Heterogeneous Integration Market Overview and Key Insights:

The global heterogeneous integration market size reached USD 3.13 Billion in 2024 and is expected to register a revenue CAGR of 34.5 % during the forecast period. Growing demand for high-performance computing (HPC), AI, and mobile computing is a major factor driving the revenue growth of the heterogeneous integration market.

Heterogeneous integration and chiplet-based designs enhance system performance for training large volumes of data across artificial intelligence (AI), machine learning, scientific simulations, and real-time analytics. According to research, around 402.74 million terabytes of data are generated each day.

HPC applications requires tens to hundreds of times densities greater than conventional Flip-Chip Ball Grid Array (FCBGA) packages. Heterogeneous integration addresses the requirements of higher number of interconnections compared to traditional monolithic system-on-chip (SoC) designs.

Market Drivers:

The exponential rise in demand for electric vehicles (EVs) is expected to drive market revenue growth for heterogeneous integration (HI). According to the International Energy Agency (IEA), around 14 million new electric vehicles (EVs) were registered globally in 2023. Electric vehicles (EVs) sales in 2023 experienced significant growth, reaching 3.5 million units higher than 2022, representing a robust 35% year-on-year increase.

Heterogeneous integration combines various components such as sensors, Microelectromechanical Systems (MEMS), Integrated Circuits (ICs), filters, power amplifiers into a single package, which helps in facilitating faster and more accurate data processing for Advanced Driver Assistance Systems (ADAS), Light Detection and Ranging (LiDAR).

Heterogeneous integration (HI) is highly useful in power electronics of electric vehicles and autonomous systems. The Silicon Carbide (SiC) and Generative Adversarial Network (GaN) packaged control circuits optimize power conversion efficiency by minimizing heat generation, making EV powertrains more power efficient, Additionally, Heterogeneous integration combines various processors and sensors into a single package, which helps improve overall safety and safety of battery management systems (BMS).

Market Opportunity:

Deployment of 5G networks globally is expected to drive substantial growth opportunities in the heterogeneous integration market. According to the GSM Association, global 5G connections are expected to surpass 2 billion by 2025. Heterogeneous integration (HI) helps in address bandwidth congestion and enhance the of Radio Frequency (RF) and optical networks in 5G+ heterogeneous networks (HetNets). Also, 5G-enabled heterogeneous packages are designed to optimize bandpass filters for 5G NR mmWave bands like n257, n258, and n260, by ensuring low insertion loss, high selectivity, and compact footprints.

Governments across the world are mandating sustainable practices across industries which are expected to drive the demand for heterogeneous integration. According to the Paris Agreement of the United Nations (UN), the earth’s average temperature is currently around 1.2°C, the emissions need to be reduced by 45% by 2030 and reach net zero by 2050.

Heterogeneous integration (HI) minimizes computation demands and extends the usability of components across multiple generations of integrated circuits (ICs). Additionally, the hierarchical system design strategies enable energy-efficient and low-power semiconductor lifecycle, while significantly reducing embodied carbon emissions.

Recent Trends:

Integration of multi-chip(let) architecture and Fan-Out Wafer Level Packaging (FOWLP) are emerging as a key industry trend in heterogeneous integration market. The heterogeneous integration market trends are shifting towards innovative and power-efficient solutions that enhance the overall performance and functionality of products. Multi-chip(let) architectures are a modular and flexible alternative to conventional monolithic System-on-Chip (SoC) designs.

Fan-out Wafer Level Packaging (FOWLP) supports this trend by enabling high-density interconnects and reducing overall footprint of chip assemblies. Manufacturers can deliver compact, optimized, and high-performance packages for power efficiency and scalability by combining advanced chiplet designs with FOWLP.

Restraints & Challenges:

Disruption in supply chain of materials and components is a major factor hindering the market revenue growth. Production of heterogeneous integration (HI) depends on sourcing critical materials such as Silicon Carbide (SiC), Gallium Nitride (GaN), copper, aluminium, germanium, and various other chemicals and materials.

According to the Center for Strategic & International Studies (CSIS), China produces around 98 % of the world’s supply of raw gallium. In December 2023, China announced a ban on allium, germanium, and antimony to the United States. These concerns are creating a complete monopoly over sourcing critical materials which are significantly affecting revenue growth.

Moreover, ongoing geopolitical conflicts between countries such as China and Taiwan, Russia, and Ukraine are emerging as a major challenge of heterogeneous integration market. The production process of developing heterogeneous integration (HI) components requires gases like neon. According to a study by the European Union (EU), Ukraine holds around 40% and 70% of the world’s neon production and accounts for almost 70% of the world’s neon gas capacity. These factors are expected to hinder the market revenue growth over the forecast period.

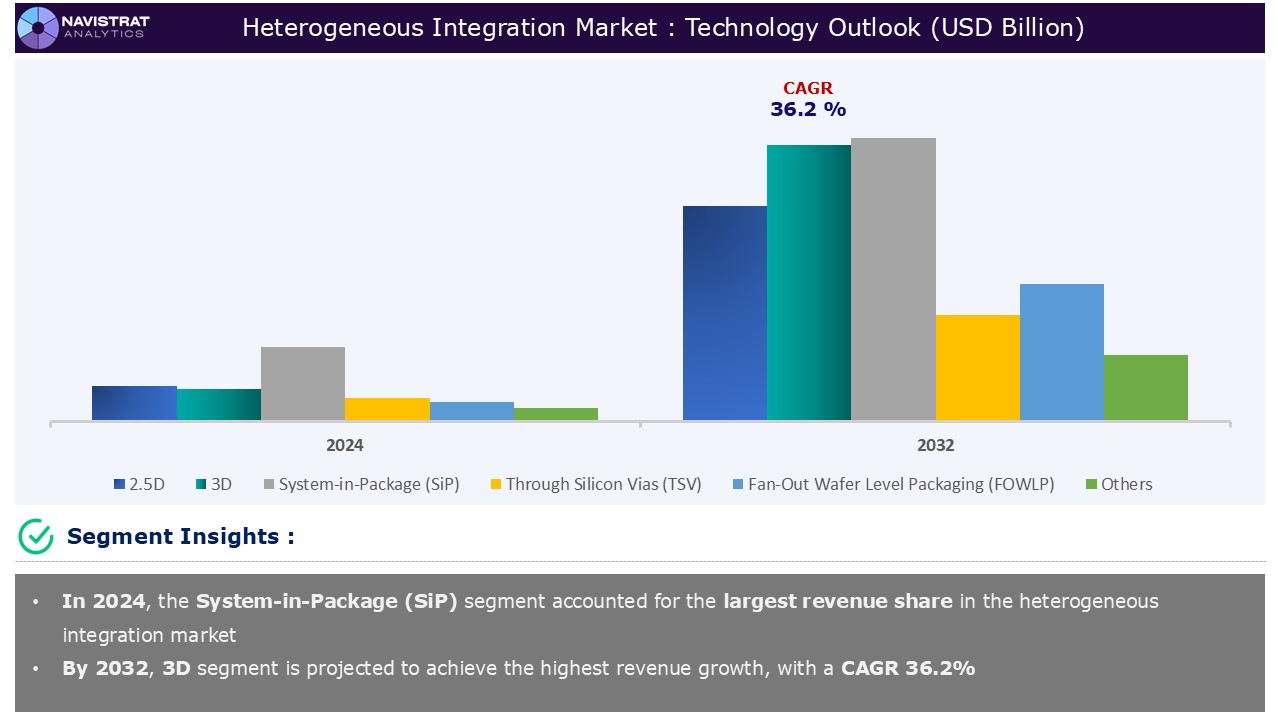

Technology Segment Insights and Analysis:

Based on the technology, the heterogeneous integration market is segmented into 2.5D, 3D, System-in-Package (SiP), Through Silicon Vias (TSV), Fan-Out Wafer Level Packaging (FOWLP), and others.

The System-in-Package (SiP) contributed the largest revenue share in 2024. System-in-Package (SiP) technology can integrate multiple components such as processors, memory, and sensors, into a compact package. Integrating components into a single package helps companies to reduce material, assembly, and testing costs. Furthermore, SiP’s ability to accelerate development cycles and improve time-to-market is a key competitive advantage of heterogeneous integration market.

The 3D segment is expected to register the fastest revenue growth over the forecast period. Increasing demand for higher computational power and system integration is driving the adoption of 3D heterogeneous integration (HI). The design of 3D heterogeneous integration helps in stacking multiple die/wafer layers vertically to create multilayer semiconductor packages.

This vertical stacking minimizes the length of interconnects which significantly enhances performance by reducing signal delays and power consumption. This vertical stacking minimizes the length of interconnects required for routing electrical signals, enhancing the performance of the system by reducing signal delays and power consumption. Moreover, government initiatives, such as the U.S. Department of Defense’s Next-Generation Microelectronics Manufacturing (NGMM) program are promoting investments in 3D heterogeneous integration (HI) technologies.

Component Segment Insights and Analysis:

Based on the component, the heterogeneous integration market is segmented into hardware and software.

The hardware segment will be sub-segmented into the key areas of sensors and MEMS, integrated circuits (ICs), filters, power amplifiers, and others.

Moreover, the software segment will be sub-segmented into the areas of Integration and testing, system modeling and simulation, electronic design automation (EDA) and others.

The hardware segment contributed the largest revenue share in 2024. Rapid integration of microelectromechanical systems (MEMS) with integrated circuits (ICs) across consumer electronics, automotive, IT and telecommunications, aerospace, and defense applications contributed to market revenue growth of heterogeneous integration market. Increasing incorporation of components such as MEMS, integrated circuits (ICs), filters, and power amplifiers to design system-on-chip (SoC) has also supported market share expansion.

The software segment is expected to register fastest revenue growth over the forecast period. Rising demand for software to design monolithic system-on-chip (SoC) designs and multi-die systems is expected to drive market revenue growth in heterogeneous integration market. Also, the integration of various networks in military to civil applications requires software solutions that can effectively handle the heterogeneity of architectures, protocols, and switching mechanisms.

Advancements in Embedded Multi-die Interconnect Bridge (EMIB) technology are further projected to accelerate market revenue growth over the forecast period. In February 2024, Cadence and Intel Foundry collaborated to develop an integrated advanced packaging flow that uses Embedded Multi-die Interconnect Bridge (EMIB) technology to address challenges associated with heterogeneously integrated multi-chip(let) architectures.

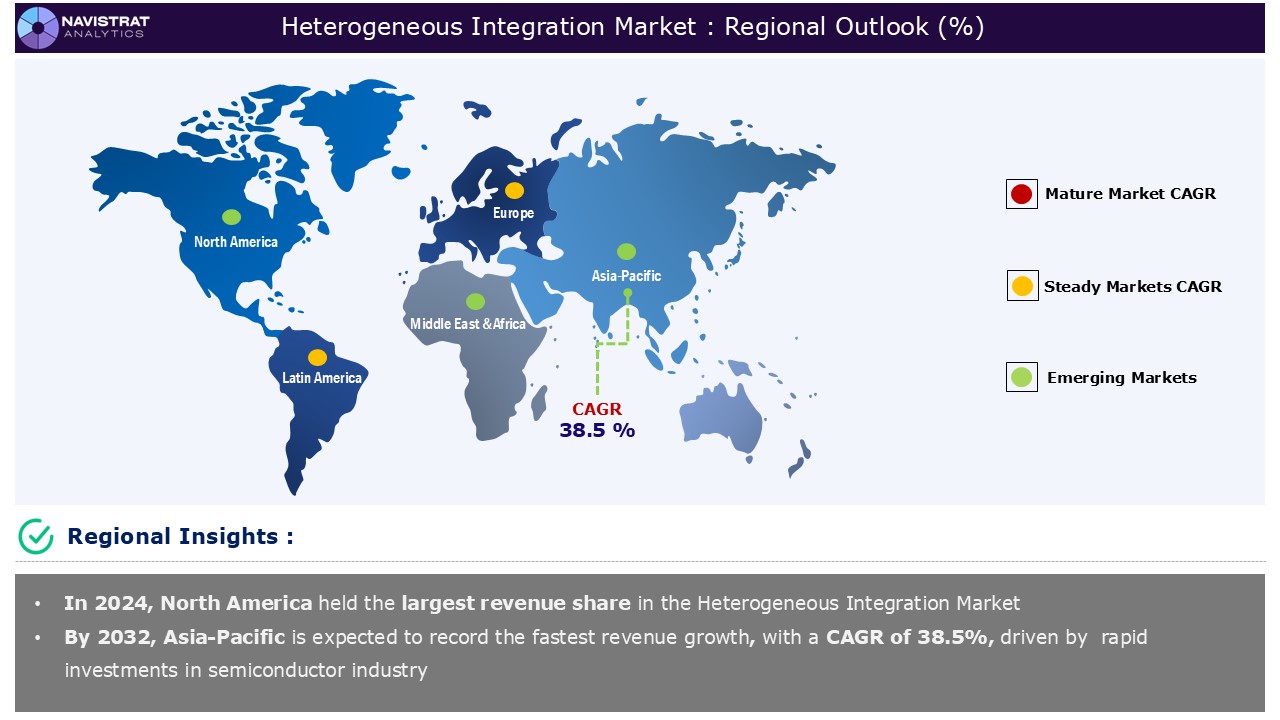

Geographical Outlook:

North America registered highest market share in the heterogeneous integration market. Rapid investment in semiconductor industry and chip-designing ecosystem has contributed to revenue growth in this region. The United States CHIPS and Science Act, 2022 catalyzed significant investments in the U.S. According to the Semiconductor Industry Association (SIA), as of august 2024 companies in the semiconductor ecosystem have announced over 90 new manufacturing projects in the United States, aggregating around USD 450 billion investments across 28 states.

Rapid investments in semiconductor packaging are further supporting the market revenue growth. For instance, In November 2024, the U.S. Department of Commerce (DOC) is negotiating a USD 300 million investment in advanced packaging research projects in Georgia, California, and Arizona to accelerate the development of cutting-edge semiconductor technologies.

Moreover, government support for tax credits has further accelerated the revenue growth in the U.S. The government of the United States has introduced the Semiconductor Technology Advancement and Research (STAR) Act of 2024, to strengthen the United States’ leadership and worldwide competitiveness in semiconductor design. The Act intends to encourage U.S. chip design companies by offering a 25% investment tax credit for design operations.

Asia Pacific is expected to register fastest revenue growth by 2032. The Asia-Pacific region serves as a key export hub of semiconductors. Countries such as China, Japan, and South Korea are playing a pivotal role in driving the growth of semiconductor export volumes. According to the Korea Trade Investment Promotion Agency (KOTRA), In 2022 Korea’s total export of semiconductors amounted to USD 129.2 billion.

Government initiatives in an expansion of the semiconductor industry in this region have further accelerated the market revenue growth of heterogeneous integration market. Industrial policies such as “Made in China 2025” and “Make in India” initiatives are significantly promoting domestic manufacturing of semiconductors.

Governments in this region are rapidly investing in semiconductor and electronics production to meet the growing demand for semiconductors across industries. In March 2024, the Government of India, invested USD 15.2 Billion to develop a state-of-the-art semiconductor fab. In May 2024, Government of the People’s Republic of China established its third planned state-backed investment fund to strengthen the semiconductor sector, with a registered capital of USD 47.5 billion.

Foreign Direct Investments (FDI) in the semiconductor industry are further driving the opportunities of the market. According to the Minister of Planning and Investment of Vietnam, as of December 2024, 174 foreign-invested semiconductor projects have been established, with a combined registered capital of approximately USD 11.6 billion.

Europe contributed a substantial revenue share in 2024. Deployment 5G networks across major countries in European Union (EU) is driving the demand for heterogeneous integration. According to the GSM Association, 5G adoption in Europe will soar to 80% by 2030.

Rapid investments in semiconductor research and innovation have also contributed to the market revenue expansion in this region. For instance, In February 2024, the European Union (EU) announced an investment of USD 350.7 million to support Europe’s semiconductor innovation ecosystem. Also, In July 2024, the EU announced additional funding of USD 351.37 million to support semiconductor research and innovation projects in photonics, competence centers.

Competition Analysis:

The heterogeneous integration market is characterized by a consolidated structure, with major players competing across various segments and regions. The list of major players included in the Heterogeneous Integration Market report are:

- ASE Technology Holding

- Applied Materials, Inc.

- Siemens AG

- Shin-Etsu Chemical Co., Ltd.

- Etron Technology, Inc.

- EV Group (EVG)

- Merck Group

- Samsung Electronics Co., Ltd.

- Kulicke & Soffa Industries, Inc.

- Northrop Grumman Corporation

- Intel Corporation

- Cadence Design Systems, Inc.

- Synopsys, Inc.

Strategic Developments in Heterogeneous Integration Market:

- On 31st October 2024, Merck completed acquisition of Unity-SC for USD 168.65 Million to strengthen the strategic focus of its Electronics business on semiconductor solutions. This includes the integration of its display and semiconductor business units. Merck aims to drive innovation in optoelectronics through the convergence of semiconductor and display technologies by leveraging its existing capabilities.

- On 24th June 2024, Siemens Digital Industries Software introduced Innovator3D IC, a new software solution designed to streamline the planning and heterogeneous integration of ASICs and chiplets utilizing cutting-edge 2.5D and 3D semiconductor packaging technologies and substrates. Innovator3D IC offers a unified platform for constructing a digital twin of the entire semiconductor package assembly, featuring a consolidated data model for design planning, prototyping, and predictive analysis.

Key Advantages for Stakeholders:

Navistrat Analytics’ industry report provides an in-depth quantitative analysis of various market segments, historical and current trends, market forecasts, and dynamics within the global market. The historical years covered in this report are 2022 to 2023, with 2024 serving as the base year for market size calculations. The forecast period extends from 2025 to 2032.

The report includes an executive summary and a comprehensive overview of market drivers, restraints, opportunities, and challenges (DROC), along with insights into regulatory standards. It features detailed analyses such as PORTER’s Five Forces, SWOT, and PESTLE, as well as assessments of technological trends and the competitive landscape.

PORTER’s Five Forces analysis helps stakeholders evaluate the impact of new entrants, competitive rivalry, supplier power, buyer power, and substitution threats, enabling them to assess the level of competition and the attractiveness of the global market. The competitive landscape provides stakeholders with a clear understanding of the current market positions of key players, offering valuable insights into their competitive environment.

Scope And Key Highlights of The Heterogeneous Integration Market Report:

| Report Features | Details |

| Market Size in 2024 | USD 3.13 Billion |

| Market Growth Rate in CAGR (2025–2032) | 34.5 % |

| Market Revenue forecast to 2032 | USD 31.20 Billion |

| Base year | 2024 |

| Historical year | 2022–2023 |

| Forecast period | 2025–2032 |

| Report Pages | 450 |

| Segments covered |

|

| Regional scope |

|

| Country Scope |

|

| Key Market Players |

|

| Delivery Format | Reports are delivered in PDF format via email. |

| Customization scope | Request for Customization |

The heterogeneous integration market report offers a detailed analysis of market size, including historical revenue (in USD Billion) data for 2022-2023 and revenue forecasts for 2025-2032 across the following segments:

- Technology Outlook (Revenue, USD Billion; 2022-2032)

- 5D

- 3D

- System-in-Package (SiP)

- Through Silicon Vias (TSV)

- Fan-Out Wafer Level Packaging (FOWLP)

- Others

- Component Outlook (Revenue, USD Billion; 2022-2032)

- Hardware

- Sensors and MEMS

- Integrated Circuits (ICs)

- Filters

- Power Amplifiers

- Others

- Software

- Integration and Testing

- System Modeling and Simulation

- Electronic Design Automation (EDA)

- Others

- Hardware

- Material Outlook (Revenue, USD Billion; 2022-2032)

- Semiconductor Compound

- Silicon

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Substrate Material

- Organic

- Ceramic

- Glass

- Metals

- Copper

- Gold

- Aluminum

- Others

- Semiconductor Compound

- Application Outlook (Revenue, USD Billion; 2022-2032)

- Consumer Electronics

- Automotive

- IT and Telecommunications

- Aerospace and Defense

- Energy and Power

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Others

- Regional Outlook (Revenue, USD Billion; 2022-2032)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Taiwan

- Oceania

- ASEAN Countries

- Rest of APAC

- Latin America

- Brazil

- Rest of LATAM

- Middle East & Africa

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of MEA

- North America

Frequently Asked Questions (FAQ) About the Heterogeneous Integration Market Report

The market size of heterogeneous integration market was 3.13 billion in 2024.

The growth of heterogeneous integration market is expected to register a compound annual growth rate (CAGR) of 34.5% over the forecast period.

Growing demand for high-performance computing (HPC), AI, and mobile computing is a major factor driving the revenue growth of heterogeneous integration market.

Disruption in the supply chain of materials and components is a major restraint of heterogeneous integration market.

Asia-Pacific accounts for the fastest revenue growth of 38.5%.

The hardware is the major leading segment of heterogeneous integration market in terms of components.

- Market Definition

- Research Objective

- Research Methodology

- Research Design

- Data Collection Methods

- Primary

- Secondary

- Market Size Estimation

- Top-down method

- Bottom-up method

- Forecasting Methodology

- Tools and Models Used

- Market Overview and Trends

- Market Size and Forecast

- Industry Analysis

- Market Driver, Restraints, Opportunity, and Challenges (DROC) Analysis

- Market Drivers

- Growing demand for high-performance computing (HPC), AI, and mobile computing

- Increasing adoption for electric vehicles (EVs)

- Market Restraints

- High cost of development

- Disruption in supply chain of material and components

- Market Opportunities

- Deployment of 5G networks

- Rapid developments of quantum computing ecosystems

- Market Challenges

- Shortages of skilled professionals

- Geopolitical challenges

- Regulatory Landscape

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

- Strategic Insights

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Price Trend Analysis

- Value Chain Analysis

- Technological Trends

- Recent Developments

- Funding

- Merger and Acquisition

- Expansion

- Partnership and Collaboration

- Product/ Service Launch

- Technology Market Revenue Estimates and Forecasts, 2022-2032

- 5D

- 3D

- System-in-Package (SiP)

- Through Silicon Vias (TSV)

- Fan-Out Wafer Level Packaging (FOWLP)

- Others

- Component Market Revenue Estimates and Forecasts, 2022-2032

- Hardware

- Sensors and MEMS

- Integrated Circuits (ICs)

- Filters

- Power Amplifiers

- Others

- Software

- Integration and Testing

- System Modeling and Simulation

- Electronic Design Automation (EDA)

- Others

- Hardware

- Material Market Revenue Estimates and Forecasts, 2022-2032

- Semiconductor Compound

- Silicon

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Substrate Material

- Organic

- Ceramic

- Glass

- Others

- Semiconductor Compound

- Application Market Revenue Estimates and Forecasts, 2022-2032

- Consumer Electronics

- Automotive

- IT and Telecommunications

- Aerospace and Defense

- Energy and Power

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Others

- Heterogeneous Integration Market Revenue Estimates and Forecasts by Region, 2022-2032, USD Billion

- North America

- North America Heterogeneous Integration Market By Technology, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- 5D

- 3D

- System-in-Package (SiP)

- Through Silicon Vias (TSV)

- Fan-Out Wafer Level Packaging (FOWLP)

- Others

- North America Heterogeneous Integration Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Hardware

- Sensors and MEMS

- Integrated Circuits (ICs)

- Filters

- Power Amplifiers

- Others

- Software

- Integration and Testing

- System Modeling and Simulation

- Electronic Design Automation (EDA)

- Others

- North America Heterogeneous Integration Market By Material, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Semiconductor Compound

- Silicon

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Substrate Material

- Organic

- Ceramic

- Glass

- Metals

- Copper

- Gold

- Aluminum

- Others

- Semiconductor Compound

- North America Heterogeneous Integration Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Consumer Electronics

- Automotive

- IT and Telecommunications

- Aerospace and Defense

- Energy and Power

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Others

- North America Heterogeneous Integration Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion

- United States

- Canada

- Mexico

- Hardware

- North America Heterogeneous Integration Market By Technology, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Europe

- Europe Heterogeneous Integration Market By Technology, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- 5D

- 3D

- System-in-Package (SiP)

- Through Silicon Vias (TSV)

- Fan-Out Wafer Level Packaging (FOWLP)

- Others

- Europe Heterogeneous Integration Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Hardware

- Sensors and MEMS

- Integrated Circuits (ICs)

- Filters

- Power Amplifiers

- Others

- Software

- Integration and Testing

- System Modeling and Simulation

- Electronic Design Automation (EDA)

- Others

- Europe Heterogeneous Integration Market By Material, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Semiconductor Compound

- Silicon

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Substrate Material

- Organic

- Ceramic

- Glass

- Metals

- Copper

- Gold

- Aluminum

- Others

- Semiconductor Compound

- Europe Heterogeneous Integration Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Consumer Electronics

- Automotive

- IT and Telecommunications

- Aerospace and Defense

- Energy and Power

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Others

- Europe Heterogeneous Integration Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion

- Germany

- United Kingdom

- France

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Hardware

- Europe Heterogeneous Integration Market By Technology, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Asia-Pacific

- Asia-Pacific Heterogeneous Integration Market By Technology, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- 5D

- 3D

- System-in-Package (SiP)

- Through Silicon Vias (TSV)

- Fan-Out Wafer Level Packaging (FOWLP)

- Others

- Asia-Pacific Heterogeneous Integration Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Hardware

- Sensors and MEMS

- Integrated Circuits (ICs)

- Filters

- Power Amplifiers

- Others

- Software

- Integration and Testing

- System Modeling and Simulation

- Electronic Design Automation (EDA)

- Others

- Asia-Pacific Heterogeneous Integration Market By Material, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Semiconductor Compound

- Silicon

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Substrate Material

- Organic

- Ceramic

- Glass

- Metals

- Copper

- Gold

- Aluminum

- Others

- Semiconductor Compound

- Asia-Pacific Heterogeneous Integration Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Consumer Electronics

- Automotive

- IT and Telecommunications

- Aerospace and Defense

- Energy and Power

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Others

- Asia-Pacific Heterogeneous Integration Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion

- China

- India

- Japan

- South Korea

- Taiwan

- Oceania

- ASEAN Countries

- Hardware

- Asia-Pacific Heterogeneous Integration Market By Technology, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Latin America

- Latin America Heterogeneous Integration Market By Technology, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- 5D

- 3D

- System-in-Package (SiP)

- Through Silicon Vias (TSV)

- Fan-Out Wafer Level Packaging (FOWLP)

- Others

- Latin America Heterogeneous Integration Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Hardware

- Sensors and MEMS

- Integrated Circuits (ICs)

- Filters

- Power Amplifiers

- Others

- Software

- Integration and Testing

- System Modeling and Simulation

- Electronic Design Automation (EDA)

- Others

- Latin America Heterogeneous Integration Market By Material, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Semiconductor Compound

- Silicon

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Substrate Material

- Organic

- Ceramic

- Glass

- Metals

- Copper

- Gold

- Aluminum

- Others

- Semiconductor Compound

- Latin America Heterogeneous Integration Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Consumer Electronics

- Automotive

- IT and Telecommunications

- Aerospace and Defense

- Energy and Power

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Others

- Latin America Heterogeneous Integration Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion

- Brazil

- Rest of Latin America

- Hardware

- Latin America Heterogeneous Integration Market By Technology, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Middle East & Africa

- Middle East & Africa Heterogeneous Integration Market By Technology, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- 5D

- 3D

- System-in-Package (SiP)

- Through Silicon Vias (TSV)

- Fan-Out Wafer Level Packaging (FOWLP)

- Others

- Middle East & Africa Heterogeneous Integration Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Hardware

- Sensors and MEMS

- Integrated Circuits (ICs)

- Filters

- Power Amplifiers

- Others

- Software

- Integration and Testing

- System Modeling and Simulation

- Electronic Design Automation (EDA)

- Others

- Middle East & Africa Heterogeneous Integration Market By Material, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Semiconductor Compound

- Silicon

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Substrate Material

- Organic

- Ceramic

- Glass

- Metals

- Copper

- Gold

- Aluminum

- Others

- Semiconductor Compound

- Middle East & Africa Heterogeneous Integration Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- Consumer Electronics

- Automotive

- IT and Telecommunications

- Aerospace and Defense

- Energy and Power

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Others

- Middle East & Africa Heterogeneous Integration Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion

- GCC Countries

- South Africa

- Israel

- Turkey

- Hardware

- Middle East & Africa Heterogeneous Integration Market By Technology, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion

- North America

- Market Share Analysis

- Revenue Market Share by Key Players (2023-2024)

- Analysis of Top Players by Market Presence

- Competitive Matrix

- Competitive Strategies

- Mergers and Acquisitions

- Partnerships and Collaboration

- Investment and Fundings

- Agreement

- Expansion

- New Product/ Services Launches

- Technological Innovations

- ASE Technology Holding

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Applied Materials, Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Siemens AG

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Shin-Etsu Chemical Co., Ltd.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Etron Technology, Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- EV Group (EVG)

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Merck Group

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Samsung Electronics Co., Ltd.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Kulicke & Soffa Industries, Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Northrop Grumman Corporation

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- Intel Corporation

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Cadence Design Systems, Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Synopsys, Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis