implementation of GE Aerospace’s integrated software solution aimed at reducing carbon emissions and enhancing operational efficiency and safety. The solution features three software programs: Fuel Insight, Safety Insight, and FlightPulse. These tools collectively improve fuel efficiency by 1.4% annually and potentially cutting carbon emissions by 5,916 tons based on Air Premia’s current operations.

Aircraft Type Segment Insights and Analysis:

Based on aircraft type, the aviation emissions control market is segmented into narrow-body aircraft, wide-body aircraft, regional aircraft, turboprop aircraft, business jets, helicopter and others. Narrow-body aircraft is further sub-segmented into narrowbody long-haul flights, narrowbody medium-haul flights, and narrowbody short-haul flights. Wide-body aircraft is further sub-segmented into wide-body long-haul flights, wide-body medium-haul flights, and wide-body short-haul flights. Regional aircraft is further sub-segmented into regional long-haul flights, regional medium-haul flights, and regional short-haul flights. Turboprop aircraft is further sub segmented in turboprop long-haul flights, turboprop medium-haul flights, and turboprop short-haul flights.

Wide-body aircraft segment contributed largest share in 2024 due to its crucial role in long-haul international travel, which demands greater fuel efficiency and compliance with stringent environmental regulations. These aircraft are equipped with advanced emissions control technologies, such as next-generation engines, aerodynamic enhancements, and sustainable fuel systems, to meet global carbon reduction targets.

On March 2023 Vistara, a joint venture between the Tata Group and Singapore Airlines, announced that it has become the first Indian airline to operate a wide-body aircraft using Sustainable Aviation Fuel (SAF) on a long-haul route. By utilizing a fuel blend comprising 30% SAF and 70% conventional jet fuel, Vistara reported a reduction of approximately 150,000 pounds of CO2 emissions over the fuel’s lifecycle.

Turboprop aircraft segment is expected to register a fast revenue growth rate during the forecast period due to its fuel efficiency and suitability for short-haul routes. These aircraft consume less fuel compared to jet-powered counterparts. It aligns with the growing emphasis on reducing aviation emissions. Additionally, developers are integrating advancements in propulsion technologies, including hybrid-electric systems into turboprops to enhance their environmental performance, which is driving the adoption of turboprop aircraft.

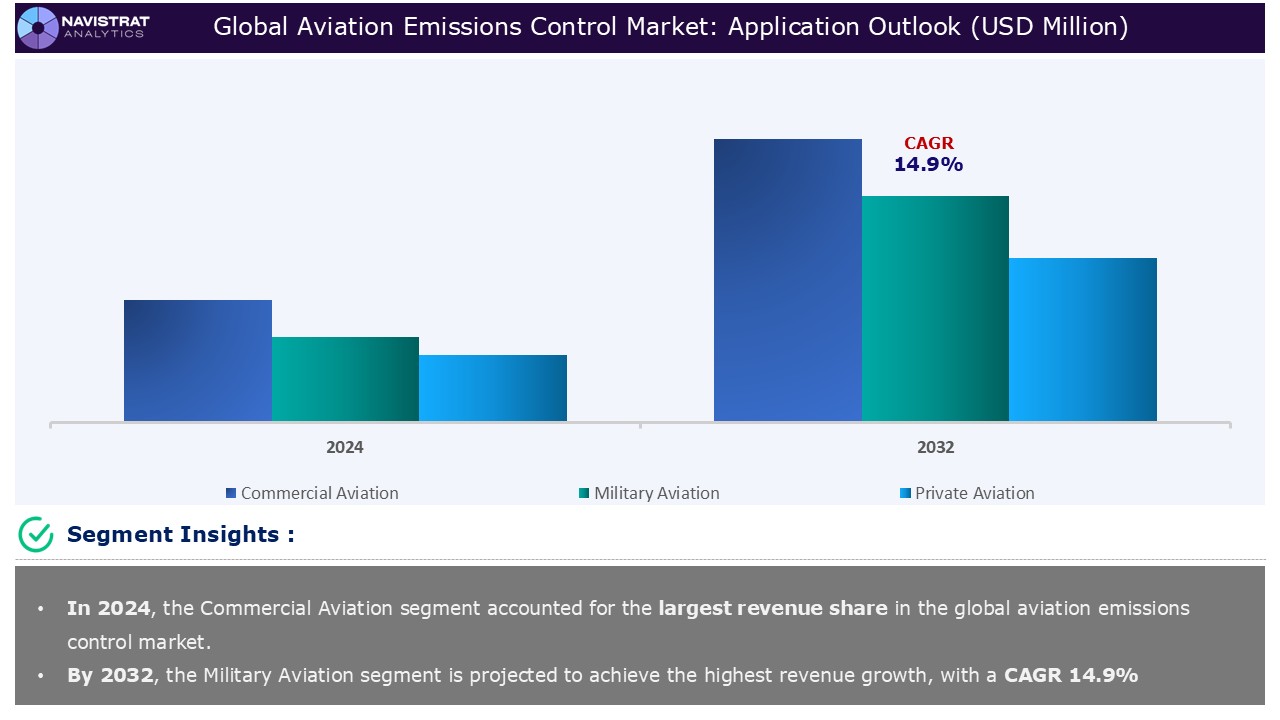

Application Segment Insights and Analysis:

Based on the application, the aviation emissions control market is segmented into commercial aviation, military aviation and private aviation.

Commercial aviation segment contributed largest share in 2024. The commercial aviation industry is expanding rapidly owing to the rising global passenger traffic, increased connectivity, and the growth of low-cost carriers. This expansion has led to a surge in aircraft deliveries, fleet modernization, and the introduction of new routes. However, the expansion also amplifies the environmental impact of aviation, with increased greenhouse gas emissions and noise pollution becoming pressing concerns. As a result, the aviation emissions control market is gaining traction. The airlines and manufacturers are investing in sustainable technologies such as fuel-efficient engines, alternative fuels, and emissions monitoring systems which is boosting the revenue growth of this segment.

Military aviation segment is expected to have the fastest CAGR throughout the forecasted period. Military aviation contributes significantly to greenhouse gas emissions due to the high fuel consumption of its fleet. This is prompting defense organizations to align with global sustainability goals and reduce their carbon footprint. Manufacturers are integrating advanced emissions control technologies, such as fuel-efficient engines, Sustainable Aviation Fuels (SAF), and emissions monitoring systems to meet stringent environmental regulations and enhance operational efficiency.

For example, The UK government has set a legal obligation for the country to achieve net-zero emissions by 2050. In line with this, the Ministry of Defence (MOD) has outlined its approach in the Climate Change and Sustainability Strategic Approach, detailing how the defense sector will contribute to this goal. Additionally, in 2022, the Department for Transport (DfT) released the Jet Zero Strategy, aiming to achieve net-zero emissions for UK aviation by 2050.

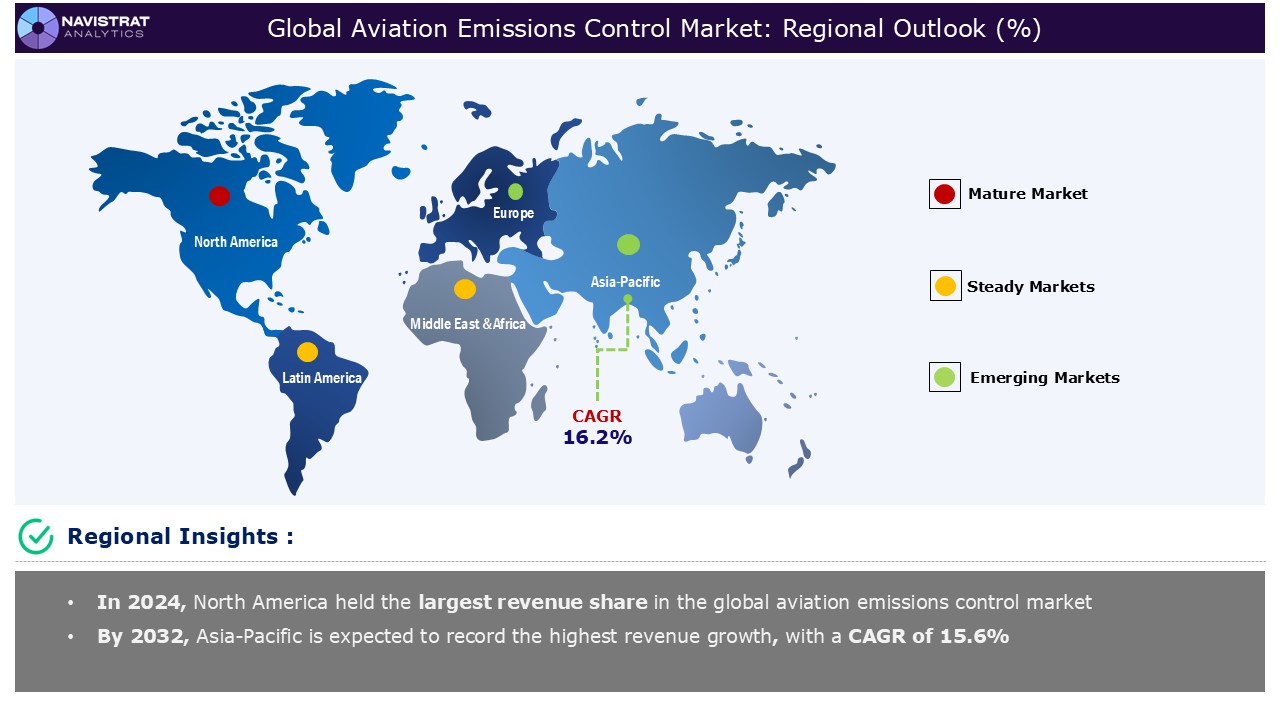

Geographical Outlook:

Market in North America accounted for largest revenue share in 2024 due to the stringent environmental regulations, increasing demand for sustainable aviation practices, and significant investments in green technologies by both government and private sectors in the region, especially in U.S. and Canada. The United States and Canada have set ambitious goals to reduce carbon emissions. U.S. has targeted net-zero emissions by 2050 and Canada aims to achieve net-zero emissions for its aviation sector by 2050. This regulatory push is motivating airlines and manufacturers to adopt more efficient and low-emission technologies.

The increasing supporting initiatives by the government also boost the revenue growth of the market in this region. In 2022, for instance, the United States made a significant commitment to advancing Sustainable Aviation Fuel (SAF) production through the Inflation Reduction Act. The U.S. government introduced substantial tax credits and a competitive grant program. The government has allocated USD 3.3 billion to scale up SAF production in the country. This initiative aims to help the U.S. reach a target of producing 3 billion gallons of SAF by 2030. This push is part of a broader effort to reduce aviation emissions and accelerate the transition to cleaner, more sustainable fuel alternatives in the aviation industry. U.S. is positioning itself as a leader in the global push for greener aviation practices with these investments.

Asia Pacific is expected to register a fast revenue growth rate during the forecast period due to rapid expansion of the aviation industry, increasing focus on environmental sustainability, and the implementation of stricter emissions regulations in countries, especially in China, India, and Japan. The demand for emissions control solutions is rising as these countries significantly expand air traffic and airline operations. In recent years, Governments in Asia Pacific have set ambitious carbon reduction targets and adopted international standards.

In 2022, the Civil Aviation Administration of China (CAAC) unveiled the 14th Five-Year Plan for Green Development of Civil Aviation. They are outlining a vision for sustainable development by 2035. This includes the creation of a robust green, low-carbon circular development system, achieving carbon-neutral growth in air transport, and positioning green civil aviation as a key focus in international exchanges. The plan aims to establish China as a leading force in the global push for sustainable development within the civil aviation sector. These factors, coupled with growing public and governmental pressure to address climate change are propelling the revenue growth of the market in the region.

Market in Europe is expected to register a modest revenue growth rate during the forecast period due to the strong commitment to environmental sustainability and stringent regulatory frameworks in the region. In 2023, the European Parliament and Council of the European Union reached a political consensus on ReFuelEU Aviation regulations. They are outlining a timeline for minimum Sustainable Aviation Fuel (SAF) blending requirements. It includes specific targets for synthetic fuels, extending through 2050. Meanwhile, in 2022, the United Kingdom allocated GBP 165 million (USD 205 million) for SAF projects, under the Jet Zero commitment. This multidisciplinary program aims to have at least five commercial facilities for SAF production under construction by 2025, underscoring the region’s commitment to sustainable aviation and emissions reduction.

Competition Analysis:

The aviation emissions control market is characterized by a fragmented structure, with numerous players competing across various segments and regions. List of major players included in the Aviation Emissions Control market report are:

- Airbus SE

- Embraer S.A.

- Rolls-Royce Holdings plc

- GE Aerospace (General Electric)

- Pratt & Whitney

- Safran Grpup

- Neste Corporation

- Gevo, Inc.

- Aemetis, Inc.

- Thales Group

- Indra Sistemas, S.A

- Collins Aerospace

- Textron Aviation

- MTU Aero Engines

Strategic Developments in Aviation emissions control Market:

- On 23 July 2024, Embraer has unveiled advancements in its sustainable aircraft initiative, Energia, showcasing its commitment to eco-friendly aviation. The company has broadened its research scope to include 50-seater aircraft, moving beyond its initial focus on 30-seater models. Additionally, Embraer is now exploring Hydrogen Gas Turbine/Dual Fuel (GT/DF) technologies, complementing its ongoing investigations into hybrid electric and fuel cell systems.

- On 19 July 2024, GE Aerospace signed the Aviation Net Zero Charter of UK Ministry of Defence (MOD). It outlines the importance of climate change and sustainability within the defense aviation sector and its role in supporting the UK’s Net Zero ambition. The signing marks a significant step forward in encouraging collaboration and sharing best practices among partners, enabling defense aviation to contribute positively to the Government’s Net Zero objectives and support the Royal Air Force’s aspiration to achieve Net Zero by 2040.

Key Advantages for Stakeholders:

Navistrat Analytics’ industry report provides an in-depth quantitative analysis of various market segments, historical and current trends, market forecasts, and dynamics within the global market. The historical years covered in this report are 2022 to 2023, with 2024 serving as the base year for market size calculations. The forecast period extends from 2025 to 2032.

The report includes an executive summary and a comprehensive overview of market Drivers, Restraints, Opportunities, and Challenges (DROC), along with insights into regulatory standards. It features detailed analyses such as PORTER’s Five Forces, SWOT, and PESTLE, as well as assessments of technological trends and the competitive landscape.

PORTER’s Five Forces analysis helps stakeholders evaluate the impact of new entrants, competitive rivalry, supplier power, buyer power, and substitution threats, enabling them to assess the level of competition and the attractiveness of the global market. The competitive landscape provides stakeholders with a clear understanding of the current market positions of key players, offering valuable insights into their competitive environment.

Scope And Key Highlights of The Aviation emissions control Market Report:

| Report Features | Details |

| Market Size in 2024 | USD 1,165.3 Million |

| Market Growth Rate in CAGR (2025–2032) | 13.6% |

| Market Revenue Forecast to 2032 | USD 3,214.0 Million |

| Base year | 2024 |

| Historical year | 2022–2023 |

| Forecast period | 2025–2032 |

| Report Pages | 450 |

| Segments Covered |

|

| Regional scope |

|

| Country Scope |

|

| Key Market Players |

|

| Delivery Format | Reports are delivered in PDF format via email. |

| Customization Scope | Request for Customization |

The aviation emissions control market report offers a detailed analysis of market size, including historical revenue (in USD Million) data for 2022-2023 and revenue forecasts for 2025-2032 across the following segments:

- Component Outlook (Revenue, USD Million; 2022-2032)

- Hardware

- Sensors

- Actuators

- Filters

- Others

- Software

- Emission Monitoring Software

- Predictive Maintenance Tools

- Others

- Services

- Installation Services

- Maintenance & Repair Services

- Hardware

-

- Aircraft Type Outlook (Revenue, USD Million; 2022-2032)

- Narrow-body Aircraft

- Narrowbody Long-Haul Flights

- Narrowbody Medium-Haul Flights

- Narrowbody Short-Haul Flights

- Wide-body Aircraft

- Widebody Long-Haul Flights

- Widebody Medium-Haul Flights

- Widebody Short-Haul Flights

- Regional Aircraft

- Regional Jet Long-Haul Flights

- Regional Jet Medium-Haul Flights

- Regional Jet Short-Haul Flights

- Turboprop Aircraft

- Turboprop Long-Haul Flights

- Turboprop Medium-Haul Flights

- Turboprop Short-Haul Flights

- Business Jets

- Helicopters

- Others

- Narrow-body Aircraft

- Aircraft Type Outlook (Revenue, USD Million; 2022-2032)

-

- Scenario (Revenue, USD Million; 2022-2032)

- No Emissions Control

- Optimistic Scenario

- Ideal Scenario

- Most Likely Scenario

- Scenario (Revenue, USD Million; 2022-2032)

-

- Fuel Type Outlook (Revenue, USD Million; 2022-2032)

- Bio-Jet Fuel

- Hydrogen

- Ammonia

- Liquefied Methane

- Others

- Fuel Type Outlook (Revenue, USD Million; 2022-2032)

-

- Application Outlook (Revenue, USD Million; 2022-2032)

- Commercial Aviation

- Military Aviation

- Private Aviation

- Application Outlook (Revenue, USD Million; 2022-2032)

-

- Regional Outlook (Revenue, USD Million; 2022-2032)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Oceania

- ASEAN Countries

- Rest of APAC

- Latin America

- Brazil

- Rest of LATAM

- Middle East & Africa

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of MEA

- North America

- Regional Outlook (Revenue, USD Million; 2022-2032)

Frequently Asked Questions (FAQ) about the Aviation Emissions Control Market report

The aviation emissions control market size was USD 1,165.3 Million in 2024.

The aviation emissions control market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 13.6% during the forecast period.

Stringent environmental regulations on aviation emissions, rising concerns about climate change, increasing adoption of sustainable aviation practices, and growing government incentives and funding for using clean energy solutions in aviation are the key drivers of the aviation emissions control market revenue growth.

Limited availability of sustainable aviation fuels, slow adoption of alternative propulsion systems, and inconsistent policies and regulations across different countries and regions are key factors restraining revenue growth of the market.

Asia Pacific is expected to account for the fastest revenue growth of 15.6%

Commercial aviation segment is the leading segment of aviation emissions control market in terms of application.

- Market Definition

- Research Objective

- Research Methodology

- Research Design

- Data Collection Methods

- Primary

- Secondary

- Market Size Estimation

- Top-down method

- Bottom-up method

- Forecasting Methodology

- Tools and Models Used

- Market Overview and Trends

- Market Size and Forecast

- Industry Analysis

- Market Driver, Restraints, Opportunity and Challenges (DROC) Analysis

- Market Drivers

- Stringent environmental regulations on aviation emissions

- Rising concerns about climate change

- Increasing adoption of sustainable aviation practices

- Growing government incentives and funding for using clean energy solutions in aviation

- Market Restraints

- Limited availability of sustainable aviation fuels

- Slow adoption of alternative propulsion systems

- Inconsistent policies and regulations across different countries and regions

- Market Opportunities

- Development of advanced emissions control technologies

- Rising Investments in carbon offsetting programs

- Increasing expansion of global passenger and cargo air traffic

- Market Challenges

- Technological and operational challenges

- Infrastructure constraints

- Regulatory Landscape

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

- Strategic Insights

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Price Trend Analysis

- Value Chain Analysis

- Technological Trends

- Recent Developments

- Funding

- Merger and Acquisition

- Expansion

- Partnership and Collaboration

- Product/ Service Launch

- Component Market Revenue Estimates and Forecasts, 2022-2032

- Hardware

- Sensors

- Actuators

- Filters

- Others

- Software

- Emission Monitoring Software

- Predictive Maintenance Tools

- Others

- Services

- Installation Services

- Maintenance & Repair Services

- Hardware

- By Aircraft Type Market Revenue Estimates and Forecasts, 2022-2032

- Narrow-Body Aircraft

- Narrowbody Long-Haul Flights

- Narrowbody Medium-Haul Flights

- Narrowbody Short-Haul Flights

- Wide-Body Aircraft

- Widebody Long-Haul Flights

- Widebody Medium-Haul Flights

- Widebody Short-Haul Flights

- Regional Aircraft

- Regional Jet Long-Haul Flights

- Regional Jet Medium-Haul Flights

- Regional Jet Short-Haul Flights

- Turboprop Aircraft

- Turboprop Long-Haul Flights

- Turboprop Medium-Haul Flights

- Turboprop Short-Haul Flights

- Business Jets

- Helicopters

- Others

- Narrow-Body Aircraft

- Scenario Market Revenue Estimates and Forecasts, 2022-2032

- No Emissions Control

- Optimistic Scenario

- Ideal Scenario

- Most Likely Scenario

- Fuel Type Market Revenue Estimates and Forecasts, 2022-2032

- Bio-Jet Fuel

- Hydrogen

- Ammonia

- Liquefied Methane

- Others

- Application Market Revenue Estimates and Forecasts, 2022-2032

- Commercial Aviation

- Military Aviation

- Private Aviation

- Aviation Emissions Control Market Revenue Estimates and Forecasts by Region, 2022-2032, USD Million

- North America

- North America Aviation Emissions Control Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Hardware

- Sensors

- Actuators

- Filters

- Others

- Software

- Emission Monitoring Software

- Predictive Maintenance Tools

- Others

- Services

- Installation Services

- Maintenance & Repair Services

- Hardware

- North America Aviation Emissions Control Market By Aircraft Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Narrow-body Aircraft

- Narrowbody Long-Haul Flights

- Narrowbody Medium-Haul Flights

- Narrowbody Short-Haul Flights

- Wide-body Aircraft

- Widebody Long-Haul Flights

- Widebody Medium-Haul Flights

- Widebody Short-Haul Flights

- Regional Aircraft

- Regional Jet Long-Haul Flights

- Regional Jet Medium-Haul Flights

- Regional Jet Short-Haul Flights

- Turboprop Aircraft

- Turboprop Long-Haul Flights

- Turboprop Medium-Haul Flights

- Turboprop Short-Haul Flights

- Business Jets

- Helicopters

- Others

- Narrow-body Aircraft

- North America Aviation Emissions Control Market By Scenario, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- No Emissions Control

- Optimistic Scenario

- Ideal Scenario

- Most Likely Scenario

- North America Aviation Emissions Control Market By Fuel Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Bio-Jet Fuel

- Hydrogen

- Ammonia

- Liquefied Methane

- Others

- North America Aviation Emissions Control Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Commercial Aviation

- Military Aviation

- Private Aviation

- North America Aviation Emissions Control Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- United States

- Canada

- Mexico

- North America Aviation Emissions Control Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Europe

- Europe Aviation Emissions Control Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Hardware

- Sensors

- Actuators

- Filters

- Others

- Software

- Emission Monitoring Software

- Predictive Maintenance Tools

- Others

- Services

- Installation Services

- Maintenance & Repair Services

- Hardware

- Europe Aviation Emissions Control Market By Aircraft Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Narrow-body Aircraft

- Narrowbody Long-Haul Flights

- Narrowbody Medium-Haul Flights

- Narrowbody Short-Haul Flights

- Wide-body Aircraft

- Widebody Long-Haul Flights

- Widebody Medium-Haul Flights

- Widebody Short-Haul Flights

- Regional Aircraft

- Regional Jet Long-Haul Flights

- Regional Jet Medium-Haul Flights

- Regional Jet Short-Haul Flights

- Turboprop Aircraft

- Turboprop Long-Haul Flights

- Turboprop Medium-Haul Flights

- Turboprop Short-Haul Flights

- Business Jets

- Helicopters

- Others

- Narrow-body Aircraft

- Europe Aviation Emissions Control Market By Scenario, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- No Emissions Control

- Optimistic Scenario

- Ideal Scenario

- Most Likely Scenario

- Europe Aviation Emissions Control Market By Fuel Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Bio-Jet Fuel

- Hydrogen

- Ammonia

- Liquefied Methane

- Others

- Europe Aviation Emissions Control Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Commercial Aviation

- Military Aviation

- Private Aviation

- Europe Aviation Emissions Control Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- Germany

- United Kingdom

- France

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Europe Aviation Emissions Control Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Asia-Pacific

- Asia-Pacific Aviation Emissions Control Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Hardware

- Sensors

- Actuators

- Filters

- Others

- Software

- Emission Monitoring Software

- Predictive Maintenance Tools

- Others

- Services

- Installation Services

- Maintenance & Repair Services

- Hardware

- Asia-Pacific Aviation Emissions Control Market By Aircraft Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Narrow-body Aircraft

- Narrowbody Long-Haul Flights

- Narrowbody Medium-Haul Flights

- Narrowbody Short-Haul Flights

- Wide-body Aircraft

- Widebody Long-Haul Flights

- Widebody Medium-Haul Flights

- Widebody Short-Haul Flights

- Regional Aircraft

- Regional Jet Long-Haul Flights

- Regional Jet Medium-Haul Flights

- Regional Jet Short-Haul Flights

- Turboprop Aircraft

- Turboprop Long-Haul Flights

- Turboprop Medium-Haul Flights

- Turboprop Short-Haul Flights

- Business Jets

- Helicopters

- Others

- Narrow-body Aircraft

- Asia-Pacific Aviation Emissions Control Market By Scenario, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- No Emissions Control

- Optimistic Scenario

- Ideal Scenario

- Most Likely Scenario

- Asia-Pacific Aviation Emissions Control Market By Fuel Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Bio-Jet Fuel

- Hydrogen

- Ammonia

- Liquefied Methane

- Others

- Asia-Pacific Aviation Emissions Control Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Commercial Aviation

- Military Aviation

- Private Aviation

- Asia-Pacific Aviation Emissions Control Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- China

- India

- Japan

- South Korea

- Oceania

- ASEAN Countries

- Rest of Asia-Pacific

- Asia-Pacific Aviation Emissions Control Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Latin America

- Latin America Aviation Emissions Control Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Hardware

- Sensors

- Actuators

- Filters

- Others

- Software

- Emission Monitoring Software

- Predictive Maintenance Tools

- Others

- Services

- Installation Services

- Maintenance & Repair Services

- Hardware

- Latin America Aviation Emissions Control Market By Aircraft Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Narrow-body Aircraft

- Narrowbody Long-Haul Flights

- Narrowbody Medium-Haul Flights

- Narrowbody Short-Haul Flights

- Wide-body Aircraft

- Widebody Long-Haul Flights

- Widebody Medium-Haul Flights

- Widebody Short-Haul Flights

- Regional Aircraft

- Regional Jet Long-Haul Flights

- Regional Jet Medium-Haul Flights

- Regional Jet Short-Haul Flights

- Turboprop Aircraft

- Turboprop Long-Haul Flights

- Turboprop Medium-Haul Flights

- Turboprop Short-Haul Flights

- Business Jets

- Helicopters

- Others

- Narrow-body Aircraft

- Latin America Aviation Emissions Control Market By Scenario, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- No Emissions Control

- Optimistic Scenario

- Ideal Scenario

- Most Likely Scenario

- Latin America Aviation Emissions Control Market By Fuel Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Bio-Jet Fuel

- Hydrogen

- Ammonia

- Liquefied Methane

- Others

- Latin America Aviation Emissions Control Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Commercial Aviation

- Military Aviation

- Private Aviation

- Latin America Aviation Emissions Control Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- Brazil

- Rest of Latin America

- Latin America Aviation Emissions Control Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Middle East & Africa

- Middle East & Africa Aviation Emissions Control Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Hardware

- Sensors

- Actuators

- Filters

- Others

- Software

- Emission Monitoring Software

- Predictive Maintenance Tools

- Others

- Services

- Installation Services

- Maintenance & Repair Services

- Hardware

- Middle East & Africa Aviation Emissions Control Market By Aircraft Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Narrow-body Aircraft

- Narrowbody Long-Haul Flights

- Narrowbody Medium-Haul Flights

- Narrowbody Short-Haul Flights

- Wide-body Aircraft

- Widebody Long-Haul Flights

- Widebody Medium-Haul Flights

- Widebody Short-Haul Flights

- Regional Aircraft

- Regional Jet Long-Haul Flights

- Regional Jet Medium-Haul Flights

- Regional Jet Short-Haul Flights

- Turboprop Aircraft

- Turboprop Long-Haul Flights

- Turboprop Medium-Haul Flights

- Turboprop Short-Haul Flights

- Business Jets

- Helicopters

- Others

- Narrow-body Aircraft

- Middle East & Africa Aviation Emissions Control Market By Scenario, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- No Emissions Control

- Optimistic Scenario

- Ideal Scenario

- Most Likely Scenario

- Middle East & Africa Aviation Emissions Control Market By Fuel Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Bio-Jet Fuel

- Hydrogen

- Ammonia

- Liquefied Methane

- Others

- Middle East & Africa Aviation Emissions Control Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Commercial Aviation

- Military Aviation

- Private Aviation

- Middle East & Africa Aviation Emissions Control Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of Middle East & Africa

- Middle East & Africa Aviation Emissions Control Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Market Share Analysis

- Revenue Market Share by Key Players (2023-2024)

- Analysis of Top Players by Market Presence

- Competitive Matrix

- Competitive Strategies

- Mergers and Acquisitions

- Partnerships and Collaboration

- Investment and Fundings

- Agreement

- Expansion

- New Product/ Services Launches

- Technological Innovations

- Airbus SE

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Embraer S.A.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Rolls-Royce Holdings Plc

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- GE Aerospace (General Electric)

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Pratt & Whitney

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Safran Group

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Neste Corporation

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Gevo, Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Aemetis, Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Thales Group

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Indra Sistemas, S.A

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Collins Aerospace

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Textron Aviation

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- MTU Aero Engines

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis