Software Defined Satellites (SDS) Market Overview and Key Insights:

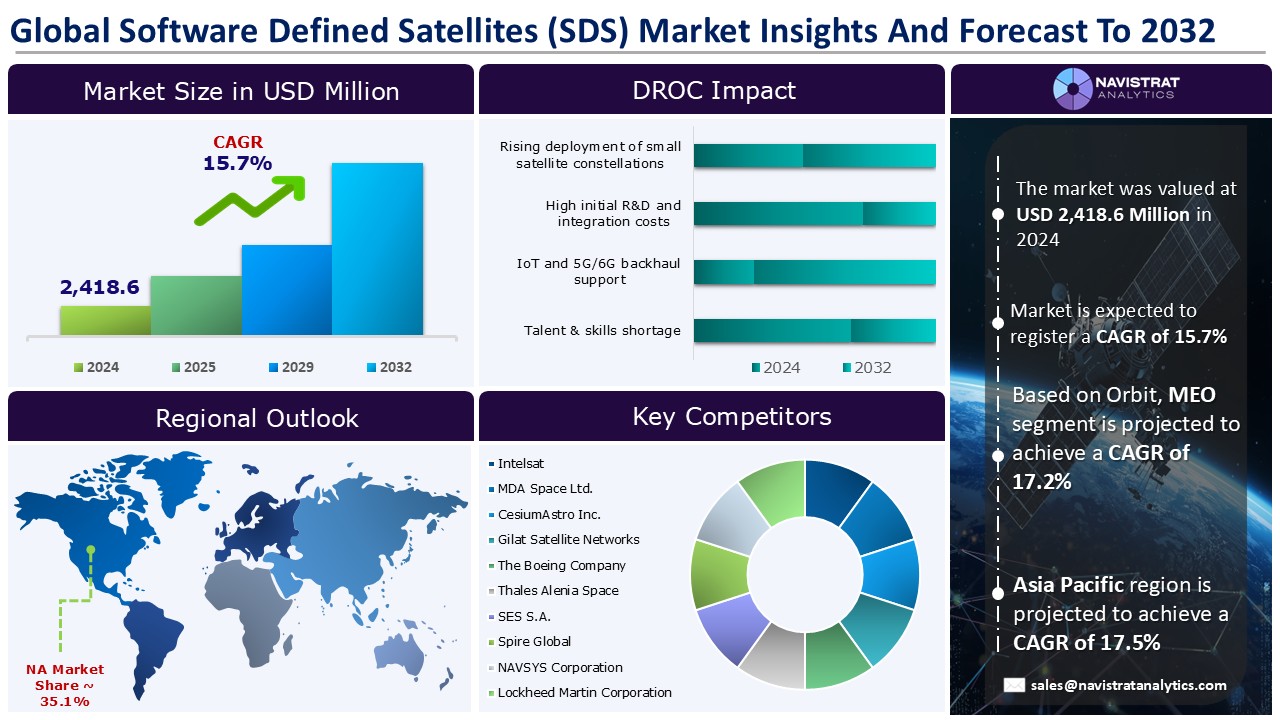

Software Defined Satellites (SDS) market size reached USD 2,418.6 Million in 2024 and is expected to register a revenue CAGR of 15.7% during the forecast period. With the rise of software-defined high-throughput satellites and non-geostationary orbit (NGSO) constellations, scalability, flexibility, and performance have become more crucial than ever. Software-defined satellite (SDS) architectures bring groundbreaking adaptability, allowing operators to customize services based on user needs and maximize capacity efficiency by allocating resources precisely where and when they are required.

Market Drivers:

Rising deployment of small satellite constellations is a key driver of revenue growth in Software Defined Satellites (SDS) market. The deployment of small satellite constellations is transforming data collection, allowing for quick revisit rates and continuous coverage of critical locations. With sophisticated imaging capabilities, these constellations provide high-resolution insights, arming decision-makers with near-real-time data.

Small satellite constellations are becoming increasingly popular among governments and business groups seeking unrivaled access to Earth intelligence. For example, in 2021, China revealed its Guowang constellation, which consists of 13,000 satellites monitored by the Chinese government. The first 10 were introduced in December 2024. China’s Shanghai Spacecom Satellite Technology (SSST) has launched 90 satellites as part of the planned 15,000-satellite Qianfan constellation (also known as ‘Thousand Sails’, SpaceSail, or G60), which has already signed service contracts with Brazil, Malaysia, and Thailand.

One of the most transformational breakthroughs in small satellite constellations is the incorporation of Synthetic Aperture Radar (SAR) technology. Unlike optical sensors, SAR can work in all-weather situations, day or night, piercing clouds, smoke, and darkness to acquire continuous pictures. This capability is a game changer for continuous Earth monitoring. Small satellites quickly analyze the level of damage from natural catastrophes like hurricanes, wildfires, and floods, providing emergency responders with actionable knowledge. This speeds up response coordination, improves resource allocation, and ultimately saves lives.

On May 2024, SKY Perfect JSAT, Asia’s largest satellite operator, and Thales Alenia Space, a joint venture between Thales and Leonardo, announced the signing of a contract to build JSAT-31, a new generation of software-defined satellite based on Thales Alenia Space’s Space INSPIRE (INstant SPace In-orbit REconfiguration) platform. JSAT-31 High Throughput Satellite, which operates in both the Ka and Ku frequency bands, will provide high-speed internet services throughout Japan, South-East Asia, Australia, New Zealand, and Pacific islands. JSAT-31, the largest capacity in the history of SKY Perfect JSAT spacecraft, is scheduled to launch in 2027.

Market Opportunity:

IoT and 5G/6G backhaul support acts as opportunities for Software Defined Satellites (SDS) market. Even in a space business with innumerable technological advancements, software-defined satellites have emerged as one of the most exciting developments. Regenerative or software-defined satellites can perform demodulation, channelization, and signal processing and modulation before retransmission by incorporating processing into the space platform. The standardization of hardware and the movement of system complexity to software have improved not only satellite manufacturing’s capital expenditure (capex), but also its operational flexibility. Software-defined satellites allow operators to change operations and capabilities after launch, which is becoming increasingly crucial as downstream markets evolve faster than before.

Software-defined satellite technology will be vital to the development and operation of 5G and 6G networks. They offer clear advantages in terms of resilience, coverage, security, and mobility. They will efficiently make 5G and 6G technology available to businesses and individuals worldwide. Software-defined satellites will be important in expanding 5G networks to the air, sea, and other remote locations that tiny cell networks cannot reach. Satellites provide seamless coverage of 5G services from cities to aeroplanes, cruise ships, and other automobiles in remote locations for end users.

On August 2025, Kratos Defense & Security Solutions, Inc., a technology company focused on defense, national security, and global markets, and hiSky announced a partnership to deliver hiSky satellite network services, including Industrial Internet of Things (IoT), as a fully orchestrated capability via Kratos’ OpenSpace dynamic, software-defined ground system. The partnership would enable satellite and other communications network operators to provide IoT connectivity services to their commercial and government customers, leveraging the size, economics, and operational benefits of a modern, cloud-enabled network architecture.

Recent Trends:

Emerging trends include software-defined ground stations, onboard Artificial Intelligence (AI)/ML/edge processing, High-Throughput Satellites (HTS), and evolution of SDRs.

The growth of commercial operators prompted new ways to improving the productivity of facilities in space and on the ground to increase profitability. The development of software-defined technologies is seen as a major technological trend aimed at lowering costs and increasing operational efficiency. With the growing demand for satellite services, there is a greater need for high-performance satellite ground stations (SGS), especially given the cutting-edge technical advancements associated with 5G and IoT, such as ground stations as a service (GSaaS).

Software-defined radios (SDR) transformed the design and operation of satellite ground stations by combining the high performance of cutting-edge radio front ends (RFEs) with flexible FPGA-based digital backends that can be reprogrammed using software without requiring any hardware changes. This versatility allows SDRs to tune to a wide range of frequencies, record massive volumes of data, and execute a variety of digital signal processing (DSP) operations on-board.

On May 2025, Terma has announced the availability of Terma SPECTRA (Software-defined Platform for Enhanced Communication, Telemetry, and Ranging Applications), a new SDR TT&C modem that provides a flexible and scalable solution for satellite communication and testing. The modem combines a flexible and cloud-ready architecture, multi-channel support for TX and RX, built-in security by design, and native L- and S-Band support to provide a small and cost-effective solution for lowering CAPEX and OPEX. The modem is intended to serve ground stations and testing facilities, and it enables operations such as satellite modem verification, satellite communications, EGSE/SCOE integration, system-level, and end-to-end testing.

Restraints & Challenges:

Satellite networks differ from terrestrial networks in that they face intrinsic obstacles such as high propagation latency, changeable topology, and limited resources. As a result, methods built for terrestrial networks are inadequate for satellite networks with specified settings. Furthermore, the development of satellite communication technologies has advanced at the same rate as terrestrial networks. These pose significant hurdles for the integration of satellite networks with terrestrial networks.

Introducing new communication technologies, algorithms, and protocols into satellite networks requires significant expenditure and latency due to software/hardware updates. Current satellite networks lack interoperability due to vendor-specific communication technology, networking protocols, and satellite services. The reprogrammability of SDS creates potential weaknesses for cyberattacks, demanding robust security measures. The dynamic reconfiguration features require more electrical power, which might strain onboard systems and necessitate new solutions.

Software Architecture Segment Insights and Analysis:

Based on the software architecture segment, Software Defined Satellites (SDS) market is segmented into on-board virtualized platforms, Software-Defined Radios (SDR), Cloud-Native Ground Integration (SaaS and PaaS), middleware & bus abstraction layers, and others.

Software-Defined Radios (SDR) segment contributed the largest market share in 2024. SDRs are highly functional RF communication systems that use software to perform operations that would normally be performed by hardware, such as modulation/demodulation and signal processing. SDRs are used in a variety of space-related applications, including ground-space communication systems, satellite-satellite communication, and on-orbit servicing. For example, because to the increased demand for more processing power, both Earth Observation (EO) and communication satellites are increasingly employing SDR technologies.

Spaceborne SDRs’ capabilities will grow as computational power and software frameworks progress. Cognitive radio technology will enable the SDR to intelligently adapt to changes in the radio environment, allowing it to operate in dynamic and unexpected communication situations. AI and machine learning could enable SDRs to adapt to space surroundings and optimize communication in real time.

On October 2024, SatixFy Communications Ltd., a market leader in next-generation satellite communication systems based on in-house-developed chipsets, has signed a software development and licensing agreement with MDA Space Ltd., a leading provider of advanced technology and services to the rapidly expanding global space industry. SatixFy will offer the modem and beamforming software for SatixFy chipsets, which will be utilized in digital satellite broadband Low Earth Orbit Constellation payloads. It will also offer SatixFy with software licenses and a development kit to help MDA Space deliver to customers.

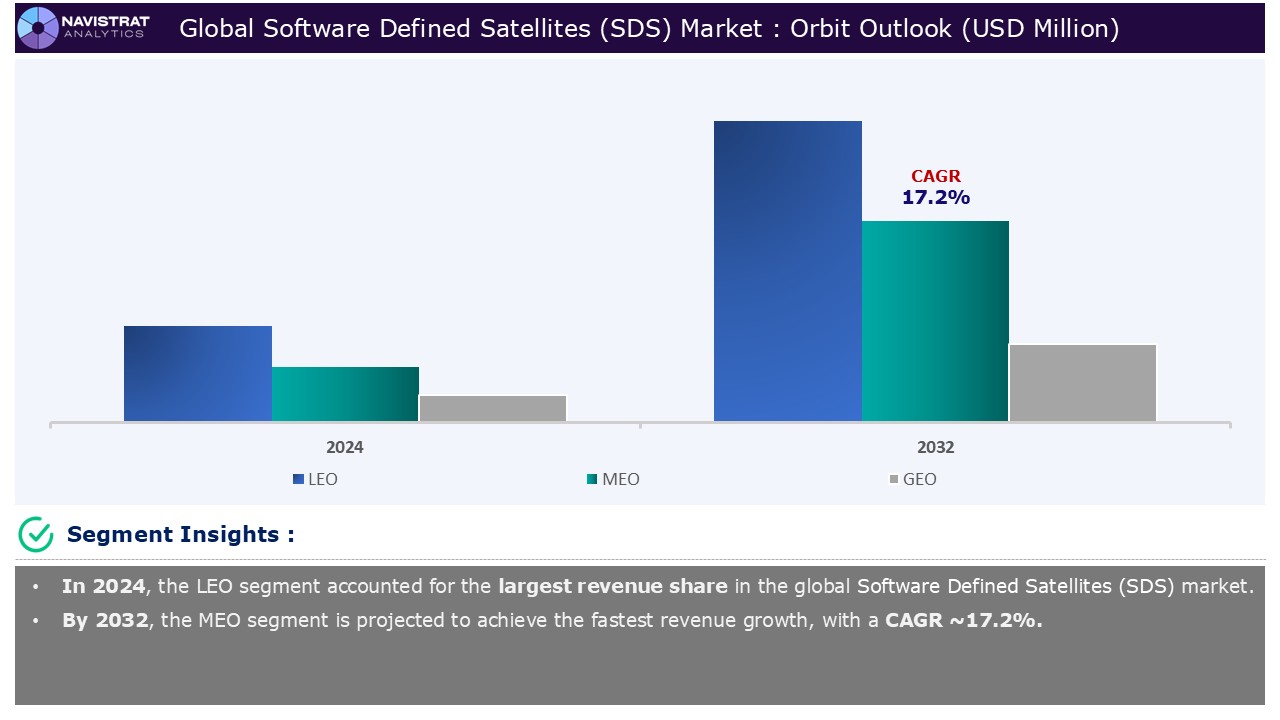

Orbit Segment Insights and Analysis:

Based on the orbit, Software Defined Satellites (SDS) market is segmented into LEO, MEO, and GEO.

LEO segment contributed the largest market share in 2024. Low Earth Orbit (LEO) satellites operate at a low altitude and hence have low propagation delay and link loss, giving them a significant advantage in supporting high-throughput services for ever-evolving mobile communication. Efficient management of the ever-expanding LEO satellite networks is critical to maximizing their superiority and providing low-latency routing services. LEO satellite networks serve mobile users directly, resulting in dynamic network traffic and different user demands. As a result, traditional satellite networks’ decentralized management design, which includes planned link allocations, is inefficient. Furthermore, the LEO satellite network topology is continually changing due to varied link quality and intermittent connectivity between satellites.

On December 2024, Parsons Corporation and Globalstar have formed an exclusive cooperation to service the public, government, and defense sectors. The agreement also involves a successful demonstration of Parsons’ software-defined satellite communications solution on Globalstar’s Low Earth Orbit (LEO) satellite fleet. Parsons and Globalstar have collaborated on an innovative solution to improve resilience against disrupted communication paths. Utilizing Globalstar’s LEO satellite constellation, the partnership aims to ensure resilient and diverse communication protocols to support a myriad of communication needs.

Application Segment Insights and Analysis:

Based on the application, Software Defined Satellites (SDS) market is segmented into Earth Observation (EO) and remote sensing, Satellite Communications (Satcom), navigation & PNT augmentation, scientific/research missions, and others.

Navigation & PNT augmentation segment contributed the largest market share in 2024. Software Defined Satellites (SDS) represent a significant advancement in space technology, providing unparalleled flexibility and adaptability in satellite operations. Unlike traditional satellites with fixed functionalities, operators can remotely reprogram software-defined satellites (SDS) to change communication parameters, coverage areas, and even mission tasks. Aligning the upstream and downstream markets in terms of software defined capabilities, standards, and conventions can help to speed growth. One of the primary advantages of software defined satellite technology is remote operational capacity, which provides ground network operators with new capabilities and efficiency levels. It will also help to virtualize ground stations and regulate satellite configurations in earth orbit.

On March 2025, Thales has announced the delivery of Ku-band Dual Travelling Wave Tubes (Dual-TWTs) for the ASTRA 1Q satellite, which was ordered by SES, a Luxembourg-based supplier of global content and connectivity solutions. ASTRA 1Q, based on Thales Alenia Space’s Space INSPIRE product line, is a software-defined satellite that can be reconfigured in orbit. This solution represents a significant advancement in geostationary satellites used for communication. The delivery of the Dual-TWTs for the ASTRA 1Q represents a significant technological advancement, improving the satellite’s communications and data management to improve both performance and operational reliability.

Geographical Outlook:

Software Defined Satellites (SDS) market is strategically segmented by geography to provide a comprehensive understanding of regional market dynamic. Discover demand analysis, emerging trends, and growth opportunities shaping market performance across different region and countries.

North America Software Defined Satellites (SDS) Market:

North America is registered to have highest market share in Software Defined Satellites (SDS) market in 2024. This is mainly driven by growing demand for flexible and reconfigurable satellites, rising deployment of small satellite constellations, and advances in on-board computing & AI/ML integration. The commercial communications sector, especially satellite internet services, has seen substantial growth due to the growing interest in satellite television and imaging. In addition, the growing number of space exploration missions and private investment in satellite technology are improving the market outlook. Governments around the world are also making significant investments in satellite infrastructure for a variety of purposes, including homeland security and disaster management. Integrating artificial intelligence (AI) models onto satellites provides considerable benefits that improve satellite operations, data management, and allow for autonomous decisions in orbit.

On April 2023, Kratos Defense & Security Solutions, Inc., a technology company specializing in defence, national security, and communications solutions, and ALL.SPACE, the world’s only provider of multi-orbit smart terminals, announced a strategic partnership to jointly develop and deliver solutions that will allow software-defined satellite ground systems to better leverage the capabilities of next-generation smart terminals. Integrated solutions will improve dynamic operations end-to-end across the ground segment, from the gateway to the network’s edge. They will give end users more application power and significantly expand flexibility beyond current proprietary, purpose-built satellite terminals.

Asia Pacific Software Defined Satellites (SDS) Market:

Asia Pacific is expected to register the fastest growth rate during the forecasted period. Significant developments in the telecommunications business, particularly in the Asia-Pacific area, are keeping pace with space innovation. The industry is experiencing a surge in power and scalability, ranging from geostationary (GEO), high (HEO), and medium earth orbits (MEO) to LEO and high-altitude platform stations (HAPS). This includes terabit-capable constellations, dynamic beam switching, and the transition from customized to standardized, software-defined payloads. Simultaneously, the Asia-Pacific telecommunications sector is undergoing a significant shift toward a comprehensive 5G infrastructure. This includes more than simply a radio access network; automation, virtualization, and orchestration are integral to 5G as a network and access technology.

On March 2025, Eutelsat Communications announced that its subsidiary, Eutelsat Asia PTE. LTD., has entered a partnership with Space Tech Innovation Limited (STI), a subsidiary of Thaicom and a prominent Asian satellite operator, to deploy a new software-defined satellite (SDS) at the 119.5° East orbital position over Asia. STI will procure the advanced geostationary SDS, which belongs to a new generation of satellites capable of real-time in-orbit adjustments and flexible reconfiguration, maximizing resource utilization for the advantage of both operators and end customers.

Europe Software Defined Satellites (SDS) Market:

Europe is expected to have considerable market share in 2024, driven by growing demand for flexible and reconfigurable satellites and rising deployment of small satellite constellations. On December 2024, the European Commission awarded a 12-year concession contract for the Infrastructure for Resilience, Interconnectivity, and Security via Satellite (IRIS²) system to SES SA, Eutelsat SA, and Hispasat S.A. The Euro 11 billion project will include little under 290 satellites, with launches beginning in 2029. The goal is to provide secure connectivity services to EU member states and governmental entities, as well as high-speed broadband to private businesses and European residents, with coverage in connectivity-deprived areas.

On September 2025, SES, a renowned space solutions provider, and K2 Space, an innovative new space technology business, have established a strategic partnership to accelerate the construction of SES’s future medium Earth orbit (MEO) network. The collaboration brings together SES’s decades of experience operating global multi-orbit networks, notably the O3b mPOWER MEO network, and K2 Space’s agile engineering capabilities to co-develop future network infrastructure and technologies.

Competition Analysis:

Software Defined Satellites (SDS) market is characterized by a fragmented structure, with several players competing across various segments and regions. List of major players included in Software Defined Satellites (SDS) market report are:

- Intelsat

- MDA Space Ltd.

- CesiumAstro Inc.

- Gilat Satellite Networks

- The Boeing Company

- Thales Alenia Space

- SES S.A.

- Spire Global

- NAVSYS Corporation

- Lockheed Martin Corporation

- L3Harris Technologies, Inc.

- Reorbit

- Hensoldt AG

- SpaceX

- Eutelsat Communications SA

Strategic Developments in Software Defined Satellites (SDS) Market:

- In February 2025, Helsing, Europe’s premier defence technology firm, and Loft Orbital, a pioneer in satellite infrastructure, announced a strategic collaboration to build and deploy a cutting-edge multi-sensor satellite constellation. This collaboration will use AI-powered capabilities to provide real-time intelligence and situational awareness to European defense and security sectors. The technology is intended for crucial duties such as border surveillance, troop movement tracking, and infrastructure security, giving European forces a strategic advantage in any operating situation.

- In September 2023, MDA Ltd., a major provider of sophisticated technology and services to the rapidly expanding global space sector, has disclosed the first details of its new software-defined digital satellite product line, as the market transitions from analog to digital software-defined satellites. The move from analog to digital satellite solutions provides considerable benefits to satellite operators wanting to improve performance while also reducing time, cost, and complexity in their LEO constellation networks.

Key Advantages for Stakeholders:

Navistrat Analytics’ industry report provides an in-depth quantitative analysis of various market segments, historical and current trends, market forecasts, and dynamics within the global market. The historical years covered in this report are 2022 to 2023, with 2024 serving as the base year for market size calculations. The forecast period extends from 2025 to 2032.

The report includes an executive summary and a comprehensive overview of market drivers, restraints, opportunities, and challenges (DROC), along with insights into regulatory standards. It features detailed analyses such as PORTER’s Five Forces, SWOT, and PESTLE, as well as assessments of technological trends and the competitive landscape.

PORTER’s Five Forces analysis helps stakeholders evaluate the impact of new entrants, competitive rivalry, supplier power, buyer power, and substitution threats, enabling them to assess the level of competition and the attractiveness of the global market. The competitive landscape provides stakeholders with a clear understanding of the current market positions of key players, offering valuable insights into their competitive environment.

Scope And Key Highlights Of Software Defined Satellites (SDS) Market Report:

| Report Features | Details |

| Market Size in 2024 | USD 2,418.6 Million |

| Market Growth Rate in CAGR (2025–2032) | 15.7% |

| Market Revenue forecast to 2032 | USD 7,802.3 Million |

| Base year | 2024 |

| Historical year | 2022-2023 |

| Forecast period | 2025-2032 |

| Report Pages | 450 |

| Segments covered |

|

| Regional scope |

|

| Country Scope |

|

| Key Market Players |

|

| Delivery Format | Reports are delivered in PDF format via email. |

| Customization scope | Request for Customization |

Software Defined Satellites (SDS) market report offers a detailed analysis of market size, including historical revenue (in USD Million) data for 2022-2023 and revenue forecasts for 2025-2032 across the following segments:

- Software Architecture Outlook (Revenue, USD Million; 2022-2032)

- On-board Virtualized Platforms

- Software-Defined Radios (SDR)

- Cloud-Native Ground Integration (SaaS and PaaS)

- Middleware & Bus Abstraction Layers

- Others

- Deployment Outlook (Revenue, USD Million; 2022-2032)

- CubeSats or NanoSats

- SmallSats or Microsats

- Medium and Large Satellites

- Orbit Outlook (Revenue, USD Million; 2022-2032)

- LEO

- MEO

- GEO

- Application Outlook (Revenue, USD Million; 2022-2032)

- Earth Observation (EO) and Remote Sensing

- Satellite Communications (Satcom)

- Navigation & PNT augmentation

- Scientific/Research Missions

- Others

- End-Use Outlook (Revenue, USD Million; 2022-2032)

- Commercial Service Providers

- Defence & National Security Agencies

- Government and Civil Agencies

- Enterprise and Vertical Customers

- Regional Outlook (Revenue, USD Million; 2022-2032)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Oceania

- ASEAN Countries

- Rest of APAC

- Latin America

- Brazil

- Rest of LATAM

- Middle East & Africa

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of MEA

- North America

Frequently Asked Questions (FAQ) about Software Defined Satellites (SDS) market report

The market size of Software Defined Satellites (SDS) market was 2,418.6 million in 2024.

The market size of Software Defined Satellites (SDS) market is expected to register compound annual growth rate (CAGR) of 15.7% over the forecast period.

Growing demand for flexible and reconfigurable satellites, rising deployment of small satellite constellations, and advances in on-board computing & AI/ML integration are major key factors driving the market revenue growth of Software Defined Satellites (SDS) market.

High initial R&D and integration costs and limited power and processing capacity in small satellites are key limiting factors driving the market.

Asia Pacific account for fastest revenue growth of 17.5%.

LEO is the major leading segment of Software Defined Satellites (SDS) market in terms of orbit.

- Market Definition

- Research Objective

- Research Methodology

- Research Design

- Data Collection Methods

- Primary

- Secondary

- Market Size Estimation

- Top-down Orbit

- Bottom-up Orbit

- Forecasting Methodology

- Tools and Models Used

- Market Overview and Trends

- Market Size and Forecast

- Industry Analysis

- Market Driver, Restraints, Opportunity, and Challenges (DROC) Analysis

- Market Drivers

- Growing demand for flexible and reconfigurable satellites

- Rising deployment of small satellite constellations

- Advances in on-board computing & AI/ML integration

- Increasing demand for real-time Earth observation & analytics

- Market Restraints

- High initial R&D and integration costs

- Limited power and processing capacity in small satellites

- Market Opportunities

- Expansion of mega-constellations in LEO

- AI-driven autonomy & self-healing satellites

- IoT and 5G/6G backhaul support

- Market Challenges

- Risk of mission failure from software bugs

- Talent & skills shortage

- Regulatory Landscape

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

- Strategic Insights

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Price Trend Analysis

- Value Chain Analysis

- Technological Trends

- Recent Developments

- Funding

- Merger and Acquisition

- Expansion

- Partnership and Collaboration

- Product/ Service Launch

- Software Architecture Market Revenue Estimates and Forecasts, 2022-2032

- On-board Virtualized Platforms

- Software-Defined Radios (SDR)

- Cloud-Native Ground Integration (SaaS and PaaS)

- Middleware & Bus Abstraction Layers

- Others

- Deployment Market Revenue Estimates and Forecasts, 2022-2032

- CubeSats or NanoSats

- SmallSats or Microsats

- Medium and Large Satellites

- Orbit Market Revenue Estimates and Forecasts, 2022-2032

- LEO

- MEO

- GEO

- Application Market Revenue Estimates and Forecasts, 2022-2032

- Earth Observation (EO) and Remote Sensing

- Satellite Communications (Satcom)

- Navigation & PNT augmentation

- Scientific/Research Missions

- Others

- End-Use Market Revenue Estimates and Forecasts, 2022-2032

- Commercial Service Providers

- Defence & National Security Agencies

- Government and Civil Agencies

- Enterprise and Vertical Customers

- Software Defined Satellites (SDS) Market Revenue Estimates and Forecasts by Region, 2022-2032, USD Million

- North America

- North America Software Defined Satellites (SDS) Market By Software Architecture, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- On-board Virtualized Platforms

- Software-Defined Radios (SDR)

- Cloud-Native Ground Integration (SaaS and PaaS)

- Middleware & Bus Abstraction Layers

- Others

- North America Software Defined Satellites (SDS) Market By Deployment, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- CubeSats or NanoSats

- SmallSats or Microsats

- Medium and Large Satellites

- North America Software Defined Satellites (SDS) Market By Orbit, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- LEO

- MEO

- GEO

- North America Software Defined Satellites (SDS) Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Earth Observation (EO) and Remote Sensing

- Satellite Communications (Satcom)

- Navigation & PNT augmentation

- Scientific/Research Missions

- Others

- North America Software Defined Satellites (SDS) Market By End-Use, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Commercial Service Providers

- Defence & National Security Agencies

- Government and Civil Agencies

- Enterprise and Vertical Customers

- North America Software Defined Satellites (SDS) Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- United States

- Canada

- Mexico

- North America Software Defined Satellites (SDS) Market By Software Architecture, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Europe

- Europe Software Defined Satellites (SDS) Market By Software Architecture, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- On-board Virtualized Platforms

- Software-Defined Radios (SDR)

- Cloud-Native Ground Integration (SaaS and PaaS)

- Middleware & Bus Abstraction Layers

- Others

- Europe Software Defined Satellites (SDS) Market By Deployment, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- CubeSats or NanoSats

- SmallSats or Microsats

- Medium and Large Satellites

- Europe Software Defined Satellites (SDS) Market By Orbit, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- LEO

- MEO

- GEO

- Europe Software Defined Satellites (SDS) Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Earth Observation (EO) and Remote Sensing

- Satellite Communications (Satcom)

- Navigation & PNT augmentation

- Scientific/Research Missions

- Others

- Europe Software Defined Satellites (SDS) Market By End-Use, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Commercial Service Providers

- Defence & National Security Agencies

- Government and Civil Agencies

- Enterprise and Vertical Customers

- Europe Software Defined Satellites (SDS) Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- Germany

- United Kingdom

- France

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Europe Software Defined Satellites (SDS) Market By Software Architecture, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Asia Pacific

- Asia Pacific Software Defined Satellites (SDS) Market By Software Architecture, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- On-board Virtualized Platforms

- Software-Defined Radios (SDR)

- Cloud-Native Ground Integration (SaaS and PaaS)

- Middleware & Bus Abstraction Layers

- Others

- Asia Pacific Software Defined Satellites (SDS) Market By Deployment, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- CubeSats or NanoSats

- SmallSats or Microsats

- Medium and Large Satellites

- Asia Pacific Software Defined Satellites (SDS) Market By Orbit, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- LEO

- MEO

- GEO

- Asia Pacific Software Defined Satellites (SDS) Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Earth Observation (EO) and Remote Sensing

- Satellite Communications (Satcom)

- Navigation & PNT augmentation

- Scientific/Research Missions

- Others

- Asia Pacific Software Defined Satellites (SDS) Market By End-Use, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Commercial Service Providers

- Defence & National Security Agencies

- Government and Civil Agencies

- Enterprise and Vertical Customers

- Asia Pacific Software Defined Satellites (SDS) Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- China

- India

- Japan

- South Korea

- Oceania

- ASEAN Countries

- Rest of Asia Pacific

- Asia Pacific Software Defined Satellites (SDS) Market By Software Architecture, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Latin America

- Latin America Software Defined Satellites (SDS) Market By Software Architecture, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- On-board Virtualized Platforms

- Software-Defined Radios (SDR)

- Cloud-Native Ground Integration (SaaS and PaaS)

- Middleware & Bus Abstraction Layers

- Others

- Latin America Software Defined Satellites (SDS) Market By Deployment, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- CubeSats or NanoSats

- SmallSats or Microsats

- Medium and Large Satellites

- Latin America Software Defined Satellites (SDS) Market By Orbit, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- LEO

- MEO

- GEO

- Latin America Software Defined Satellites (SDS) Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Earth Observation (EO) and Remote Sensing

- Satellite Communications (Satcom)

- Navigation & PNT augmentation

- Scientific/Research Missions

- Others

- Latin America Software Defined Satellites (SDS) Market By End-Use, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Commercial Service Providers

- Defence & National Security Agencies

- Government and Civil Agencies

- Enterprise and Vertical Customers

- Latin America Software Defined Satellites (SDS) Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- Brazil

- Rest of Latin America

- Latin America Software Defined Satellites (SDS) Market By Software Architecture, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Middle East and Africa

- Middle East and Africa Software Defined Satellites (SDS) Market By Software Architecture, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- On-board Virtualized Platforms

- Software-Defined Radios (SDR)

- Cloud-Native Ground Integration (SaaS and PaaS)

- Middleware & Bus Abstraction Layers

- Others

- Middle East and Africa Software Defined Satellites (SDS) Market By Deployment, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- CubeSats or NanoSats

- SmallSats or Microsats

- Medium and Large Satellites

- Middle East and Africa Software Defined Satellites (SDS) Market By Orbit, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- LEO

- MEO

- GEO

- Middle East and Africa Software Defined Satellites (SDS) Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Earth Observation (EO) and Remote Sensing

- Satellite Communications (Satcom)

- Navigation & PNT augmentation

- Scientific/Research Missions

- Others

- Middle East and Africa Software Defined Satellites (SDS) Market By End-Use, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- Commercial Service Providers

- Defence & National Security Agencies

- Government and Civil Agencies

- Enterprise and Vertical Customers

- Middle East and Africa Software Defined Satellites (SDS) Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Million

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of Middle East and Africa

- Middle East and Africa Software Defined Satellites (SDS) Market By Software Architecture, Market Revenue Estimates and Forecasts, 2022-2032, USD Million

- North America

- Market Share Analysis

- Revenue Market Share by Key Players (2023-2024)

- Analysis of Top Players by Market Presence

- Competitive Matrix

- Competitive Strategies

- Mergers and Acquisitions

- Partnerships and Collaboration

- Investment and Fundings

- Agreement

- Expansion

- New Software Architecture/ Services Launches

- Technological Innovations

- Intelsat

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- MDA Space Ltd.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- CesiumAstro Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Gilat Satellite Networks

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- The Boeing Company

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Thales Alenia Space

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- SES S.A.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Spire Global

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- NAVSYS Corporation

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Lockheed Martin Corporation

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- L3Harris Technologies, Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Reorbit

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Hensoldt AG

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- SpaceX

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Eutelsat Communications SA

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis