Global Floating Offshore Wind Power Market Overview and Key Insights:

The global floating offshore wind power market reached USD 304.7 million in 2024 and is expected to register a revenue CAGR of 43.6% during the forecast period. Rising concern about climate change, increasing demand for energy consumption across the globe, growing investments in renewable energy stringent regulations on reducing carbon emissions are expected to drive the revenue growth of the market.

Market Drivers:

Increasing demand for energy consumption across the globe is the major factor driving revenue growth of the floating offshore wind power market. There is a rising demand for reliable, sustainable, and renewable energy sources due to increasing population, urbanization, and industrialization. Global energy consumption experienced accelerated growth in 2023, increasing by 2.2% and surpassing its historical trend. This surge was mainly due to the BRICS countries. These countries collectively accounted for 42% of global energy usage. Among these, China saw a remarkable 6.6% rise, doubling its average annual growth rate. India also recorded a 5.1% increase, slightly outpacing its historical average. Brazil’s energy consumption also grew by 3.3%. This rising energy demand is driving revenue growth of offshore wind power market.

Additionally, the push for decarbonization and net-zero emission targets by governments and industries worldwide has increased the focus on renewable energy solutions. The global community is striving to limit the rise in average global temperatures to 1.5 degrees Celsius this century. They are trying to rapidly decarbonize hard-to-abate sectors. A historic commitment was made at the 2023 United Nations Climate Change Conference (COP 28) in Dubai, UAE to triple renewable energy capacity and double energy efficiency by 2030. In 2023, renewables accounted for 87% of new power capacity additions and 43% of the global installed power generation. It is achieving record annual growth. Offshore wind power has emerged as a central component of energy transition strategies and has become known for increasing cost competitiveness and high-capacity factors.

Market Opportunity:

Increasing government initiatives to promote renewable energy projects is creating significant opportunities for the floating offshore wind power market. It is prompting the manufacturer to accelerate investments in floating offshore wind projects. As of 2023, the world’s largest offshore wind farm is the Hornsea 2 project in the United Kingdom, boasting a capacity of 1,386 GW and comprising 165 turbines, each rated at 8 MW. Meanwhile, the Dogger Bank project, also located off the east coast of the United Kingdom, is set to become the largest offshore wind farm currently under construction. The first set of General Electric (GE) Vernova Haliade-X 13 MW turbines has already been installed at Dogger Bank. Remarkably, the 107-meter blades on the initial operational turbine are capable of generating enough clean energy to power an average home for two days with a single rotation.

Recent Trends:

One recent trend in the floating offshore wind power market is the development of larger, more efficient floating wind turbines, which are designed to harness stronger winds in deeper waters that fixed-bottom turbines cannot reach. Companies are focusing on improving the scalability of floating wind farms, with the installation of larger turbines and more advanced materials to enhance energy production. Additionally, there has been a push toward the commercialization of floating offshore wind farms, with projects moving from pilot phases to larger-scale developments.

This trend is further supported by rising investments in offshore wind infrastructure. Offshore wind investments reached a record high in 2023, totaling USD 76.7 billion, marking a 79% increase. China led the global offshore wind market, followed by the UK and the US. In addition, Companies such as Orsted, Iberdrola, Northland Power, and Mitsui & Co. were among those making final investment decisions on significant projects in 2023. In August 2024, TotalEnergies plans to install a 3-MW floating wind turbine to provide power to its Culzean gas-oil production facility in the UK central North Sea. Located 2 km west of the Culzean platform, the turbine is expected to be fully operational by the end of 2025, supplying around 20% of the field’s power requirements.

Restraints & Challenges:

Supply chain limitations are significantly restraining the revenue growth of the floating offshore wind power market. A study by the Global Wind Energy Council (GWEC) highlights increasing volatility in supply chains, driven by issues such as insufficient bids in auctions and defects in critical wind turbine components like foundations and blades. The study also points out that the lingering effects of the COVID-19 pandemic have adversely impacted capital and operating expenditures (CAPEX and OPEX) for wind projects. The offshore wind supply chain logistics and activities are becoming more complex due to a range of policy signals from various governments, along with a greater focus on localizing manufacturing capacities. These supply chain issues create uncertainty and delay the realization of large-scale offshore wind energy projects and ultimately limiting revenue growth of the market.

Component Segment Insights and Analysis:

Based on the component, the floating offshore wind power market is segmented into floating platforms, turbine and tower, blades, nacelle, mooring system, and power transmission system. Floating platforms segment is further sub-segmented into spar, barge, semi-submersible, tension-leg platform, and others. Mooring system segment is further sub-segmented into mooring lines, anchor and others. Power transmission system segment is further sub-segmented into power cables, offshore sub-station and others.

Floating Platforms segment contributed largest share in 2024 due to the increasing deployment of offshore wind projects in deeper waters. Floating platforms offer a versatile solution. It anchors wind turbines in locations with depths over 60 meters, tapping into stronger and more consistent wind resources. The demand for advanced platform designs, such as semi-submersible, spar-buoy, and tension-leg platforms, is growing as these structures provide stability, cost-efficiency, and adaptability to various sea conditions, which is boosting revenue growth of this segment.

In August 2024, A floating wind turbine platform designed by Mingyang Group has been deployed at an offshore wind farm in China. Known as OceanX, it currently represents the largest single-capacity technology of its kind. This platform is part of the 505-MW Yangjiang Mingyang Qingzhou IV project located near Guangdong, China. Mingyang announced the successful completion of the platform’s 191-nautical-mile journey from Guangzhou to the wind farm site off the coast of Guangdong Province. The company announced that the floating wind turbine platform features a “V” shape design and includes two 8.3-MW offshore wind turbines.

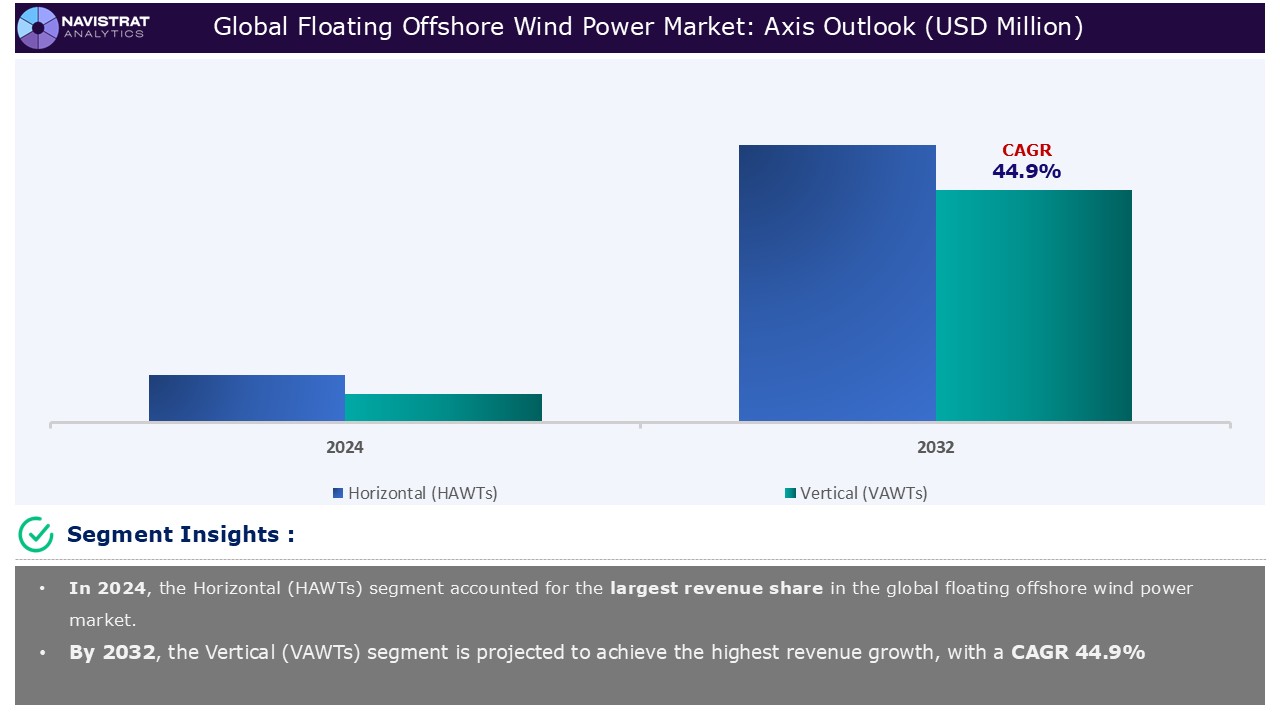

Axis Segment Insights and Analysis:

Based on axis, the floating offshore wind power market is segmented into Horizontal (HAWTs) and Vertical (VAWTs). Horizontal (HAWTs) segment is further sub-segmented into up-wind and down wind.

Horizontal (HAWTs) segment contributed largest share in 2024 due to proven efficiency, widespread adoption, and technological advancements. Wind turbines with horizontal rotor shafts and blade orientations facing the wind (HAWTs) dominate offshore projects because they offer high energy conversion efficiency and scalability. Floating platforms enable the deployment of HAWTs in deeper waters where wind speeds are stronger and more consistent, significantly boosting energy output. Technological innovations in blade design, materials, and turbine size have further enhanced their performance and durability and increase the demand for HAWTs.

Vertical (VAWTs) segment is expected to register a fast revenue growth rate during the forecast period due to the rising adoption of VAWTs in floating offshore wind power projects owing to its unique design advantages and suitability for offshore applications. VAWTs have a vertically oriented rotor shaft, allowing them to harness wind from all directions without requiring orientation mechanisms. This feature makes them highly effective in turbulent offshore wind conditions and simplifies their design, reducing maintenance requirements.

In September 2022, Norwegian shipyard group Westcon has partnered with Sweden-based company SeaTwirl to install 1MW vertical axis wind turbines in the North Sea. This commercial-scale vertical axis turbine could mark the beginning of a new phase in offshore wind farms, potentially achieving cost competitiveness in the near future. Unlike traditional horizontal axis turbines with three blades mounted atop tall towers, vertical axis technology offers greater flexibility in turbine height, paving the way for innovative offshore wind farm designs.

By Depth Segment Insights and Analysis:

Based on depth, the floating offshore wind power market is segmented into Shallow Water (0-30 meters), Transitional Water (31 – 50 meters), and Deep Water (50 meters+).

Transitional Water (31 – 50 meters) segment contributed largest share in 2024 due to the rising demand for this segment owing to its strategic balance between cost efficiency and access to favorable wind resources. Transitional waters feature higher wind speeds compared to shallow waters. It makes them ideal for harnessing more consistent and powerful wind energy. Additionally, advancements in floating platform technology have made it economically viable to deploy wind turbines in these depths, overcoming challenges associated with seabed anchoring.

The International Renewable Energy Agency (IRENA) expected that floating wind farms will contribute approximately 5% to 15% of the global offshore wind capacity, which could reach nearly 1,000 GW by 2050. This growing interest in floating wind farms arises from their ability to access sites with mid-depth conditions ranging from 30 to 50 meters. Furthermore, floating wind technology promises a more cost-effective and environmentally sustainable alternative to fixed-foundation systems.

Deep Water (50 meters+) segment is expected to have the fastest CAGR throughout the forecasted period. Deep-water locations typically experience higher and more consistent wind speeds, which significantly enhance energy generation efficiency. Governments and private sector players are increasingly investing in this segment due to its potential to produce large-scale renewable energy, especially in regions with limited shallow water areas. Additionally, the deployment of floating wind farms in deep waters reduces visual and environmental impacts near coastal regions, aligning with sustainability goals and public acceptance.

Geographical Outlook:

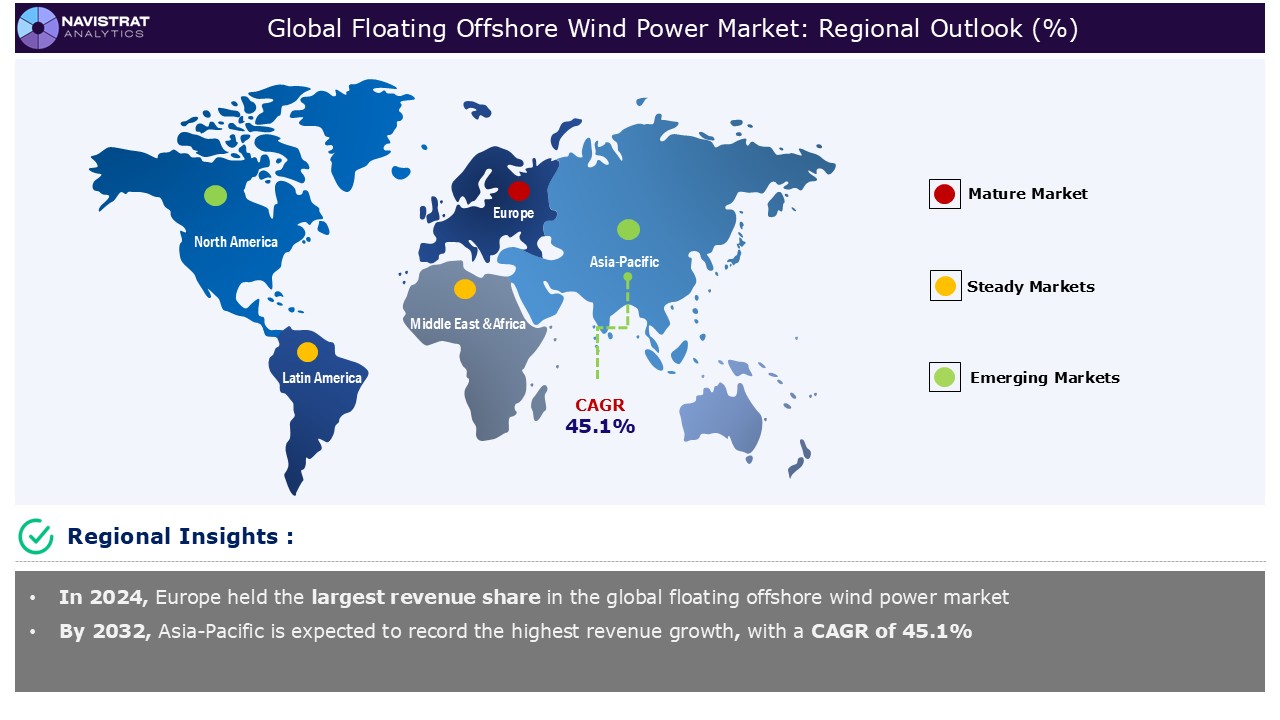

Market in Europe accounted for largest revenue share in 2024 due to its ambitious renewable energy targets and supportive regulatory frameworks in the country, especially in U.K., France, and Germany. The European Union’s Green Deal and its commitment to achieving net-zero emissions by 2050 have catalyzed investments in offshore wind, including floating technologies. The United Kingdom is a leader in the European offshore wind sector. In 2022, the country added approximately 3 GW of wind power capacity, with 90% of this coming from offshore wind projects. This sector is expected to grow at a compound annual growth rate of 14% from 2022 to 2030. With total capacity projected to reach 40 GW. In October 2023, the construction of the world’s largest offshore wind farm, Dogger Bank, began producing energy 130 kilometers off the coast of Yorkshire. The farm has featured 277 turbines, with a total installed capacity of 3.6 GW.

France also has set ambitious offshore wind goals, targeting 18 GW of installed capacity by 2035 and 45 GW by 2050. By 2023, the country had awarded 4.6 GW of offshore wind projects, with 2 GW either operational or under construction, and 3.4 GW in ongoing tenders. Annual tender volumes will increase to 2 GW starting in 2025 as part of the Sector Deal passed in March 2022. France plans to allocate 15.5 GW of new offshore wind projects within the next decade. In 2024, the country launched its second fully operational offshore wind farm, with a 500 MW capacity.

Asia Pacific is expected to register a fast revenue growth rate during the forecast period due to its robust renewable energy targets and favorable geographic conditions in countries, especially in China, Japan and India. China continues to lead the world in offshore wind development, adding an impressive 16.9 GW of offshore capacity in 2021. The country’s offshore wind projects are concentrated in regions such as Fujian, Guangdong, Guangxi, and Jiangsu. Under its 14th Five-Year Plan (2021-2025), China has reinforced its commitment to renewable energy. The country is targeting renewables to account for more than 50% of the total new primary energy consumption.

Japan has set ambitious goals to boost its offshore wind power capacity to 10 GW by 2030 and further to 30-45 GW by 2040. To achieve these objectives, the country resumed public auctions for offshore wind projects in December 2022, introducing updated rules. Projects with earlier start dates receive higher scores. Any single consortium faces a 1 GW capacity limit when multiple ocean areas are auctioned. Japan has already conducted two auctions with capacities of 1.5 GW and 1.8 GW. A third auction launched in January 2024 aims to allocate 1.1 GW of capacity. The Noshiro Port Offshore Wind Farm, Japan’s first commercial full-scale offshore wind facility with a capacity of 84 MW. It became operational at the end of December 2022.

Market in North America accounted for a significant revenue share in 2024 due to the combination of favorable government policies, increasing investments, and significant offshore wind resource potential in the region, especially in U.S and Canada. The United States has made strong commitments to expanding renewable energy. The country is taking initiatives such as the Biden Administration’s target to deploy 30 GW of offshore wind energy by 2030, including floating wind projects. Additionally, advancements in floating wind technology have opened opportunities to harness the vast wind resources available in deep waters off the coasts of California and Maine. These projects benefit from federal and state-level tax incentives, competitive auction processes, and partnerships with private developers.

Canada also possesses a vast offshore wind technical potential. Beginning in 2025, Nova Scotia plans to offer leases aimed at developing 5 GW of offshore wind energy by 2030. It is focusing on integrating this energy production with hydrogen generation. Supporting this initiative, Canada and Germany have established the Canada-Germany Hydrogen Alliance. It is enabling Canada to export green hydrogen to Germany by 2025. The leasing process for offshore wind development in Nova Scotia will follow a competitive bidding format, co-managed by provincial and federal authorities, with the first call for bids expected in 2025.

Competition Analysis:

The floating offshore wind power market is characterized by a fragmented structure, with numerous players competing across various segments and regions. List of major players included in the floating offshore wind power market report are:

- Ørsted A/S

- Equinor ASA

- Siemens Gamesa Renewable Energy

- GE Vernova

- Vestas Wind Systems

- BW Ideol AS

- Principle Power

- Blue H Technologies

- RWE

- MODEC, Inc

- Iberdrola, S.A

- TechnipFMC plc

Strategic Developments in Global Floating Offshore Wind Power Market:

- On 19 July 2024, ScottishPower Renewables has entered into a £1 billion (UDS 1.2 billion) agreement with Siemens Gamesa. The aim of the agreement is to provide 15MW turbines for the East Anglia 2 (EA2) offshore wind farm off the east coast of England. The wind farm, with a nearly 1GW capacity, will feature 64 SG 14-236 DD offshore wind turbines from Siemens Gamesa, each with a rotor diameter of 236 meters.

- On 23 August 2023, Equinor, the Norwegian energy company, along with its partners, is officially inaugurate the world’s largest floating offshore wind farm. The Hywind Tampen wind farm, which started producing power in November of the previous year and reached full output earlier this month, would supply power to nearby oil and gas platforms. It helps to reduce their greenhouse gas emissions. The project, a collaboration with other oil companies like OMV and Vår Energi has a capacity of 88 megawatts. This will meet approximately 35% of the annual power needs of five platforms at the Snorre and Gullfaks oil and gas fields, located around 140 km off Norway’s west coast in the North Sea.

Key Advantages for Stakeholders:

Navistrat Analytics’ industry report provides an in-depth quantitative analysis of various market segments, historical and current trends, market forecasts, and dynamics within the global market. The historical years covered in this report are 2022 to 2023, with 2024 serving as the base year for market size calculations. The forecast period extends from 2025 to 2032.

The report includes an executive summary and a comprehensive overview of market drivers, restraints, opportunities, and challenges (DROC). It also provides insights into regulatory standards. It features detailed analyses such as PORTER’s Five Forces, SWOT, and PESTLE, as well as assessments of technological trends and the competitive landscape.

PORTER’s Five Forces analysis helps stakeholders evaluate the impact of new entrants, competitive rivalry, supplier power, buyer power, and substitution threats. It is enabling them to assess the level of competition and the attractiveness of the global market. The competitive landscape provides stakeholders with a clear understanding of the current market positions of key players. It is offering valuable insights into their competitive environment.

Scope And Key Highlights of The Global Floating Offshore Wind Power Market Report:

| Report Features | Details |

| Market Size in 2024 | USD 304.7 Million |

| Market Growth Rate in CAGR (2025–2032) | 43.6% |

| Market Revenue Forecast to 2032 | USD 5,326.4 Million |

| Base year | 2024 |

| Historical year | 2022–2023 |

| Forecast period | 2025–2032 |

| Report Pages | 450 |

| Segments Covered |

|

| Regional scope |

|

| Country Scope |

|

| Key Market Players |

|

| Delivery Format | Reports are delivered in PDF format via email. |

| Customization Scope | Request for Customization |

The floating offshore wind power market report offers a detailed analysis of market size, including historical revenue (in USD Million) data for 2022-2023 and revenue forecasts for 2025-2032 across the following segments:

- Component Outlook (Revenue, USD Million; 2022-2032)

- Floating Platforms

- Spar

- Barge

- Semi-Submersible

- Tension-Leg Platform

- Others

- Turbine and Tower

- Blades

- Nacelle

- Mooring system

- Mooring Lines

- Anchor

- Others

- Power Transmission System

- Power Cables

- Offshore Sub-Station

- Others

- Floating Platforms

- Axis Outlook (Revenue, USD Million; 2022-2032)

- Horizontal (HAWTs)

- Up-wind

- Downwind

- Vertical (VAWTs)

- Horizontal (HAWTs)

- Depth (Revenue, USD Million; 2022-2032)

- Shallow Water (0-30 meters)

- Transitional Water (31 – 50 meters)

- Deep Water (50 meters+)

- Turbine Capacity Outlook (Revenue, USD Million; 2022-2032)

- Upto 2 MW

- 2 to 5 MW

- 6 to 10 MW

- Above 10 MW

- Regional Outlook (Revenue, USD Million; 2022-2032)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Oceania

- ASEAN Countries

- Rest of APAC

- Latin America

- Brazil

- Rest of LATAM

- Middle East & Africa

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of MEA

- North America

Frequently Asked Questions (FAQ) about the Floating Offshore Wind Power Market report

The global floating offshore wind power market size was USD 304.7 Million in 2024.

The global floating offshore wind power market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 43.6% during the forecast period.

Rising concern about climate change, increasing demand for energy consumption across the globe, growing investments in renewable energy stringent regulations on reducing carbon emissions are the key drivers of the floating offshore wind power market revenue growth.

High initial capital investment, grid Integration and Infrastructure limitations, and rising competition from other renewable sources are key factors restraining revenue growth of the market.

Asia Pacific is expected to account for the fastest revenue growth of 45.1%

Horizontal (HAWTs) segment is the leading segment of floating offshore wind power market in terms of axis.

- Market Definition

- Research Objective

- Research Methodology

- Research Design

- Data Collection Methods

- Primary

- Secondary

- Market Size Estimation

- Top-down method

- Bottom-up method

- Forecasting Methodology

- Tools and Models Used

- Market Overview and Trends

- Market Size and Forecast

- Industry Analysis

- Market Driver, Restraints, Opportunity and Challenges (DROC) Analysis

- Market Drivers

- Rising concern about climate change

- Increasing demand for energy consumption across the globe

- Growing investments in renewable energy

- Stringent regulations on reducing carbon emissions

- Market Restraints

- High initial capital investment

- Grid integration and infrastructure limitations

- Rising competition from other renewable sources

- Market Opportunities

- Improvement in floating wind turbine technology

- Rising collaboration between government agencies and private investors

- Increasing government initiatives to promote renewable energy projects

- Market Challenges

- Regulatory and permitting challenges

- Supply chain limitations

- Regulatory Landscape

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

- Strategic Insights

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Price Trend Analysis

- Value Chain Analysis

- Technological Trends

- Recent Developments

- Funding

- Merger and Acquisition

- Expansion

- Partnership and Collaboration

- Product/ Service Launch

- Component Market Revenue Estimates and Forecasts, 2022-2032

- Floating Platforms

- Spar

- Barge

- Semi-Submersible

- Tension-Leg Platform

- Others

- Turbine and Tower

- Blades

- Nacelle

- Mooring system

- Mooring Lines

- Anchor

- Others

- Power Transmission System

- Power Cables

- Offshore Sub-Station

- Others

- Floating Platforms

- By Axis Market Revenue Estimates and Forecasts, 2022-2032

- Horizontal (HAWTs)

- Up-wind

- Downwind

- Vertical (VAWTs)

- Horizontal (HAWTs)

- Depth Market Revenue Estimates and Forecasts, 2022-2032

- Shallow Water (0-30 meters)

- Transitional Water (31 – 50 meters)

- Deep Water (50 meters+)

- Turbine Capacity Market Revenue Estimates and Forecasts, 2022-2032

- Upto 2 MW

- 2 to 5 MW

- 6 to 10 MW

- Above 10 MW

- Floating Offshore Wind Power Market Revenue Estimates and Forecasts by Region, 2022-2032, USD Million

- North America

- North America Floating Offshore Wind Power Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Floating Platforms

- Spar

- Barge

- Semi-Submersible

- Tension-Leg Platform

- Others

- Turbine And Tower

- Blades

- Nacelle

- Mooring System

- Mooring Lines

- Anchor

- Others

- Power Transmission System

- Power Cables

- Offshore Sub-Station

- Others

- Floating Platforms

- North America Floating Offshore Wind Power Market By Axis, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Horizontal (HAWTs)

- Up-wind

- Downwind

- Vertical (VAWTs)

- Horizontal (HAWTs)

- North America Floating Offshore Wind Power Market By Depth, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Shallow Water (0-30 meters)

- Transitional Water (31 – 50 meters)

- Deep Water (50 meters+)

- North America Floating Offshore Wind Power Market By Turbine Capacity, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Upto 2 MW

- 2 to 5 MW

- 6 to 10 MW

- Above 10 MW

- North America Floating Offshore Wind Power Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- United States

- Canada

- Mexico

- North America Floating Offshore Wind Power Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Europe

- Europe Floating Offshore Wind Power Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Floating Platforms

- Spar

- Barge

- Semi-Submersible

- Tension-Leg Platform

- Others

- Turbine And Tower

- Blades

- Nacelle

- Mooring System

- Mooring Lines

- Anchor

- Others

- Power Transmission System

- Power Cables

- Offshore Sub-Station

- Others

- Floating Platforms

- Europe Floating Offshore Wind Power Market By Axis, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Horizontal (HAWTs)

- Up-wind

- Downwind

- Vertical (VAWTs)

- Horizontal (HAWTs)

- Europe Floating Offshore Wind Power Market By Depth, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Shallow Water (0-30 meters)

- Transitional Water (31 – 50 meters)

- Deep Water (50 meters+)

- Europe Floating Offshore Wind Power Market By Turbine Capacity, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Upto 2 MW

- 2 to 5 MW

- 6 to 10 MW

- Above 10 MW

- Europe Floating Offshore Wind Power Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- Germany

- United Kingdom

- France

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Europe Floating Offshore Wind Power Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Asia-Pacific

- Asia-Pacific Floating Offshore Wind Power Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Floating Platforms

- Spar

- Barge

- Semi-Submersible

- Tension-Leg Platform

- Others

- Turbine And Tower

- Blades

- Nacelle

- Mooring System

- Mooring Lines

- Anchor

- Others

- Power Transmission System

- Power Cables

- Offshore Sub-Station

- Others

- Floating Platforms

- Asia-Pacific Floating Offshore Wind Power Market By Axis, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Horizontal (HAWTs)

- Up-wind

- Downwind

- Vertical (VAWTs)

- Horizontal (HAWTs)

- Asia-Pacific Floating Offshore Wind Power Market By Depth, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Shallow Water (0-30 meters)

- Transitional Water (31 – 50 meters)

- Deep Water (50 meters+)

- Asia-Pacific Floating Offshore Wind Power Market By Turbine Capacity, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Upto 2 MW

- 2 to 5 MW

- 6 to 10 MW

- Above 10 MW

- Asia-Pacific Floating Offshore Wind Power Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- China

- India

- Japan

- South Korea

- Oceania

- ASEAN Countries

- Rest of Asia-Pacific

- Asia-Pacific Floating Offshore Wind Power Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Latin America

- Latin America Floating Offshore Wind Power Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Floating Platforms

- Spar

- Barge

- Semi-Submersible

- Tension-Leg Platform

- Others

- Turbine And Tower

- Blades

- Nacelle

- Mooring System

- Mooring Lines

- Anchor

- Others

- Power Transmission System

- Power Cables

- Offshore Sub-Station

- Others

- Floating Platforms

- Latin America Floating Offshore Wind Power Market By Axis, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Horizontal (HAWTs)

- Up-wind

- Downwind

- Vertical (VAWTs)

- Horizontal (HAWTs)

- Latin America Floating Offshore Wind Power Market By Depth, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Shallow Water (0-30 meters)

- Transitional Water (31 – 50 meters)

- Deep Water (50 meters+)

- Latin America Floating Offshore Wind Power Market By Turbine Capacity, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Upto 2 MW

- 2 to 5 MW

- 6 to 10 MW

- Above 10 MW

- Latin America Floating Offshore Wind Power Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- Brazil

- Rest of Latin America

- Latin America Floating Offshore Wind Power Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Middle East & Africa

- Middle East & Africa Floating Offshore Wind Power Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Floating Platforms

- Spar

- Barge

- Semi-Submersible

- Tension-Leg Platform

- Others

- Turbine And Tower

- Blades

- Nacelle

- Mooring System

- Mooring Lines

- Anchor

- Others

- Power Transmission System

- Power Cables

- Offshore Sub-Station

- Others

- Floating Platforms

- Middle East & Africa Floating Offshore Wind Power Market By Axis, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Horizontal (HAWTs)

- Up-wind

- Downwind

- Vertical (VAWTs)

- Horizontal (HAWTs)

- Middle East & Africa Floating Offshore Wind Power Market By Depth, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Shallow Water (0-30 meters)

- Transitional Water (31 – 50 meters)

- Deep Water (50 meters+)

- Middle East & Africa Floating Offshore Wind Power Market By Turbine Capacity, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Upto 2 MW

- 2 to 5 MW

- 6 to 10 MW

- Above 10 MW

- Middle East & Africa Floating Offshore Wind Power Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of Middle East & Africa

- Middle East & Africa Floating Offshore Wind Power Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Market Share Analysis

- Revenue Market Share by Key Players (2023-2024)

- Analysis of Top Players by Market Presence

- Competitive Matrix

- Competitive Strategies

- Mergers and Acquisitions

- Partnerships and Collaboration

- Investment and Fundings

- Agreement

- Expansion

- New Product/ Services Launches

- Technological Innovations

- Ørsted A/S

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Equinor ASA

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Siemens Gamesa Renewable Energy

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- GE Vernova

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Vestas Wind Systems

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- BW Ideol AS

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Principle Power

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Blue H Technologies

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- RWE

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- MODEC, Inc

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Iberdrola, S.A

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- TechnipFMC Plc

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis