Autonomous Vehicles Market Overview and Key Insights:

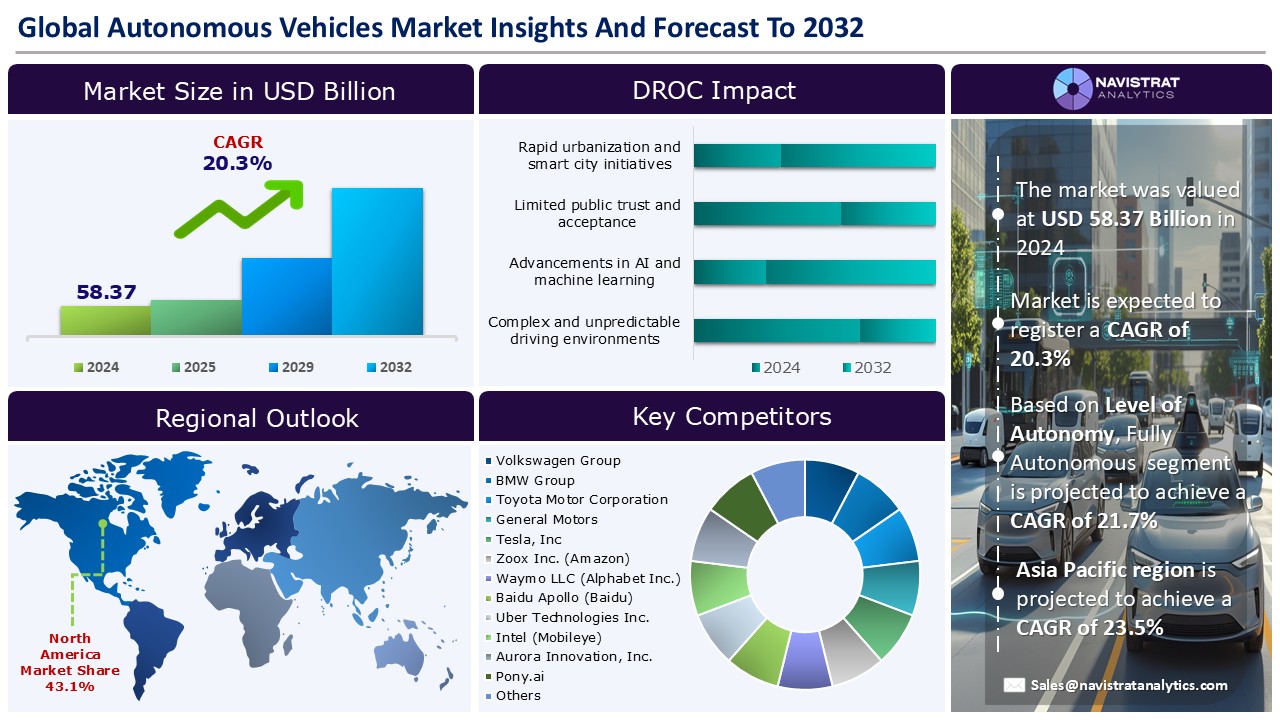

The global autonomous vehicles market reached USD 58.37 billion in 2024 and is expected to register a revenue CAGR of 20.3% during the forecast period. Increasing development of Advanced Driver Assistance Systems (ADAS), rising demand for safety and reduction in road accidents, growing need for efficient and productive transportation, expanding applications of autonomous vehicles in logistics and last-mile delivery, and rapid urbanization and smart city initiatives are expected to drive revenue growth of the market.

Market Drivers:

Rapid urbanization and smart city initiatives are the major factors driving revenue growth of the market. The demand for efficient, safe, and sustainable transportation solutions has intensified in recent days due to the rising population in cities. According to the United Nations, by 2050, 68% of the global population is expected to reside in cities and urban areas. It leads to a steady increase in emissions and energy consumption. This growing urbanization underscores the urgent need for more intelligent and sustainable transportation systems.

Smart city frameworks prioritize reducing traffic congestion, lowering emissions, and improving public mobility systems, all areas where autonomous vehicles offer tangible benefits. AVs, particularly in the form of robo-taxis, autonomous shuttles, and last-mile delivery vehicles, are being integrated into urban transport ecosystems to optimize mobility and reduce human dependency. All of these create high demand for autonomous vehicles in smart cities and drive revenue growth of the market.

Additionally, governments and municipal bodies are investing in connected infrastructure such as V2X communication systems and smart traffic management. These advancements are encouraging companies to accelerate the development and deployment of AV technologies. In May 2025, for instance, Waymo, a subsidiary of Google, announced plans to begin testing its self-driving vehicles in Alamo City. The company noted that these dynamic urban environments offer valuable insights as it expands autonomous mobility to additional communities. Before this, Waymo had already launched its technology in Texas through a partnership with rideshare leader Uber. It brings robotaxi services to the city of Austin.

Market Opportunity:

Growing investments from OEMs and leading technology companies are creating significant opportunities for the market. Automotive giants such as General Motors, Toyota, and Hyundai, alongside tech leaders like Google (Waymo), NVIDIA, and Intel (Mobileye), are pouring significant capital into the research, development, and commercialization of autonomous driving technologies. These investments are accelerating innovation across hardware, software, and AI-powered driving systems. It enables faster progress toward higher levels of vehicle autonomy.

In October 2024, Waymo, the autonomous driving division of Alphabet, successfully secured USD 5.6 billion in an oversubscribed funding round led by its parent company. The round also saw participation from existing investors and major private equity firms. The funds will be used to scale Waymo’s commercial ride-hailing service, “Waymo One”, to additional U.S. cities and to enhance its AI-driven “Waymo Driver” technology platform, which supports a range of autonomous mobility applications. These accelerate commercialization and expand the overall revenue growth potential of the autonomous vehicles market

Recent Trends:

One recent trend in the autonomous vehicles market is the rising expansion of robotaxi services. Tesla is set to launch its robotaxi service in Austin, Texas, starting with a fleet of approximately 10 vehicles and plans to scale up to 1,000 units in the coming months. Waymo, a subsidiary of Alphabet, has rapidly expanded its operations, now offering services in cities like San Francisco, Phoenix, Los Angeles, Austin, and Atlanta, with plans to enter markets such as Miami and Tokyo. Chinese companies like WeRide and Baidu are also extending their reach. WeRide is initiating fully driverless robotaxi trials in Abu Dhabi and planning expansions into Saudi Arabia and Europe. This trend is signaling a shift toward more widespread adoption of autonomous mobility solutions and drives revenue growth of the market.

Restraints & Challenges:

High development and deployment costs remain significant restraints to the revenue growth of the autonomous vehicles market. Developing AV technology requires significant investment in advanced sensors, high-performance computing systems, AI algorithms, and continuous testing across diverse environments. These components, especially LiDAR, radar, and onboard processing units, are expensive and contribute heavily to the overall cost of manufacturing autonomous vehicles. The high cost of AVs also makes them less accessible to mass-market consumers. It slows down adoption and limits revenue growth of the market.

Component Segment Insights and Analysis:

Based on the component, the autonomous vehicles market is segmented into hardware and software. Hardware segment is further sub-segmented into LiDAR, radar, cameras, ultrasonic sensors, GPS/IMU, Electronic Control Units (ECUs), and others. Software segment is further sub-segmented into driving algorithms, mapping & localization, data processing & analytics, Real-time Operating Systems (RTOS), and others.

Hardware segment contributed the largest share in 2024 due to the increasing investments in Advanced Driver-Assistance Systems (ADAS), LiDAR, radar, and camera systems essential for vehicle autonomy. The demand for high-performance sensors, onboard computing units, and communication modules has surged in recent years due to the deployment of Level 3 and Level 4 autonomous driving technologies. In May 2025, Innoviz Technologies announced it is expanding its partnership with Volkswagen Autonomous Mobility to speed up the deployment of its InnovizTwo LiDAR sensors in the ID. Buzz AD, Volkswagen’s Level 4 autonomous shuttle. This enhanced collaboration aims to fast-track the integration of InnovizTwo units into the autonomous shuttle platform.

In addition, rising production of electric autonomous vehicles and expanding pilot programs for robotaxis, autonomous delivery and ride sharing fleets are fueling the need for robust and scalable hardware solutions. For instance, Waymo is actively expanding its Waymo One commercial ride-hailing service across multiple U.S. cities by leveraging its fleet of autonomous vehicles. At present, the company delivers approximately 250,000 paid rides weekly in regions including the San Francisco Bay Area, Los Angeles, Phoenix, and Austin. It also plans to extend its services to new markets, with upcoming launches expected in Washington D.C. and Miami.

Level of Autonomy Segment Insights and Analysis:

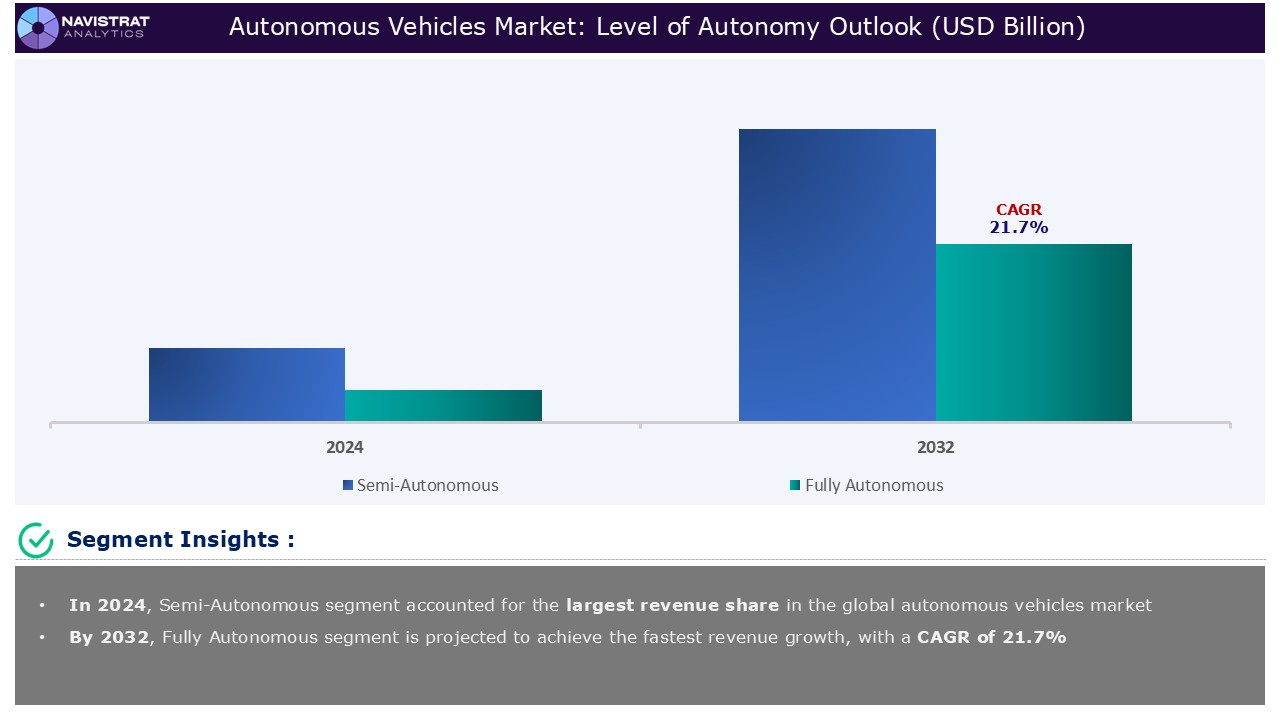

Based on the level of autonomy, the autonomous vehicles market is segmented into semi-autonomous and fully autonomous. Semi-autonomous segment is further sub-segmented into Level 1 (driver assistance), Level 2 (partial automation), and Level 3 (conditional automation). Fully autonomous segment is further sub-segmented into Level 4 (high automation), and Level 5 (full automation).

Fully autonomous segment is expected to register a fast revenue growth rate during the forecast period due to the increasing investments in Level 4 and Level 5 vehicle technologies, along with expanding commercial applications such as robotaxis, autonomous shuttles, and delivery vehicles. Companies like Waymo, Cruise, and Baidu are scaling up pilot programs and launching commercial services in urban areas. It creates new revenue streams and accelerates revenue growth of this segment.

In November 2025, Nissan and Mitsubishi formed a joint venture to provide services that incorporate self-driving and electric vehicles. Their goal is to launch a passenger transport service utilizing Level 4 autonomous driving technology, which allows vehicles to operate independently without human intervention in specific conditions. This type of initiative creates high demand for autonomous vehicles through ride-hailing and mobility-as-a-service (MaaS) offerings and drives revenue growth of this segment.

Application Segment Insights and Analysis:

Based on application, the autonomous vehicles market is segmented into transportation, agriculture, construction, military & defense and others.

Transportation segment contributed the largest share in 2024 due to the increasing adoption of autonomous solutions in ride-hailing, public transit, and goods delivery services. The integration of self-driving technology in urban mobility systems is reducing operational costs, improving efficiency, and enabling 24/7 service availability. Companies like Waymo, Cruise, and Baidu are scaling commercial operations, while automakers and tech firms are forming partnerships to launch autonomous shuttles and robotaxi services.

Additionally, the rising demand for last-mile delivery and logistics automation, especially in e-commerce and retail sectors, is driving investments in autonomous transportation fleets. In September 2024, Cainiao Group is rolling out its newest Level 4 autonomous vehicles to support parcel deliveries along public roads, specifically between delivery hubs and pickup points. These vehicles are built on Alibaba’s AutoDrive platform and are primarily intended for commercial use at delivery stations. They come equipped with an integrated service support system to ensure safe navigation on public roads and have obtained operational clearance in several regions across China.

Geographical Outlook:

Autonomous Vehicles market is strategically segmented by geography to provide a comprehensive understanding of regional market dynamic. Discover demand analysis, emerging trends, and growth opportunities shaping market performance across different region and countries.

North America Autonomous Vehicles Market:

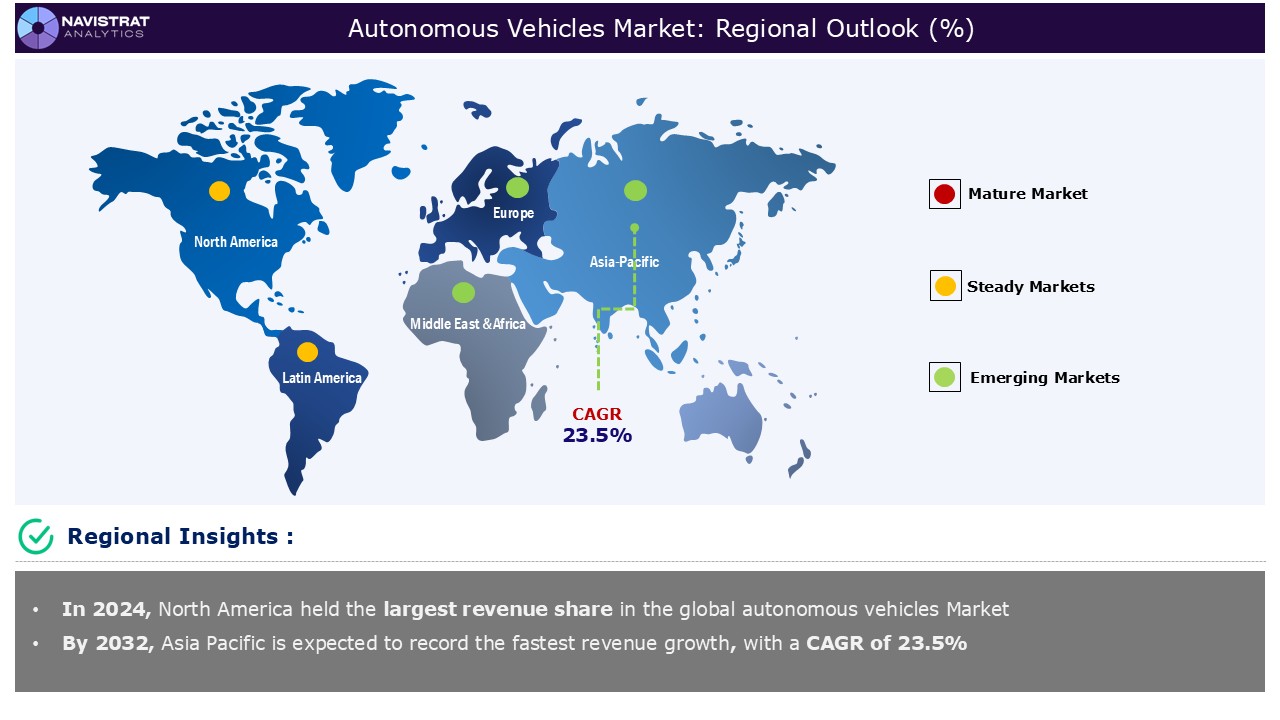

Market in North America accounted for largest revenue share in 2024 due to the strong technological innovation, favorable regulatory support, and significant investments from leading automotive and technology companies. The region is home to major players such as Waymo, Cruise, Tesla, and Aurora, who are actively deploying autonomous driving technologies across various applications. It includes ride-hailing, logistics, and last-mile delivery. Pilot programs and commercial operations in cities like San Francisco, Phoenix, and Austin are also accelerating the adoption of autonomous vehicles in the region, especially in U.S. In July 2024, Alphabet, the parent company of Waymo, announced plans to invest up to USD 5 billion in the company, coinciding with the launch of the sixth generation of its Waymo Driver autonomous driving technology. It stimulates demand for autonomous vehicles and drives revenue growth of the market in this region.

The Autonomous Vehicles market in Canada is also witnessing significant momentum due to supportive regulatory frameworks and increasing consumer demand for innovative transportation solutions. Provinces such as Ontario and Quebec are leading in the development and testing of autonomous vehicle technologies. In February 2024, the federal government announced to allocate USD 8 million to establish two real-world pilot zones aimed at advancing the development and commercialization of zero-emission and connected/autonomous vehicle technologies. These pilot sites, located in Toronto and Windsor-Sarnia, will be managed by the Ontario Vehicle Innovation Network (OVIN) under the Ontario Centre of Innovation (OCI).

Asia Pacific Autonomous Vehicles Market:

Market in Asia Pacific is expected to register a fast revenue growth rate during the forecast period due to technological advancements, supportive government policies, and increasing demand for safer and more efficient transportation solutions. Countries such as China, Japan, South Korea, and Singapore are at the forefront of this growth, with substantial investments in autonomous driving research and development. China stands out due to its rapidly developing economy and robust technology sector. Local governments also have been instrumental in advancing the sector, with cities like Beijing, Shanghai, and Shenzhen establishing dedicated autonomous driving test zones. These cities provide incentives such as subsidies, expedited permitting processes, and strategic partnerships to promote development. These test areas enable AV companies to trial their technologies in real-world environments while facing fewer regulatory barriers compared to many western nations.

China has already secured over USD 10 billion in investments related to autonomous vehicles. It benefits both established companies and emerging startups. These funds are driving swift progress in areas such as artificial intelligence, sensor systems, and real-time data processing. Major Chinese firms like Baidu, AutoX, WeRide, and Pony.ai are at the forefront, committing significant resources to the development of autonomous vehicle technologies. For example, Baidu’s Apollo platform ranks among the most comprehensive open autonomous vehicle platforms globally. It launched commercial robotaxi operations across multiple cities. In 2022 alone, its Apollo Go service completed more than 1.4 million rides. Other leading Chinese players, such as AutoX, WeRide, and Pony.ai, have also achieved notable milestones. Pony.ai, with headquarters in both Silicon Valley and Guangzhou, has secured approvals to run fully driverless vehicles in select regions of China and is collaborating with Toyota to expand the reach of its autonomous driving technology.

Europe Autonomous Vehicles Market:

Europe accounted for a significant revenue share in 2024 due to the supportive regulatory frameworks for testing and deployment of autonomous vehicles on public roads, especially in U.K., Germany, and France. For instance, the United Kingdom has passed the Automated Vehicles (AV) Act, allowing autonomous vehicles to operate without a safety driver. The AV Act allows advanced technology to operate vehicles safely on British roads. This new legislation positions U.K as a global leader in self-driving technology regulation. It unlocks an industry estimated to be valued at up to £42 billion (USD 57 billion) and generating 38,000 additional skilled jobs by 2035.

The autonomous vehicles market in Germany is also witnessing significant revenue growth due to the combination of technological advancements, supportive regulatory frameworks, and strategic industry partnerships. For the first time in Germany, Level 4 autonomous vehicles are carrying passengers as part of the KIRA Project. It is a trial program in the Rhine-Main area. The pilot features on-demand robotaxi services operating in the city of Langen and the municipality of Egelsbach within the Offenbach district. Additionally, the service is planned to expand to certain areas of Darmstadt later this year.

Competition Analysis:

The Autonomous Vehicles market is characterized by a fragmented structure, with numerous players competing across various segments and regions. List of major players included in the Autonomous Vehicles market report are:

Original Equipment Manufacturers (OEMs):

- Volkswagen Group

- BMW Group

- Toyota Motor Corporation

- General Motors

- Tesla, Inc

- Hyundai Motor Group

- Mercedes-Benz Group AG

- Volvo Group

- Ford Motor Company

- Nissan Motor Co., Ltd

Autonomous Mobility Service Provider:

- Zoox Inc. (Amazon)

- Waymo LLC (Alphabet Inc.)

- Baidu Apollo (Baidu)

- Uber Technologies Inc.

- Beijing Didi Chuxing Technology Co., Ltd

- Lyft Inc

- Sixt SE

- May Mobility

Autonomous Technology and Component Provider:

- Intel (Mobileye)

- Aurora Innovation, Inc.

- Motional

- WeRide AI

- WeRide AI

- AutoX, Inc.

- Aptiv PLC

- NVIDIA Corporation

- Continental AG

- Robert Bosch GmbH

- Nuro, Inc

- Einride

Strategic Developments in Autonomous Vehicles Market:

- On 01 May 2025, Uber Technologies, Inc. and May Mobility, Inc., a leading autonomous vehicle technology firm, unveiled a new long-term strategic alliance. As part of the collaboration, May Mobility plans to introduce thousands of autonomous vehicles to the Uber platform in the coming years, starting with an initial deployment in Arlington, Texas. This partnership reflects the shared goal of both companies to rapidly expand the integration of autonomous vehicles within the ride-hailing industry.

- On 29 April 2025, Toyota Motor Corporation and Waymo entered into a preliminary agreement to investigate a joint effort aimed at advancing the development and rollout of autonomous driving technologies. Woven by Toyota, acting as Toyota’s strategic innovation arm, will also participate by leveraging its expertise in advanced software and mobility solutions. The prospective partnership is grounded in a mutual commitment to enhancing road safety and expanding mobility access for everyone.

- On 09 April 2025, Autonomous vehicle developer Nuro announced that it has secured USD 106 million to date in its ongoing Series E funding round, which places the company’s valuation at USD 6 billion. This latest round brings Nuro’s cumulative funding to USD 2.2 billion, with additional Series E investors expected to join soon. The company plans to utilize the new capital to enhance its technology platform and strengthen its commercial collaborations.

Key Advantages for Stakeholders:

Navistrat Analytics’ industry report provides an in-depth quantitative analysis of various market segments, historical and current trends, market forecasts, and dynamics within the global market. The historical years covered in this report are 2022 to 2023, with 2024 serving as the base year for market size calculations. The forecast period extends from 2025 to 2032.

The report includes an executive summary and a comprehensive overview of market drivers, restraints, opportunities, and challenges (DROC), along with insights into regulatory standards. It features detailed analyses such as PORTER’s Five Forces, SWOT, and PESTLE, as well as assessments of technological trends and the competitive landscape.

PORTER’s Five Forces analysis helps stakeholders evaluate the impact of new entrants, competitive rivalry, supplier power, buyer power, and substitution threats, enabling them to assess the level of competition and the attractiveness of the global market. The competitive landscape provides stakeholders with a clear understanding of the current market positions of key players, offering valuable insights into their competitive environment.

Scope And Key Highlights of The Autonomous Vehicles Market Report:

| Report Features | Details |

| Market Size in 2024 | USD 58.37 Billion |

| Market Growth Rate in CAGR (2025–2032) | 20.3% |

| Market Revenue Forecast to 2032 | USD 244.27 Billion |

| Base year | 2024 |

| Historical year | 2022–2023 |

| Forecast period | 2025–2032 |

| Report Pages | 450 |

| Segments Covered |

|

| Regional scope |

|

| Country Scope |

|

| Key Market Players (OEMs) |

|

| Autonomous Mobility Service Provider |

|

| Autonomous Technology and Component Provider |

|

| Delivery Format | Reports are delivered in PDF format via email. |

| Customization scope | Request Customization |

The Autonomous Vehicles market report offers a detailed analysis of market size, including historical revenue (in USD Billion) data for 2022-2023 and revenue forecasts for 2025-2032 across the following segments:

- Component (Revenue, USD Billion; Volume, Thousand Units; 2022-2032)

- Hardware

- LiDAR

- Radar

- Cameras

- Ultrasonic Sensors

- GPS/IMU

- Electronic Control Units (ECUs)

- Others

- Software

- Driving Algorithms

- Mapping & Localization

- Data Processing & Analytics

- Real-time Operating Systems (RTOS)

- Others

- Hardware

- Level of Autonomy Outlook (Revenue, USD Billion; Volume, Thousand Units; 2022-2032)

- Semi-Autonomous

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Fully Autonomous

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Semi-Autonomous

- Vehicle Type Outlook (Revenue, USD Billion; Volume, Thousand Units; 2022-2032)

- Passenger Vehicles

- Private Passenger Vehicles

- Public Passenger Vehicles

- Autonomous Buses

- Robo-taxis

- Others

- Commercial Vehicles

- Automatic Guided Vehicle (AGV)

- Autonomous Vans

- Autonomous Truck

- Autonomous Drones

- Others

- Off-highway Vehicles

- Autonomous Tractors

- Autonomous Harvester

- Autonomous Cranes

- Autonomous Excavators

- Passenger Vehicles

- Mobility Type (Revenue, USD Billion; Volume, Thousand Units; 2022-2032)

- Shared Mobility

- Personal Mobility

- Application (Revenue, USD Billion; Volume, Thousand Units; 2022-2032)

- Transportation

- Agriculture

- Construction

- Military & Defense

- Others

- Regional Outlook (Revenue, USD Billion; Volume, Thousand Units; 2022-2032)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Oceania

- ASEAN Countries

- Rest of APAC

- Latin America

- Brazil

- Rest of LATAM

- Middle East & Africa

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of MEA

- North America

Frequently Asked Questions (FAQ) about the Autonomous Vehicles Market Report

The autonomous vehicles market size was USD 58.37 billion in 2024.

The autonomous vehicles market revenue is expected to register a Compound Annual Growth Rate (CAGR) of 20.3% during the forecast period.

Increasing development of Advanced Driver Assistance Systems (ADAS), rising demand for safety and reduction in road accidents, growing need for efficient and productive transportation, expanding applications of autonomous vehicles in logistics and last-mile delivery, and rapid urbanization and smart city initiatives are key drivers of the autonomous vehicles market revenue growth.

High development and deployment costs, vulnerability to hacking, spoofing, and software glitches, and Limited public trust and acceptance are key factors restraining revenue growth of the market.

Asia Pacific is expected to account for the fastest revenue growth of 23.5%.

Semi-autonomous segment is the leading segment of autonomous vehicles market in terms of level of autonomy.

- Market Definition

- Research Objective

- Research Methodology

- Research Design

- Data Collection Methods

- Primary

- Secondary

- Market Size Estimation

- Top-down method

- Bottom-up method

- Forecasting Methodology

- Tools and Models Used

- Market Overview and Trends

- Market Size and Forecast

- Industry Analysis

- Market Driver, Restraints, Opportunities, and Challenges (DROC) Analysis

- Market Drivers

- Increasing development of Advanced Driver Assistance Systems (ADAS)

- Rising demand for safety and reduction in road accidents

- Growing need for efficient and productive transportation

- Expanding applications of autonomous vehicles in logistics and last-mile delivery

- Rapid urbanization and smart city initiatives

- Market Restraints

- High development and deployment costs

- Vulnerability to hacking, spoofing, and software glitches

- Limited public trust and acceptance

- Market Opportunities

- Advancements in AI and Machine Learning

- Supportive government regulations and investments

- Growing investments from OEMs and leading technology companies

- Rapid development of 5G and V2X communication

- Market Challenges

- Inadequate infrastructure

- Complex and unpredictable driving environments

- Interoperability and standardization gaps

- Regulatory Landscape

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

- Strategic Insights

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Price Trend Analysis

- Value Chain Analysis

- Technological Trends

- Recent Developments

- Funding

- Merger and Acquisition

- Expansion

- Partnership and Collaboration

- Product/Service Launch

- Component Market Revenue Estimates and Forecasts, 2022-2032

- Hardware

- LiDAR

- Radar

- Cameras

- Ultrasonic Sensors

- GPS/IMU

- Electronic Control Units (ECUs)

- Others

- Software

- Driving Algorithms

- Mapping & Localization

- Data Processing & Analytics

- Real-time Operating Systems (RTOS)

- Others

- Hardware

- Level of Autonomy Market Revenue Estimates and Forecasts, 2022-2032

- Semi-Autonomous

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Fully Autonomous

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Semi-Autonomous

- Global Autonomous Vehicles Market By Vehicle Type, Market Estimates and Forecasts, (USD Billion), (Thousand Units)

- Vehicle Type Market Revenue Estimates and Forecasts, 2022-2032

- Passenger Vehicles

- Private Passenger Vehicles

- Public Passenger Vehicles

- Autonomous Buses

- Robo-taxis

- Others

- Commercial Vehicles

- Automatic Guided Vehicle (AGV)

- Autonomous Vans

- Autonomous Truck

- Autonomous Drones

- Others

- Off-highway Vehicles

- Autonomous Tractors

- Autonomous Harvester

- Autonomous Cranes

- Autonomous Excavators

- Others

- Passenger Vehicles

- Vehicle Type Market Revenue Estimates and Forecasts, 2022-2032

- Mobility Type Market Revenue Estimates and Forecasts, 2022-2032

- Shared Mobility

- Personal Mobility

- Application Market Revenue Estimates and Forecasts, 2022-2032

- Transportation

- Agriculture

- Construction

- Military & Defense

- Others

- Autonomous Vehicles Market Revenue Estimates and Forecasts by Region, 2022-2032, USD Billion, Thousand Units

- North America

- North America Autonomous Vehicles Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Hardware

- LiDAR

- Radar

- Cameras

- Ultrasonic Sensors

- GPS/IMU

- Electronic Control Units (ECUs)

- Others

- Software

- Driving Algorithms

- Mapping & Localization

- Data Processing & Analytics

- Real-time Operating Systems (RTOS)

- Others

- Hardware

- North America Autonomous Vehicles Market By Level of Autonomy, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Semi-Autonomous

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Fully Autonomous

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Semi-Autonomous

- North America Autonomous Vehicles Market By Vehicle Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Passenger Vehicles

- Private Passenger Vehicles

- Public Passenger Vehicles

- Autonomous Buses

- Robo-taxis

- Others

- Commercial Vehicles

- Automatic Guided Vehicle (AGV)

- Autonomous Vans

- Autonomous Truck

- Autonomous Drones

- Others

- Off-highway Vehicles

- Autonomous Tractors

- Autonomous Harvester

- Autonomous Cranes

- Autonomous Excavators

- Others

- Passenger Vehicles

- North America Autonomous Vehicles Market By Mobility Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Shared Mobility

- Personal Mobility

- North America Autonomous Vehicles Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Transportation

- Agriculture

- Construction

- Military & Defense

- Others

- North America Autonomous Vehicles Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion, Thousand Units

- United States

- Canada

- Mexico

- North America Autonomous Vehicles Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Europe

- Europe Autonomous Vehicles Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Hardware

- LiDAR

- Radar

- Cameras

- Ultrasonic Sensors

- GPS/IMU

- Electronic Control Units (ECUs)

- Others

- Software

- Driving Algorithms

- Mapping & Localization

- Data Processing & Analytics

- Real-time Operating Systems (RTOS)

- Others

- Hardware

- Europe Autonomous Vehicles Market By Level of Autonomy, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Semi-Autonomous

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Fully Autonomous

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Semi-Autonomous

- Europe Autonomous Vehicles Market By Vehicle Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Passenger Vehicles

- Private Passenger Vehicles

- Public Passenger Vehicles

- Autonomous Buses

- Robo-taxis

- Others

- Commercial Vehicles

- Automatic Guided Vehicle (AGV)

- Autonomous Vans

- Autonomous Truck

- Autonomous Drones

- Others

- Off-highway Vehicles

- Autonomous Tractors

- Autonomous Harvester

- Autonomous Cranes

- Autonomous Excavators

- Others

- Passenger Vehicles

- Europe Autonomous Vehicles Market By Mobility Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Shared Mobility

- Personal Mobility

- Europe Autonomous Vehicles Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Transportation

- Agriculture

- Construction

- Military & Defense

- Others

- Europe Autonomous Vehicles Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion, Thousand Units

- Germany

- United Kingdom

- France

- Italy

- Spain

- Benelux

- Nordic Countries

- Rest of Europe

- Europe Autonomous Vehicles Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Asia-Pacific

- Asia-Pacific Autonomous Vehicles Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Hardware

- LiDAR

- Radar

- Cameras

- Ultrasonic Sensors

- GPS/IMU

- Electronic Control Units (ECUs)

- Others

- Software

- Driving Algorithms

- Mapping & Localization

- Data Processing & Analytics

- Real-time Operating Systems (RTOS)

- Others

- Hardware

- Asia-Pacific Autonomous Vehicles Market By Level of Autonomy, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Semi-Autonomous

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Fully Autonomous

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Semi-Autonomous

- Asia-Pacific Autonomous Vehicles Market By Vehicle Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Passenger Vehicles

- Private Passenger Vehicles

- Public Passenger Vehicles

- Autonomous Buses

- Robo-taxis

- Others

- Commercial Vehicles

- Automatic Guided Vehicle (AGV)

- Autonomous Vans

- Autonomous Truck

- Autonomous Drones

- Others

- Off-highway Vehicles

- Autonomous Tractors

- Autonomous Harvester

- Autonomous Cranes

- Autonomous Excavators

- Others

- Passenger Vehicles

- Asia-Pacific Autonomous Vehicles Market By Mobility Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Shared Mobility

- Personal Mobility

- Asia-Pacific Autonomous Vehicles Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Transportation

- Agriculture

- Construction

- Military & Defense

- Others

- Asia-Pacific Autonomous Vehicles Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion, Thousand Units

- China

- India

- Japan

- South Korea

- Oceania

- ASEAN Countries

- Rest of Asia-Pacific

- Asia-Pacific Autonomous Vehicles Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Latin America

- Latin America Autonomous Vehicles Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Hardware

- LiDAR

- Radar

- Cameras

- Ultrasonic Sensors

- GPS/IMU

- Electronic Control Units (ECUs)

- Others

- Software

- Driving Algorithms

- Mapping & Localization

- Data Processing & Analytics

- Real-time Operating Systems (RTOS)

- Others

- Hardware

- Latin America Autonomous Vehicles Market By Level of Autonomy, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Semi-Autonomous

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Fully Autonomous

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Semi-Autonomous

- Latin America Autonomous Vehicles Market By Vehicle Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Passenger Vehicles

- Private Passenger Vehicles

- Public Passenger Vehicles

- Autonomous Buses

- Robo-taxis

- Others

- Commercial Vehicles

- Automatic Guided Vehicle (AGV)

- Autonomous Vans

- Autonomous Truck

- Autonomous Drones

- Others

- Off-highway Vehicles

- Autonomous Tractors

- Autonomous Harvester

- Autonomous Cranes

- Autonomous Excavators

- Others

- Passenger Vehicles

- Latin America Autonomous Vehicles Market By Mobility Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Shared Mobility

- Personal Mobility

- Latin America Autonomous Vehicles Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Transportation

- Agriculture

- Construction

- Military & Defense

- Others

- Latin America Autonomous Vehicles Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion, Thousand Units

- Brazil

- Rest of Latin America

- Latin America Autonomous Vehicles Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Middle East & Africa

- Middle East & Africa Autonomous Vehicles Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Hardware

- LiDAR

- Radar

- Cameras

- Ultrasonic Sensors

- GPS/IMU

- Electronic Control Units (ECUs)

- Others

- Software

- Driving Algorithms

- Mapping & Localization

- Data Processing & Analytics

- Real-time Operating Systems (RTOS)

- Others

- Hardware

- Middle East & Africa Autonomous Vehicles Market By Level of Autonomy, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Semi-Autonomous

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Fully Autonomous

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Semi-Autonomous

- Middle East & Africa Autonomous Vehicles Market By Vehicle Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Passenger Vehicles

- Private Passenger Vehicles

- Public Passenger Vehicles

- Autonomous Buses

- Robo-taxis

- Others

- Commercial Vehicles

- Automatic Guided Vehicle (AGV)

- Autonomous Vans

- Autonomous Truck

- Autonomous Drones

- Others

- Off-highway Vehicles

- Autonomous Tractors

- Autonomous Harvester

- Autonomous Cranes

- Autonomous Excavators

- Others

- Passenger Vehicles

- Middle East & Africa Autonomous Vehicles Market By Mobility Type, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Shared Mobility

- Personal Mobility

- Middle East & Africa Autonomous Vehicles Market By Application, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Transportation

- Agriculture

- Construction

- Military & Defense

- Others

- Middle East & Africa Autonomous Vehicles Market Revenue Estimates and Forecasts by Country, 2022-2032, USD Billion, Thousand Units

- GCC Countries

- South Africa

- Israel

- Turkey

- Rest of Middle East & Africa

- Middle East & Africa Autonomous Vehicles Market By Component, Market Revenue Estimates and Forecasts, 2022-2032, USD Billion, Thousand Units

- Market Share Analysis

- Revenue Market Share by Key Players (2023-2024)

- Analysis of Top Players by Market Presence

- Competitive Matrix

- Competitive Strategies

- Mergers and Acquisitions

- Partnerships and Collaboration

- Investment and Funding

- Agreement

- Expansion

- New Product/Service Launches

- Technological Innovations

- Volkswagen Group

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- BMW Group

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Toyota Motor Corporation

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- General Motors

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Tesla, Inc

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Hyundai Motor Group

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Mercedes-Benz Group AG

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Volvo Group

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Ford Motor Company

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Nissan Motor Co., Ltd

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Zoox Inc. (Amazon)

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Waymo LLC (Alphabet Inc.)

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Baidu Apollo (Baidu)

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Uber Technologies Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Beijing Didi Chuxing Technology Co., Ltd

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Lyft Inc

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Sixt SE

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- May Mobility

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Intel (Mobileye)

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Aurora Innovation, Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Motional

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- ai

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- WeRide AI

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- AutoX, Inc.

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Aptiv PLC

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- NVIDIA Corporation

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Continental AG

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Robert Bosch GmbH

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Nuro, Inc

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis

- Einride

- Company Overview

- Financial Insights

- Product/ Services Offerings

- Strategic Developments

- SWOT Analysis